Subsection 55(1) - Definitions

See Also

Daggett v. MNR, 93 DTC 14 (TCC)

A series of transactions pursuant to which the taxpayer used borrowed funds under a daylight loan to subscribe for common shares of a loss company controlled by him, had the company declare and pay a capital dividend to him in the same amount, used the dividend proceeds to repay the daylight loan and then sold the shares for $1 to an acquaintance, would have given rise to an artificial capital loss contrary to s. 55(1), even if such transactions had been legally effective.

Distribution

See Also

Northern Hot Oil Services Ltd. v. The Queen, 97 DTC 12107 (TCC)

A transaction in which the common shares of a corporation held by the taxpayer were purchased for cancellation for consideration consisting of equipment and cash did not qualify under former s. 55(3)(b) given that the cash and equipment could not be regarded as a single type of property for purposes of that provision and given that it was the parties' intention that the taxpayer receive more than its proportionate share of the equipment of the corporation.

Administrative Policy

2015 Ruling 2014-0548491R3 - Split-up XXXXXXXXXX Butterfly

A split up of DC's business among three brothers (A, B and C) and their respective immediate families is accomplished by split-up style butterfly transfers to ACo and Bco of pro rata portions of the three types of DC's property, so that C remains as a shareholder of DC.

2015 Ruling 2013-0490651R3 - Single-wing Split-up Farm Butterfly

DC carries on a farming business. There is a single-wing butterfly transfer of its three types of property to TC, to which Sibling 1 has transferred his shares of DC, so that Siblings 1 and 2 may now indirectly carry on separate farming businesses.

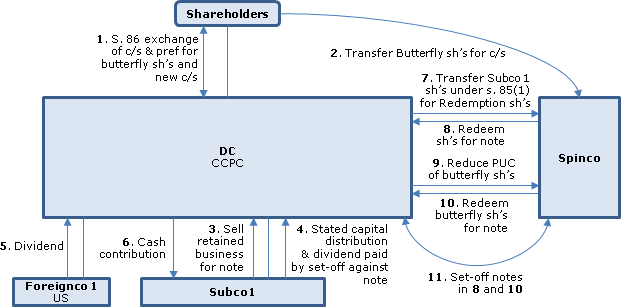

2014 Ruling 2014-0533601R3 - Spin-off butterfly - subsection 55(2)

Current structure

DC, which is a Canadian-controlled private corporation, carries on the production, processing and sale of XX (the "DC Retained Business") through subsidiaries including Subco 1 (which is wholly-owned) and a chain of U.S. subsidiaries (Foreignco 1, Foreignco 2 and Foreignco 3) as its principal business, and also carries on the "Subco 1 Transferred Business 1") and the "Subco 1 Transferred Business" (also both active businesses) through Subco 1. DC's issued share capital consists of Class A common shares and Class B and C common shares which are convertible into Class A common shares, as well as non-voting non-retractable and redeemable Class A and B preferred shares. The DC shareholders (who mostly are CCPCs but also include individuals and trusts) each hold an equal number of common and preferred shares on a stapled basis (i.e., any sale must consist of an equal number of common and preferred shares).

Subco 1 lands

Subco 1 carries on the Subco 1 Transferred Business 1 on the "Subco 1 Land 1" and "Subco 1 Land 2". Currently certain of the land surrounding the existing operations as described above acts as XX for those operations. Of these XX are presently leased to XX. All leasing revenue received has been reported by Subco 1 as active business income, representing income that is earned in connection with the Subco 1 Transferred Business 1. Subco 1 has also leased portions of the Subco 1 Land 1 and a portion of the Subco 1 Land 2 to third parties that operate XX businesses. Subco 1 acquires the XX of these businesses, and uses XX for its business operations. In addition, a business operates a XX business on an incidental portion of the same acreage that Subco 1 uses primarily as the XX. All leasing revenue received by Subco 1 from the XX businesses has been reported by Subco 1 as active business income, such income being earned in connection with the Subco 1 Transferred Business 1.

Proposed transactions

The following transactions will occur under a Plan of Arrangement to accomplish a spin-off of Subco 1 and 2 Transferred Business through Spinco, which was incorporated but has no shareholders:

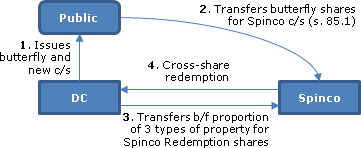

- Under a s. 86 reorganization, each DC shareholder will exchange all of its DC common shares for "DC Butterfly Shares" and Class D, E or F common shares (with the aggregate paid-up capital of the exchanged shares being apportioned), such that the aggregate fair market value of the DC Butterfly Shares will be equal to the "Butterfly Ratio" (equal to the relative net FMV of Subco 1 Transferred Business 1 and 2) multiplied by the aggregate FMV of all the DC shares held immediately before the exchange – and the FMV of the Class D, E or F common shares received on the exchange will capture the balance of the FMV of the exchanged Class A, B or C common shares. The Class E and F common shares will be convertible into Class D common shares. "The holders of these shares will not be entitled to stock dividends having a different stated capital amount as [was the case for] the A Common Shares, B Common Shares, and C Common Shares…[and] shall be provided consolidated unaudited quarterly financial statements prepared by DC in accordance with international financial reporting standards…[a right which] does not exist for the holders of the A Common Shares, B Common Shares, and C Common Shares" (para. 23.2). Also under the s. 86 reorganization, each DC shareholder's Class A (or B) Preferred Shares will be exchanged for Class G (or H) Common Shares having an aggregate FMV equal to that of the exchanged shares.

- The DC shareholders will transfer each DC Butterfly Share to Spinco in exchange for one Spinco common share (so that the test in s. (b)(iii) of "permitted exchange" in s. 55(1) is satisfied).

- Subco 1 will transfer the "Subco 1 Retained Business" solely in consideration for the "Sale Note." ("The preference of management was not to further complicate the Proposed Transactions by inserting a sequential butterfly transaction' here instead.)

- Subco 1 will distribute an amount to DC as a reduction of the PUC of its shares and declare dividends equal to any remaining portion of the amount received in 3, with payment effected by set-off of the Sale Note.

- Foreignco 1 will pay a cash dividend to DC.

- With a view to the pro rata cash or near cash test to be satisfied in 7 below, DC will contribute the cash so received to Subco 1.

- DC will transfer its Subco 1 shares to Spinco in consideration for "Spinco Redemption Shares," with a joint s. 85(1) election filed. Having regard to the pro rata three types of property tests, the Suhco 1 land will be classified as business property, and no property will be treated as investment property.

- DC will accept a note from Spinco as full payment for redemption of the Spinco Redemption Shares.

- DC will reduce the stated capital of the DC Butterfly Shares to an amount equaling that of the Spinco Redemption Shares before their redemption ("to ensure that each of Spinco's and DC's respective dividend refunds under subsection 129(1) and respective Part IV tax under paragraph 186(1)(a) (all in respect of the dividends arising on the redemption of the DC Butterfly Shares, and the dividends arising on the redemption of the Spinco Redemption Shares) will be approximately equal to each other, such that each of DC and Spinco will not have any net tax liabilities (i.e., as a result of each corporation's Part IV tax liabilities exceeding such corporation's dividend refund)."

- Similarly to 8, DC will redeem the DC Butterfly Shares.

- The notes issued in 8 and 10 will be set off.

Rulings

: Including application of s. 85.1 to 2, s. 86 to 1 and standard butterfly rulings.

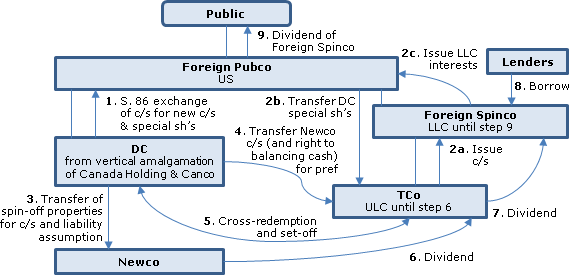

2014 Ruling 2014-0530961R3 - Cross-Border Butterfly

Overview

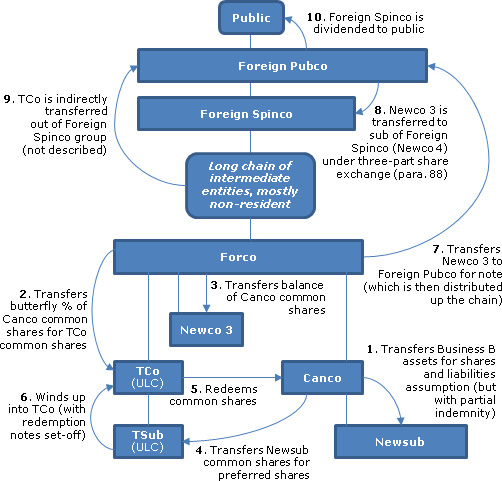

In connection with a spin-off by a U.S. public company (Foreign PubCo) of a U.S. subsidiary (Foreign Spinco) to which one of its businesses was transferred, there was a butterfly split-up of an indirect Canadian subsidiary (DC) directly and indirectly holding Canadian portions of the two businesses in question, so that the Canadian transferee corporation (TCo) of DC was a subsidiary of Foreign Spinco. In order that the butterfly transactions could qualify as a tax-free spin-off for Code purposes, TC (a ULC) and Foreign Spinco (an LLC) initially were fiscally transparent for Code purposes – then TC elected to be fiscally regarded in order that it could qualify for Treaty benefits and the Foreign Spinco became a C-corp in order that its spin-off could comply with Code rules. There was provision for a second stage transfer of cash by DC to TC if that was required to satisfy the requirements under the butterfly rules for a pro rata distribution of property of DC. As with other cross-border butterflies, there was a three-party share exchange agreement.

Background

Foreign Pubco is a U.S. resident whose common shares trade on an exchange. Prior to the "Spin-Out," being the distribution of Foreign Spinco Shares as a dividend-in-kind to the shareholders of Foreign Pubco, Foreign Pubco was engaged, through its subsidiaries, in the "Retained Services Business" and the "Transferred Services Business." The Retained Services Business in Canada and the Canadian Transferred Services Business were operated directly by Canco and indirectly through its subsidiaries. Canco was a subsidiary of Canada Holding.

Preliminary transactions

- "Foreign Spinco" was established as an LLC by Foreign Pubco.

- The worldwide Transferred Services Business, other than the Canadian Transferred Services Business, was transferred to Foreign Spinco.

Butterfly and Spin-Out transactions

- Canada Holding and Canco amalgamated through a vertical amalgamation to form DC, which elected to be treated as a corporation for Code purposes.

- The common shares of DC were changed by articles of amendment into a shares of a new class of common shares (the "DC New Common Shares") having X votes per share and shares of a new class of non-voting redeemable retractable non-cumulative special shares (the "DC Special Shares"), with the cumulative stated capital of the issued DC New Common Shares and DC Special Shares not exceeding that of the old common shares.

- Under a three-party transfer agreement between Foreign Pubco, Foreign Spinco and TCo (a newly-incorporated Canadian subsidiary of Foreign Spinco which was fiscally transparent for Code purposes): ( a) TCo paid the purchase price for DC Special Shares transferred to it by Foreign Pubco as described in para. (b) below by issuing TCo Common Shares to Foreign Spinco; (b) Foreign Pubco paid the purchase price for the member ship interests issued to it by Foreign Spinco as described in para. (c) below by transferring all of the DC Special Shares to TCo; and (c) Foreign Spinco paid the purchase price for the TCo Common Shares issued to it by TCo as described in para. (a) above by issuing membership interests to Foreign Pubco.

- DC transferred a proportionate share of each type of its property to "Newco," a newly-incorporated subsidiary (with such transferred assets relating to the Canadian Transferred Services Business and including the shares of some of its subsidiaries and portions of the vendor take-back notes ("Notes 1 and 2") received on a previous sale of subsidiaries in consideration for additional Newco common shares and the assumption of liabilities related to the Canadian Transferred Services Business. In determining the net FMV of each type of property of DC and its subsidiaries (anticipated to be cash or near-cash property, including excess cash from the previous sale of subsidiaries, investment property comprising Note 2, and business property), the net FMV of any accounts receivable, trade receivables, inventories and prepaid expenses of such corporation or partnership remaining after the allocation of current liabilities to cash or near-cash property were reclassified as business property "to the extent that such property will be collected, sold, used or consumed in the ordinary course of business to which such property relates." For the purposes of the related s. 85(1) election "the reference in subparagraph 85(1)(e)(i) to the ‘undepreciated capital cost to the taxpayer of all property of that class immediately before the disposition' shall be interpreted to mean that proportion of the undepreciated capital cost to DC of all of the property of that class immediately before the disposition, that the FMV at that time of the particular property that was transferred was of the FMV at that time of all property of that class."

- DC transferred all of the Newco Common Shares to TCo and became legally obligated to transfer to TCo within XX days any cash or near-cash property required in order to result in a proportionate transfer of that type of property.

- TCo and DC redeemed the TCo Preferred Shares and DC Special Shares respectively for promissory notes, which were accepted as full repayment of the redemption prices ("with the risk of the note being dishonored").

- The promissory notes were set-off against each other.

- TCo elected to become a corporation for Code purposes.Newco paid a dividend to TCo comprising cash and the portions of Notes 1 and 2 received by it in 4.

- TCo, in turn, paid a dividend (net of withholding) to Foreign Spinco comprising the cash and Note interests received in 9 plus the right acquired in 5 to the additional cash transfer. Foreign Spinco in turn distributed such property to Foreign Pubco.

- Foreign Spinco converted from an LLC into a C-Corp.

- Foreign Spinco borrowed the "External Debt" from third party lenders (which did not relate to any particular assets of Foreign Spinco) and "distributed" the applicable portion thereof to Foreign Pubco so as to qualify as a tax-free distribution under Code s. 361(b).

- The only parties to an Agreement were Foreign Pubco and Foreign Spinco "and, therefore, Canada Holding or its subsidiaries (or DC following the Amalgamation) did not acquire any rights pursuant to this agreement as a party thereto."

- Foreign Pubco distributed the Foreign Spinco Shares pro rata to its shareholders as a dividend-in-kind (the "Spin-Out"), with such shares being listed. The Foreign Pubco shareholders who are US residents are not taxable respecting the Spin-Out.

- To comply with s. 86.1 respecting the Spin-Out, Foreign Pubco will provide the Minister with the required s. 86.1(2)(e) information and the Canadian resident shareholders of Foreign Pubco will elect in writing (including the s. 86.1(2)(f) information) for s. 86.1 to apply to the Spin-Out.

Additional information and purposes

DC intends to pay a dividend to Foreign Pubco during its XXXX taxation year after the completion of the Subject Transactions. This dividend will be considered to be paid out of previously taxed income, for US tax purposes, that can be distributed to Foreign Pubco without additional US tax. This dividend and the Canadian butterfly transactions (in 1 to 7) are completely unrelated.

TCo was initially a fiscally disregarded entity for Code purposes in order for the transactions in 1 to 7 to qualify as a tax-free spin-off for such purposes - and it converted to a fiscally regarded entity in 8 to qualify US Treaty benefits.

None of the purposes of the dividend in 9 was to reduce the gain inherent in the Newco Common Shares, as TCo has no intention to dispose of the Newco Common Shares.

Without the amalgamation in 1, two butterfly transactions would have been required.

Foreign Spinco was formed as an LLC in order for the transactions described in 1 to 7 to qualify as a tax-free spin-off for Code purposes., and converted to a C-corp prior to the Spin-Out in order for the distribution of Foreign Pubco's Foreign Spinco Shares to its public shareholders in 14 to comply with the Code rules.

Rulings

- S. 55(3)(b) ruling is premised on 10% or more of the FMV of the Foreign Spinco membership interests or shares not, at any time, during the course the series being derived from the DC Special Shares or TCo Common Shares. For these purposes, the External Debt of Foreign Spinco will be considered to reduce the FMV of each property of Foreign Spinco pro rata in proportion to the relative FMV of all property of Foreign Spinco.

- S. 86 will apply to 2.

- Provided that all of the conditions of ss. 86.1(2)(e) and (f) are met, the Spin-Out in 14is an eligible distribution for purposes of s. 86.1.

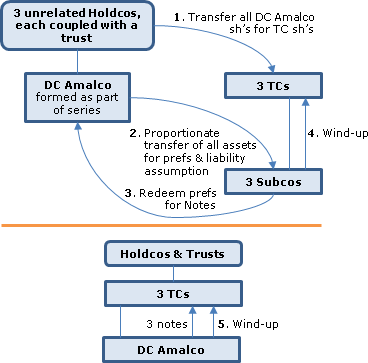

2014 Ruling 2013-0513211R3 - Butterfly Transaction

Current structure

The Class A common shares of DC1, a CCPC, are owned equally by Holdco1, Holdco2 and Holdco3 and its Class J preferred shares are owned equally by Trust1, Trust2 and Trust3. The Class A common and Class E preferred shares of DC2 are owned equally by Holdco1, Holdco2 and Holdco3.

Proposed transactions

- Holdco1 and Trust1 will form TC1, Holdco2 and Trust2 will form TC2 and Holdco3 and Trust3 will form TC1.

- DC1 and DC2 will amalgamate to form DC Amalco.

- The three shareholder groupings (comprising a Holdco and Trust) will transfer their DC Amalco shares to their TC in consideration for shares of that TC (with appropriately limited stated capital), electing under s. 85(1).

- DC Amalco will transfer to a Subco of each TC a pro rata portion of each of its three types of property (determined on a net basis) in consideration for the assumption of liabilities and the issuance of redeemable preferred shares, election under s. 85(1).

- Each Subco will redeem such preferred shares for a note.

- Each Subco will be wound up into its respective TC parent, with the notes thereby being assumed by the respective TCs.

- DC Amalco will be wound up into the three TCs, so that the respective notes will be assigned to the respective TC which, as such TC also is the debtor, will result in each such note being extinguished.

- DC Amalco will elect under s. 83(2) to treat the portion of the winding-up dividend referred to in s. 88(2)(b)(i) as a separate capital dividend paid on its classes of shares.

- DC Amalco will make a s. 89(14) designation on the portion of the winding-up dividend referred to in s. 88(2)(b)(iii) which is deemed to be a separate dividend.

- Following receipt of a dividend refund arising under the transactions, DC Amalco will dividend such cash to each TC.

- Within a reasonable time thereafter articles of dissolution will be filed by DC Amalco.

Part IV tax circularity/83(2.1)

"[A]t no time will one of the main purposes of the acquisition of the shares of DC Amalco be to receive a capital dividend. ... The purpose of the incorporation of Subco1, Subco2 and Subco3 is to avoid circularity in the calculation of DC Amalco's refundable dividend tax on hand and Part IV tax, that would otherwise occur if the transfer of property described in [4] were made directly to each TC by DC Amalco."

Rulings

Standard butterfly rulings. S. 88(2) rulings re DC Amalco wind-up (steps 7-9).

2014 Ruling 2013-0498651R3 - Single-Wing Split-up Butterfly

underline;">: Background. The sole shareholders of DC, which holds a farm property, are two siblings (Sibling1 and Sibling2) and their respective spouses (Spouse1 and Spouse2). Prior to the series of transactions, Sibling1 and Sibling2 had DC sold most of its farm machinery and commenced to operate on a share crop basis.

There is no connection between the farm machinery and equipment sales and the series. …

DC owns property ("Property1") which was rezoned… . From XX to XX, XX lots of Property1 have been severed and sold. There may be subsequent sales of lots of Property1.

Proposed transactions

Under a single-wing split-up butterfly of DC, a proportionate share (determined on a net basis) of each of its three types of property, including a co-ownership interest in Property1, will be transferred to TC, which will be owned by Sibling1 and Spouse1.

Rulings

: Typical butterfly rulings including that s. 85(1) will apply to the transfers of eligible property held by DC to TC, and that for this purpose

the "undepreciated capital cost to the taxpayer of all property of that class immediately before the disposition" found in subparagraph 85(1)(e)(i) shall be interpreted to mean that proportion of the undepreciated capital cost to the taxpayer of all property of that class immediately before the disposition, that the fair market value at that time of the property that is transferred is of the fair market value at that time of all property of that class.

2014 Ruling 2012-0446701R3 - Butterfly reorganization

Split-up butterfly is "being undertaken to allow each of [cousins] B and C to carry on separate farming operations from one another, and to independently formulate and implement a strategic development plan in respect of the portion of DC's property to be transferred to BCo and CCo."

2014 Ruling 2012-0432441R3 - Butterfly reorganization

Standard split-up butterfly of DC for division of DC between families of Brother 1 and 2.

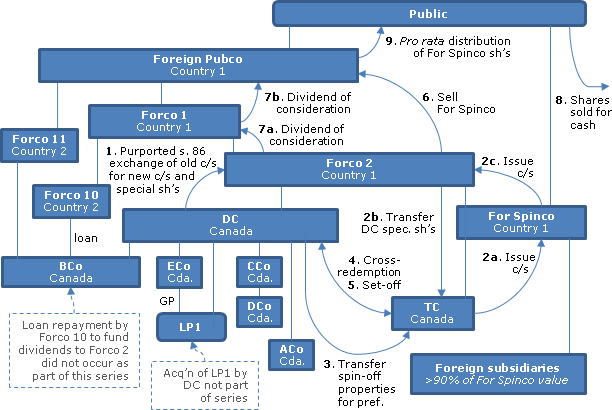

2013 Ruling 2013-0491651R3 - Cross-Border Butterfly

Overview

The ordinary shares of Foreign PubCo, which was formed under the laws of Country 1, trade on Exchange 1. The worldwide business operations in one of its two main business segments (the Spin-Off Business), which are not already owned directly or indirectly by Foreign SpinCo, will be transferred directly or indirectly to Foreign SpinCo (a great-grandchild subsidiary held by Foreign PubCo "through" ForCo 1 and ForCo 2) and Foreign PubCo will retain the Retained Business segments. DC (a wholly-owned subsidiary of ForCo 2 and thus a "sister" of Foreign SpinCo) owns A Co, which directly carries on the activities that relate to the DC Spin-Off Business and will become the indirect subsidiary of Foreign SpinCo in preparation for the Spin-Out, by virtue of DC effecting a split-up butterfly of the Spin-Off Business to TC, a direct newly-incorporated Newco subsidiary of ForCo2. Activities directly carried on in Canada by other subsidiaries of DC, namely, B Co (whose commons shares also were held by ForCo11, a subsidiary of Foreign PubCo), C Co, D Co (wholly-owned by C Co), and LP 1 and E Co, the GP of LP 1, are to be retained by DC after the Spin-Out.

Preliminary transactions

- LP 1 was acquired by DC at a time that "the directors of DC had no knowledge or expectation of the Proposed Transactions," with such acquisition being represented to be part of the series which includes 3.

- ForCo 10 (described in redacted para. 61 and likely owned outside the DC group) repaid debt owing to B Co, B Co paid a dividend to DC and ForCo11,and DC paid a dividend to ForCo2 with such transactions being represented not have been effected before the proposed transactions were contemplated.

- Numerous restructuring steps with a view to the spin-off in 9 occurred outside Canada and did not impact any of the Canadian entities or the types of property analysis for DC as no properties were transferred to or from DC group.

Proposed transactions

- The common shares of DC will be changed by articles of amendment into a shares of a new class of common shares (the "DC New Common Shares") having one vote per share and shares of a new class of non-voting redeemable retractable non-cumulative special shares (the "DC Special Shares"), with the cumulative stated capital of the issued DC New Common Shares and DC Special Shares not exceeding that of the old common shares.

- A three-party transfer agreement will be concluded and implemented between ForCo 2, Foreign SpinCo and TC (a newly-incorporated Canadian subsidiary of Foreign SpinCo) in which: ( a) TC will agree to pay the purchase price for DC Special Shares transferred to it by ForCo 2 as described in para. (b) below by issuing TC Common Shares to Foreign SpinCo; (b) ForCo 2 will agree to pay the purchase price for the common shares issued to it by Foreign SpinCo as described in para. (c) below by transferring all of the DC Special Shares to TC; and (c) Foreign SpinCo will agree to pay the purchase price for the TC Common Shares issued to it by TC as described in para. (a) above by issuing common shares to ForCo 2.

- DC will transfer a proportionate share of each type of its property to TC (with certain cash or near-cash property transferred XX days later) in consideration for TC Preferred Shares. In determining the net FMV of each type of property of DC and its subsidiaries (anticipated to be cash or near-cash property and business property), (a) the net FMV of any accounts receivable, trade receivables, inventories and prepaid expenses of such corporation or partnership remaining after the allocation of current liabilities to cash or near-cash property will be reclassified as business property "to the extent that such property will be collected, sold, used or consumed in the ordinary course of business to which such property relates," and (b) any current ("as determined by the method prescribed by the applicable pension legislation") pension plan, post-retirement benefit or liability insurance liabilities of DC will be allocated to cash or near-cash property, and any such liabilities of a non-current nature will be allocated to business property – and similarly for employee incentive plans.

- TC and DC will redeem the TC Preferred Shares and DC Special Shares respectively for promissory notes, which will be accepted as full repayment of the redemption prices.

- The promissory notes will be set-off against each other.

- ForCo 2 will sell all of its issued and outstanding shares in Foreign SpinCo to Foreign PubCo for book value in exchange for an intercompany loan.

- ForCo 2 will declare a dividend to ForCo 1, and ForCo 1 will declare a dividend to Foreign PubCo, which in each case will be settled with an intercompany loan.

- Foreign PubCo will not distribute shares of Foreign SpinCo to shareholders who are domiciled in countries where Foreign SpinCo shares cannot be offered through the proposed Spin-Out, and to shareholders who hold a small number of Foreign SpinCo shares. Instead, it will issue the affected Foreign SpinCo share to an independent trustee who will sell them in the open market and distribute the net cash proceeds to such ineligible shareholders.

- Subject to 10, Foreign PubCo will distribute the remaining outstanding shares in Foreign SpinCo pro rata to its shareholders under a scheme of arrangement on a proportionate basis.

Rulings

- S. 55(3)(b) ruling is premised on 10% or more of the FMV of the Foreign SpinCo shares not, at any time, during the course the series being derived from the DC Special Shares or TC Common Shares. For these purposes, any indebtedness of Foreign SpinCo will be considered to reduce the FMV of each property of Foreign SpinCo pro rata in proportion to the relative FMV of all property of Foreign SpinCo.

- No s. 86 ruling.

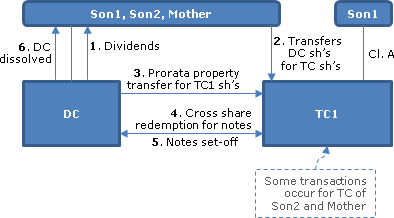

2013 Ruling 2013-0502921R3 - Split-Up Butterfly - Farm

Structure

The DC is a CCPC owned (as to both DC-Class A (common) and DC-Class D (pref)) by Son1, Son2 and Mother and which formerly had carried on a farming business. The farm (a.k.a., the "Lands") now is rented out to farmers, with the exception of the "Home Quarter," containing three residences which are rented out to Son1, Son2 and Mother (although Son1 still occupies his residence.) DC holds the "Patronage Reserves" as capital property (namely, membership equity of DC in various co-operatives from which DC purchased agricultural-related supplies for maintaining the Lands and carrying on its business and in respect of which DC is entitled to receive an annual patronage dividend, the amount, if any, of which depends on the level of DC's patronage for such year).

Purpose

To split-up DC between TCs (TC1 to 3) for the three shareholders.

Types of property

The investment property of DC comprises portfolio investments in publicly traded securities, the Lands (including the Home Quarter unless sold prior to the Distribution) "on the basis that they are currently being used by DC to generate income from property in the form of rent," and the Patronage Reserves "on the basis that they currently generate income from property for DC in the form of patronage dividends." Inventory and the remaining farm equipment will be classified as business property "on the basis that it is currently being used… to generate business income from its sale." Cash and term deposits are classified as cash or near-cash property.

Reorganization

- DC will pay a dividend (through issuing demand notes) to each of Son1, Son2 and Mother so as to entitle it to a refund of its RDTOH for that year and will designate such dividends as eligible dividends, and will also pay capital dividends to them, with the notes and shareholder loans then being repaid in cash.

- After having incorporated his or her respective TC (TC1 to 3) and subscribed for Class A voting participating shares, each of Son1, Son2 and Mother transfers his or her DC-Class A and DC Class-D shares to such TC in consideration for non-voting retractable Class C shares of TC, electing under s. 85(1).

- DC transfers pro rata portions of its three types of property (including the Home Quarter and farm equipment to the TCs as tenants-in-common if not yet sold) to the TCs in consideration for non-voting Class D redeemable retractable shares, electing under s. 85(1).

- Each TC redeems its Class D shares for demand promissory notes; and DC redeems its DC-Class D and DC-Class A shares for demand promissory notes, designating pro rata portions of its GRIP as eligible dividends under s. 89(14).

- The promissory notes are set-off.

- DC is dissolved.

Circularity comment

. After giving relatively standard butterfly rulings and rulings that the s. 84(3) deemed dividends arising on the redemptions by the TCs and DC in 4 will be subject to Part IV tax to the extent described in s. 186(1)(b), CRA noted that this "could give rise to what is referred to as a "circular" calculation of RDTOH," and stated that "the district taxation office at which each of the corporations files its T2 income tax return will have to be consulted in order to determine which corporation will receive the dividend refund and which corporation will be subject to the Part IV tax liability under paragraph 186(1)(b)."

2014 Ruling 2013-0498951R3 - Split-up Butterfly

A standard split-up butterfly for the pro rata division of the assets (mostly portfolio shares) of DC (a CCPC with no liabilities other than accrued professional fees) between TC1 for Brother and TC2 for Sister, followed by the winding-up of DC.

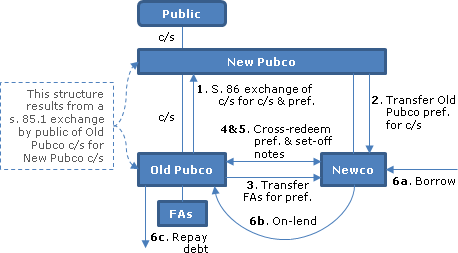

2013 Ruling 2013-0490341R3 - No-type of property spin-off butterfly

Preliminary

As a preliminary step under a plan of arrangement, the shareholders of Old Pubco (a Canadian public corporation dealing at arm's length with each shareholder) will transfer (in a s. 85.1 exchange) all their Old Pubco common shares to a newly-incorporated Canadian subsidiary of Old Pubco (New Pubco) in consideration for New Pubco common shares, and New Pubco will reduce the stated capital of its shares (in order to satisfy the solvency test for any future dividends).

Spin-off transactions

- The Old Pubco shares of New Pubco will be converted into New Common Shares (having two votes per share) and new Preferred Shares (which will be redeemable and retractable for the "Butterfly Proportion" of the old common shares of Old Pubco, subject to a price adjustment clause).

- New Pubco will transfer to a newly incorporated subsidiary ("Newco") the Old Pubco New Preferred Shares, in exchange for Newco Common Shares, electing under s. 85(1).

- Old Pubco will transfer to Newco the Spin-off Properties (being shares of various non-resident subsidiaries) in consideration for the issuance of the Newco Preferred Shares, electing under s. 85(1). "[T]he FMV of the property of Old Pubco will be determined as though there was only one type of property, as contemplated by subsection 55(3.02), on a net FMV basis."

- Newco will redeem "from Old Pubco" all of the issued and outstanding Newco Preferred Shares, and Old Pubco will redeem "from Newco" all of the outstanding Old Pubco New Preferred Shares, in each case in consideration for issuance of a non-interest-bearing demand promissory note. In each case, the resulting deemed dividend will be designated to be an eligible dividend.

- The two notes will be set off.

- New Pubco will draw down under the "New Pubco Multicurrency Credit Facilities" and use the proceeds to lend at a small spread to Old Pubco (under the "Old Pubco Internal Multicurrency Debt"), and Old Pubco will use such proceeds to pay off the "Old Pubco Multicurrency External Debt." "Simultaneously, Old Pubco will enter into an internal hedging contract ("Hedging Contract 2") with New Forco Holding 2 [included in the Spin-off Properties] to mitigate foreign exchange exposure in respect of the Old Pubco Internal Multicurrency Debt.

Rulings

- Standard butterfly rulings.

- Ruling re interest deductibility on the Old Pubco Internal Multicurrency Debt to the extent the Old Pubco Multicurrency Internal Debt does not exceed the PUC of the Old Pubco New Preferred Shares, determined immediately before the redemption."

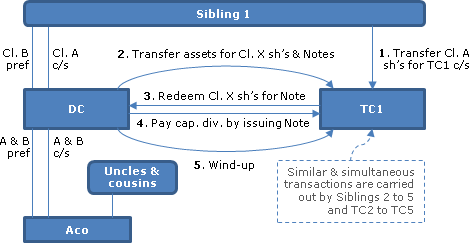

2013 Ruling 2013-0475681R3 - Family holding butterfly transaction

Facts

DC is a CCPC holding company whose assets consist of the shares of Aco (controlled by uncles, aunts and cousins), which are investment property as it does not have significant influence over it, and cash or near cash assets. All the Class B shares of DC, which are voting and non-participating, as well as the Class A shares, which are voting and entitled to discretionary dividends, are held by Sibling 1 to 5, except that Sibling5 holds her Class A shares through TC5. The Class B shares were issued prior to December 20, 2002, so that qualify as shares of a specified class notwithstanding their voting rights. "DC may pay dividends on the Class "A" shares of the capital stock owned by the current shareholders before the Proposed Transactions (such dividends not to exceed the income of DC for the current taxation year)."

Proposed transactions

- Each of TC1 through to TC4, which is solely owned by Sibling 1 to 4, respectively, will acquire the Class A Shares of the respective Sibling for treasury common shares utilizing s. 85.

- DC will transfer a proportionate share (based on the relative fair market value of the shares in its capital held by the particular TC): of its common shares and Class B shares of Aco, as well as its "Fund Units" to each of the five TCs in consideration for Class X preferred shares of that TC; of its Series A and B preferred shares of ACo to each TC in consideration for a non-interest-bearing Note1 of the respective TC; and of cash to each TC in consideration for a non-interest-bearing Note2 of the respective TC.

- Each TC will redeem its Class X preferred shares for a Note3.

- DC will pay a capital dividend on its Class A shares by issuing a Note DC-TC to each TC.

- On a winding-up of DC, it will distribute the Notes1 to 3 to the respective TC thereby paying off the DC-TC Notes and with the distributed Notes being extinguished, and with DC designating the resulting s. 88(2)(b) deemed dividend under s. 89(14), and with any dividend refund to DC being distributed on a pro rata basis.

Rulings

Inter alia on ss. 129(1.2), 55(3)(b) and 80.

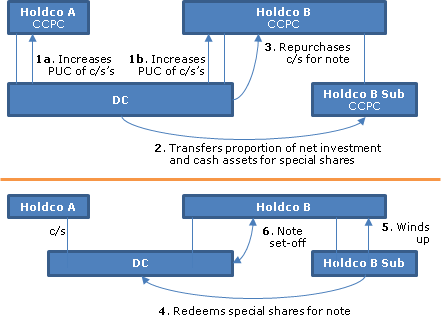

2013 Ruling 2012-0449611R3 - single-wing butterfly reorganization

Existing situation

DC, which is a CCPC beneficially owning rental real estate encumbered with mortgages (the "Buildings") and which carries on a specifed investment busines, has Holdco A and B as its (common) shareholders, who also hold shareholder advances and deal with each other at arm's length, and with Holdco B being the controlling shareholder of DC. In connection with the settlement of a lawsuit between Holdco A and its shareholders, and Holdco B and its shareholders, it was agreed that Holdco B would make a payment to the plaintiffs and that there would be a transfer of Buildings on a single-wing butterfly basis to Holdco B.

Proposed transactions

- DC will increase the stated capital of its common shares by the applicable multiple of its RDTOH at the end of the taxation year arising from Holdco A's acqusisition of conrol referred to in 3 below, with such increase not exceeding the safe income on hand attributable to the DC common shares of Holdco A and Holdco B at the safe-income determination time. Holdco A and Holdco B will make s. 55(5)(f) designations in respect of the resulting deemed dividend.

- DC will transfer a proportionate share of its two types of property (cash and near cash; and investment property, namely, the Buildings and related assets) on a net asset butterfly basis under s. 85(1) to a newly-incorporated subsidiary of Holdco B (Holdco B Sub) in consideration for the assumption of liabilities and for Holdco B Sub Special Shares (which will carry more than 10% and less than 50% of the votes for all Holdco B Sub shares), with Holdco B Sub thereby being connected with DC; the shareholder loans will be considered current liabilities for this purpose;

- DC will purchase for cancellation all of the DC common shares held by Holdco B in consideration for issuing a Note, which will be accepted as absolute payment; no s. 256(9) election will be made respecting the resulting acquisition of control of DC by Holdco A.

- Holdco B Sub will redeem all of the Holdco B Sub Special Shares held by DC in consideration for issuing a Note, which will be accepted as absolute payment.

- Holdco B Sub will be wound–up – and then dissolved.

- The two Notes will be set-off.

Purposes of transactions

58. The purpose of the PUC increase [in 1]… is to enable DC to receive a dividend refund equal to the amount of DC's RDTOH at the end of the year that will end immediately before the acquisition of control of DC by Holdco A….

60. The purpose for Holdco B incorporating Holdco B Sub…is to avoid circularity in the calculation of DC's RDTOH and Part IV tax, that would otherwise occur if the Distribution Property were transferred directly to Holdco B by DC.

61. The purpose for DC not filing a subsection 256(9) election [see 3]… is to ensure that the dividend refund that DC will obtain, arising on the PUC increase [in 1]… will occur in the taxation year of DC that will end immediately before the acquisition of control of DC by Holdco A….

Rulings

Standard butterfly rulings.

2012 Ruling 2012-0460811R3 - Public Company Spin-Off Butterfly

Under the proposed transactions for a spin-off butterfly of Spinco by DC (a public corporation and principal business corporation as defined in s. 66(15)):

- no dissent rights were exercised

- Spinco, which is a taxable Canadian corporation and whose common shares have been conditionally accepted for listing but which will not issue any shares until the time of transfer to it below of the DC Butterfly Shares, will elect to be a public corporation by filing the T2073 prescribed form

- each DC shareholder will exchange each of its DC common shares for one DC New Common Share (having the same rights as the old common shares except that the DC New Common Shares will give the holders thereof the right to vote, to the exclusion of any other class of shares of DC, for the election of directors at any meeting of shareholders called for that purpose) and one DC Butterfly Share (which will be non-voting and redeemable and retractable for the "Butterfly Proportion" of the fair market value of an old DC common share immediately before such reorganization)

- each DC stock option holder will exchange its options for new DC stock options and Spinco stock options ("The issuance by Spinco of the Spinco Stock Options will be in anticipation of the [butterfly] distribution ... and will form part of the non-share consideration relating to such transfer." – para. 29)

- each DC Butterfly Shares will be transferred to Spinco in consideration for one Spinco common share, with the Spinco common shares being listed on a designated stock exchange

- the net FMV of each of the three types of property of DC will be determined on a consolidated basis (and where the property of DC is a share of a corporation over which DC has a significant influence, the net FMV of the share of the particular corporation will be multiplied by the proportion that the net FMV of that type of property of the particular corporation is of the net FMV of all the property of the particular corporation - and following the allocation of current liabilities to each cash or near cash property, any remaining net FMV of any accounts receivable, inventories and prepaid expenses of a particular corporation will be reclassified as business property and excluded from cash or near cash property, to the extent that such property will be collected, sold or used by the particular corporation in the ordinary course of the business to which such property relates)

- DC will transfer to Spinco each transferred asset such that following the transfer the net FMV of each type of transferred property will approximate the Butterfly Proportion; and in consideration therefor Spinco will issue the Spinco Stock Options and Spinco Redemption Shares; DC and Spinco will make a joint s. 85(1) election

- Spinco and DC will redeem the Spinco Redemption Shares and DC Butterfly Shares for redemption notes (making a s. 89(14) designation respecting the resulting deemed dividend), and will each satisfy its note by transferring the other note to its debtor

Rulings:

- s. 86 rulings re exchange of DC common shares for new common shares and DC Butterfly Shares

- s. 85.1(1) rulings re transfer of DC Butterfly Shares to Spinco

- cross-cancellation of notes will not give rise to gain or forgiven amounts

2012 Ruling 2011-0425441R3 - Cross Border Butterfly

Overview

A non-resident public company (Foreign Pubco) will be spinning off Business A to its shareholders, to be accomplished by a dividend-in-kind of its shares of Foreign Spinco (also non-resident) to its shareholders. Business B will be retained. Preliminarily to this spin-off, an indirect Canadian subsidiary of Foreign Pubco (Canco – which is the distributing corporation) will transfer the Canadian business relating to Business B as well as related foreign subsidiaries held directly (Forsub) or through a partnership (Forlp) and a partner thereof (Canco Sub 4) to the transferee corporation (TCo – a ULC). This will be accomplished through a direct transfer of the Newco holding company for such assets (Newsub) to TSub (a subsidiary of TCo), with TSub then being wound up into TCo. TCo (through transactions which are heavily redacted – see perhaps para. 122) will be indirectly transferred to Foreign Pubco, whereas Canco will become an indirect subsidiary of Foreign Spinco.

Indemnity – effect on net value of types of property

In order to accomplish the butterfly spin-off of Canco's portion of Business B, Canco will first transfer such assets to Newsub under s. 85(1). The letter states (para. 61):

For purposes of applying the types of property classification in regards to Canco and Newsub, any liability that is assumed by Newsub, but in respect of which Canco provides an indemnity to Newsub, will, to the extent of that indemnity, be treated as a liability of Canco and not of Newsub, and any liability that is retained by Canco, but in respect of which Newsub provides an indemnity to Canco, will, to the extent of that indemnity, be treated as a liability of Newsub and not of Canco.

Cash adjusting payment

XXX days after the transfer of Newsub to TSub, Canco will transfer any additional cash or near cash assets to TCo as is required to satisfy the requirement for the butterfly percentage for the transferred net business, and cash and near cash, assets being approximately the same (there being no investment assets) (para. 84.1).

2012 Ruling 2011-0416001R3 - Split-up butterfly

Structure

The DC is a CCPC whose only significant assets is shares (being investment property) of Pubco (a Canadian public company over which it does not have significant influence - whose standard definition referred to s. 3051.04 of the Private Enterprises standards, or IAS 28 for IFRS). Dividends on its Pubco shares are subject to Part IV tax. The TCs are numerous CCPCs controlled by 3rd or 4th generation family members. DC is not connected under s. 186(4) with each TC, which holds less than 10% of the voting shares of DC and deals at arm's length with most of the other TCs.

Reorganization

DC transfers pro rata portions of its Pubco shares and incidental assets to the TCs for preferred shares having nominal stated capital, which are redeemed for promissory notes. DC reduces the stated capital of its shares to a nominal amount, and then assigns the promissory notes to the TCs in the course of its winding-up. DC also distributes the dividend refund, generated on the s. 84(2) dividends deemed to arise on its winding-up, pro rata to the TCs.

Before going on to give relatively standard butterfly rulings and rulings that both the s. 84(3) deemed dividends arising on the redemption of the TC preferred shares and the s. 84(2) dividends arising on the winding-up of DC will be subject to Part IV tax and generate a dividend refund, the letter states (para. 70) that the purpose for the nominal stated capital of the DC shares and TC preferred shares is:

to ensure that each of the TCs and DC's respective dividend refund under subsection 129(1) and respective Part IV tax liabilities under paragraph 186(1)(a) (all in respect of the winding-up dividend arising on the wind-up of DC...and the dividends arising on the redemptions of the TC Preferred Shares of the TCs...), will approximately be equal to each other.

2012 Ruling 2012-0439381R3 - Cross-border spin-off butterfly

Preliminary transactions

. The transactions entail the spin-off by Foreign Pubco of Foreign Spinco Parent including a Canadian business which will have been butterflied (as described below) from DC to TC, a Canadian subsidiary of Foreign Spinco Parent. Accordingly, preliminary transactions are effected to indirectly transfer the "Spin-off Business" to Foreign Spinco Parent. First, the shares of DC will be distributed by its immediate non-resident parent (DC Parent), through a dividend in kind to the shareholder of DC Parent, and thereafter is distributed though dividends-in-kind by further intermmediate corporations, to Foreign Pubco. Furthermore, a "demerger transaction" (perhaps the UK equivalent of a spin-off transaction) is effected pursuant to which DC Parent transfers its portion of the Spin-off business to a subsidiary of its parent (Forco8), and similar demerger transactions are carried out to indirectly transfer the assets of the Spin-off business upstream through a succession of levels of Foreign Spincos and Forcos, followed by further distributions through a succession of dividends in kind of such assets to Foreign Spinco Parent.

DC and s. 86 reorganization

Each common share of DC will be changed into one redeemable retractable non-voting DC preferred shares (a DC New Preferred Share1) and one DC New Common Share.

Three-Party Share Exchange

In the context of a three-party transfer agreement (the "Three-Party Share Exchange") between Foreign Pubco, Foreign Spinco Parent and TC (a newly-incorporated Canadian subsidiary of Foreign Spinco Parent):

a) TC will agree to pay the purchase price for DC New Preferred Shares1 transferred to it by Foreign Pubco as described in para. (b) below by issuing TC Common Shares to Foreign Spinco Parent;

b) Foreign Pubco will agree to pay the purchase price for the common shares issued to it by Foreign Spinco Parent as described in para. (c) below by transferring all of the DC New Preferred Shares1 to TC; and

c) Foreign Spinco Parent will agree to pay the purchase price for the TC Common Shares issued to it by TC as described in para. (a) above by issuing common shares to Foreign Pubco (para. 66).

Permitted exchange

Immediately before the transfer of Newco common shares by DC to TC described below, the common shares of Foreign Spinco Parent (viewed as the "acquiror") owned by Foreign Pubco (viewed as the "participant") will have a fair market value that accords with the formula in (b)(iii) of the "permitted exchange" definition (para. 71).

Drop-down of Canadian Spin-off Business to Newco

DC will transfer its assets of the Spin-off Business to a newly-incorporated subsidiary (Newo) in consideration for assumption of liabilities and the issuance of common shares (para 74-75). A s. 20(24) election may be made. The undepreciated capital cost of depreciable property will be pro-rated.

Three types of property

Immediately before the drop-down transaction referred to above the property of DC will be classified as three types of poroperty under a net asset butterfly approach. Following the allocation of current liabilities to cash or near-cash property in accordance with the usual methodology, provided that the net FMV of the cash or near-cash property of such corporation is positive, any remaining net FMV of any accounts receivable, trade receivables, inventories and prepaid expenses of such corporation will be reclassified as business property of such corporation and excluded from the net FMV of the cash or near-cash property, to the extent that such property will be collected, sold, used or consumed in the ordinary course of business to which such property relates (para. 73(b)). The net fair market value of each type of property transferred to Newco will be such as to satisfy the proportionality test in the distribution definition.

Butterfly distribution

. DC transfers its common shares of Newco to TC in consideration for TC preferred shares (para. 80).

Cross-redemption

TC will redeem its preferred shares, and DC will redeem the DC Preferred Shares1, in each case for a demand promissory note. Immediately thereafter, the principal amounts owing thereunder will be set-off against each other.

Spin-off by Foreign Pubco

Foreign Pubco will distribute all its shares of Foreign Spinco Parent to its shareholders as a dividend-in-kind.

Rulings

. S. 55(2) will not apply to the deemed dividends arising on the cross-redemptions (referred to in Ruling D) provided that:

10% or more of the FMV of the Foreign Spinco Parent common shares that Foreign Pubco owns was not, at any time during the course of any series of transactions or events that includes the dividends described in Ruling D (a) and (b), derived from the DC New Preferred Shares1 or the TC Common Shares. (Ruling F)

2012 Ruling 2011-0431101R3 - Cross-border spin-off butterfly

Background

Foreign Pubco has announced that it will divide itself into three separate publicly traded companies by making a distribution by way of dividend of shares of Foreign Spinco 1 and Foreign Spinco 2 to its shareholders (the "Spin-out"). Foreign Spinco 1 will indirectly hold the Foreign Spin Business (para. 28). Various transactions (para. 102 to 121) to separate the Foreign Spin Business from the Foreign Keep Business, and arrange for the Foreign Spin Business to be held by Foreign Spinco 1, will occur before the Canadian butterfly transactions described below occur (entailing the separation of the DC Spin Business from the DC Keep Business) with (somewhat counter-intuitively) DC being included in what will be spun out as part of Foreign Spinco 1, and TC being retained as an indirect subsidiary of Foreign Pubco.

DC and s. 86 reorganization

The only issued and outstanding shares of DC, a private corporation and a taxable Canadian corporation (and, per para. 149, a deemed specified financial institution), are common shares which currently are owned by Foreign Sub 2, but after the preliminary transactions referred to above, they will be owned by Foreign Sub 1 (para. 118). DC holds foreign subsidiaries (the A Co and E Co and subsidiaries thereof). Each common share of DC will be changed into one redeemable retractable non-voting DC special share and one DC New Common Share.

Permitted exchanges/Three-Party Share Exchange

Foreign Sub 1 will concurrently make the following transfers of its shares of DC (which will not be taxable Canadian property):

(i) transfer all the DC Special Shares to TC, a newly-incorporated private corporation subsidiary of Foreign Sub 1 (para. 126(a)) in consideration for the issue of common shares of TC; and

(ii) transfer all the DC New Common Shares to Foreign Sub 15, a newly-incorporated LLC subsidiary of Foreign Spinco 1 which, in turn will be a non-Canadian subsidiary of Foreign Sub 1 (para. 126(b)).

In connection with the transfer in (ii) above, Foreign Sub 1, Foreign Sub 15, and Foreign SpinCo 1 will enter into a three-party agreement (the "Three-Party Share Exchange"), whereby:

(a) Foreign Sub 15 will agree to pay the purchase price for the DC Common Shares transferred to it by Foreign Sub 1 by issuing membership interests in the capital of Foreign Sub 15 to Foreign SpinCo 1 having an aggregate FMV at that time equal to the aggregate FMV of the DC Common Shares so transferred to it by Foreign Sub 1 as described in [para. (b) below]...;

(b) Foreign Sub 1 will pay the purchase price for the Foreign SpinCo 1 Common Shares issued to it by Foreign SpinCo 1 as described in [para. (c) below], by transferring all of the DC Common Shares to Foreign Sub 15; and

(c) Foreign SpinCo 1 will agree to pay the purchase price for the membership interests in Foreign Sub 15 by issuing common shares to Foreign Sub 1 having an aggregate FMV at that time equal to the aggregate FMV of the membership interests in Foreign Sub 15 so issued by Foreign Sub 15 to Foreign SpinCo 1 described in para. (a) above.

Immediately before the butterfly "distribution" by DC described below, the common shares of Foreign Spinco 1 (viewed as the "acquiror") owned by Foreign Sub 1 (viewed as the "participant") will have a fair market value that accords with the formula in (b)(iii) of the "permitted exchange" definition (para. 130). Immediately before that "distribution", the common shares of Foreign Spinco 1 (viewed as the "acquiror") owned by Foreign Sub 1 (viewed as the "participant") also will have a fair market value that accords with the formula in (b)(iii) of the "permitted exchange" definition (para. 131).

Consolidated look-through/leased property as business asset

In applying the consolidated look-through approach to the property of DC (under a net asset butterfly approach), it will not be considered to have any property other than business property (para. 133, 136). In this connection, a leasehold interest which DC is subleasing to a third party will be considered to be a business property (para. 132(h)). DC had recently acquired this property as a result of acquiring another Canadian corporation (Canco 11), winding-up Canco 11, transferring the personnel at the facility to other leased premises of DC, and then subleasing to the third party for the duration of the lease:

The entering into of the sublease was motivated entirely by DC's desire to reduce to the extent possible, the cost of the lease obligation assumed on the liquidation of Canco 11. Controlling lease costs is a normal business transaction for DC as that entity has approximately XX leases for various premises across Canada and routinely reviews its leased space and costs (para. 73).

Following the allocation of current liabilities to cash or near-cash property of a corporation in accordance with the usual methodology, provided that the net FMV of the cash or near-cash property of such corporation is positive, any remaining net FMV of any accounts receivable, trade receivables, inventories and prepaid expenses of such corporation will be reclassified as business property of such corporation and excluded from the net FMV of the cash or near-cash property, to the extent that such property will be collected, sold, used or consumed in the ordinary course of business to which such property relates.

Amounts capitalized under SAB 101 (an SEC Bulletin on revenue recognition) will not be treated as property (para. 132(j)). In particular, "any amounts collected from customers and set up as deferred revenue under SAB 101 will not be considered a liability as there is no legal obligation to repay the amount or provide further services" (para. 134(c)(viii)).

Butterfly distribution

. DC transfers assets to TC including A Co and E Co (the Foreign Subsidiaries of CFAs) in consideration for the assumption of liabilities and the issuance by TC of preferred shares, so that the proportion of the net business assets received by TC approximates the ratio of the FMV of the DC Special Shares to the FMV of all the issued and outstanding DC shares. An s. 85(1) election is made (but with the reference in s. 85(1)(e)(i) to undepreciated capital cost of depreciable property of DC being interpreted as referring to its proportionate UCC (para. 139)). Payments made by DC to TC respecting the assumption by TC of deferred revenue obligations will be considered part of the property transfer for these purposes. A related s. 13(24) election will be made.

Cross-redemption

TC will redeem its preferred shares, and DC will redeem the DC Special Shares, in each case for a demand promissory note. Immediately thereafter, the principal amounts owing thereunder will be set-off against each other.

Refinancing

Amounts owing by DC to related parties that were not assumed will be repaid or refinanced. The debt assumed by TC may also be repaid or refinanced.

Spin-off by Foreign Pubco

Foreign Sub 1 will contribute its shares of Foreign Sub 3 to Foreign Spinco 1, and Foreign Sub 1 will then distribute all its shares of Foreign Spinco 1 to Foreign Pubco. Foreign Pubco will distribute all its shares of Foreign Spinco 1 (as well as all its shares of Foreign Spinco 2, which holds assets that were not involved in the butterfly reorganization) to its shareholders as a dividend-in-kind.

Rulings/Opinions

S. 55(2) will not apply to the deemed dividends arising on the cross-redemptions (referred to in Ruling D) provided that:

10% or more of the FMV of the Foreign SpinCo 1 Common Shares was not, at any time, during the course of the series of transactions or events that includes the dividends described in Ruling D, derived from the DC New Common Shares or derived from the membership interest in Foreign Sub 15....For the purposes of subclause 55(3.1)(b)(i)(A)(II), in determining whether 10% or more of the FMV of the common shares of Foreign SpinCo 1 was derived from the DC New Common Shares that Foreign Sub 15 owns or derived from the membership interest in Foreign Sub 15 that Foreign SpinCo 1 owns, as described in Ruling F(I) above, any indebtedness of Foreign SpinCo 1, that is not a secured debt and that is not a debt related to a particular property, will be considered to reduce the FMV of each property of Foreign SpinCo 1 (or indirectly the FMV derived from DC Common Shares owned by Foreign Sub 15) pro rata in proportion to the relative FMV of all property of Foreign SpinCo 1. (Ruling F)

Interest on DC's retained debt will be deductible (subject to the more usual qualifications) to the extent that its aggregate amount does not exceed the contributed capital and accuulated profits of the DC Special Shares which were redeemed. (Ruling K)

DC and TC will be a predecessor corporation and acquiring corporation for purposes of Reg. 5905(5) in respect of the CFAs acquired by TC. (Ruling L)

The Finance Comfort Letter recommends changes to the draft s. 212.3 rule to avoid a deemed dividend to DC on its transfer of the CFAs to TC.

2012 Ruling 2011-0413661R3 -

The distributing corporation ("DC") is controlled by a financial institution ("Owner 1" - perhaps a credit union) and its only assets are a partnership interest in a limited partnership ("LP") together with a portion of the common shares of the general partner thereof. The balance of the interests in LP are held by another credit union. LP apparently has an asset management business.

The assets of DC (i.e., essentially, LP) are divided among its shareholders (all of them non-public corporations, including Owner 1) utilizing conventional split-up butterfly mechanics, so that on completion, DC has been wound-up into the transferee corporation (a "TC") of Owner 1 and all the TCs (including the TC of Owner 1) have been wound up.

The ruling states that DC is not expected to have any business property. A preliminary transaction is for the current liabilities of DC to be paid off through the application of regular partnership distributions received from LP.

2011 Roundtable Q. , 2011-0399401C6 F

where two siblings are the shareholders of two transferee corporations which are to receive two life insurance policies taken out by the distributing corporation on the life of each sibling to fund the redemption of the other's shares on the other's death, the cash surrender value of each property would be treated as a cash or near cash asset. The excess of the fair market value over the cash surrender value potentially may be treated as an investment asset (see 2010-0358061R3), although CRA may be prepared to be flexible respecting the classification of such excess. CRA would accept that each type of property transferred may be determined on a net basis (thereby using liabilities of the DC), although such liabilities would have to be allocated following a predetermined pattern.

15 December 2009 Ruling 2008-0304371R3

in a single-wing butterfly of a company whose assets consisted of cash and cash equivalents, tenant receivables and a revenue producing rental property, the revenue-producing properties and prepaid rent were considered business property and loans receivable from certain Holdcos, which had no specified terms of repayment, were considered to be near cash assets.

After the allocation of current liabilities to cash and near cash assets, "the remaining net fair market value, if any, of any amounts receivable and prepaid expenses of Opco (other than the Prepaid Rent) will be reclassified as business property and excluded from cash or near-cash property, to the extent that such property will be collected or used in the ordinary course of the business to which such property relates" (para 66(b)).

Furthermore, "following such allocation of liabilities...it is not expected that Opco will have any cash or near cash property...."

2008 Ruling 2007-024122

preliminarily to butterfly transactions involving a CCPC (DC) whose individual shareholders are implementing a settlement agreement in respect of an oppression remedy brought by some of the individual shareholders (H to M, who act as a group): Mr. A (a major shareholder of DC), Mrs A and Mr G are paid retiring allowances; and various of the individual shareholders who are not specified shareholders elect to cash out substantially all their interest in DC by electing to receive a substantial cash dividend (including a capital dividend) on their shares (representing most of the value of those shares) with those shares then being converted into Class B Freeze shares having a nominal value.

In the first gross asset butterfly transaction, DC transfers a portion of each of its three types of property: to a subsidiary (Subco A) of a TC for Mr A (Transferee A), with Subco A then being wound up into Transferee A; and to a TC for G to M (Transferee Z). DC then is dissolved. In the second gross asset butterfly, Transferee Z (now referred to as DC2) transfers a portion of each of its three types of property to TCs for each of its individual shareholders (or a TC (Transferee N) with nominal value for the shareholders of DC who elected to be cashed out).

The liabilities assumed on the butterfly transfers to and by Transferee Z include contingent environmental liabilities (para. 37, 80).

2008 Ruling 2007-025168 -

there are two proposed successive butterfly reorganizations in which DC, which is a CCPC whose assets include development real estate, mortgage receivables and portfolio investments and which is owned by a testamentary trust, a subsidiary ("Newco 1") of the estate and a Mr. B, transfers a portion of its assets on a butterfly reorganization to a corporation ("Transferee A") owned by the same shareholders, and Transferee A then transfers a portion of its assets on a butterfly reorganization to a corporation ("Transferee C") owned by Mr. B.

On both butterfly distributions, the amount of the cash to be transferred to Transferee A or C will be determined within X days of the transfer of the other property to such transferee corporation and an adjustment will be made as required to the amount of cash transferred (para. 41, 53).

At or around the time of the above transactions, and following the exchange by the trust of its exisiting shares of DC for two new classes of shares, one of which will be retained by it and the other transferred by it on a share-for-share exchange to Transferee A, DC will pay in cash a capital dividend on the shares retained or to be retained by the trust.

2007 Ruling 2006-021575

In a net equity butterfly, after the current liabilities are allocated to cash and near-cash property, "any remaining net FMV of any accounts receivable , trade receivables, inventories and prepaid expenses of Canco will be reclassified as business property and excluded from the cash or near-cash property, to the extent that such property will be collected, sold or used in the ordinary course of the business to which such property relates." (para 35(b)(ii))

Business property did not include (and investment property included) assets any income from which would be income from a specified investment business. (para. 33)

2006 Ruling 2006-019750

Vacant land of a distributing corporation used as a parking lot for a facility owned by a subsidiary, and vacant land owned by the distributing corporation for the purpose of constructing a facility, will be considered to be capital property and business property.

2006 Ruling 2006-018106

The cash and near cash property of DC Amalco includes funds in an escrow bank account which, pursuant to the relevant loan agreement, DC Amalco is under an unconditional commitment to expend on property taxes; and its business property includes funds in escrow bank accounts which, pursuant to the relevant loan agreement, DC Amalco is under an unconditional commitment to expend on future acquisitions of furniture, fixtures and equipment (paras. 3 and 22).

2004 Ruling 2003-004375 -

Where TC receives a butterfly property from DC on spin-off butterfly, the sale by TC of some of the butterflied property back to DC after the spin-off butterfly (where such sale will not exceed the limitation in s. 55(3.1)(c)), will not affect the pro rata distribution rule.

2002 Ruling 2002-014073 -

sequential butterfly. In each butterfly, "to the extent a portion of the cash or near cash property of the [DC] Group is committed by the [DC] Group in order to fund the acquisition of a business property (that is to be acquired regardless of the Proposed Transactions), such cash or near cash property will be classified as business property." (para.52(g) and 73(f)) "[T]he net FMV of all accounts receivable, inventory and prepaid expenses of [DC]'s that are initially classified ...as cash or near cash property that will relate to a business that will be carried on by the [TC Groups] and that will be collected or consumed in the ordinary course of such business, will then be reclassified as business property...." (para. 53(a)(ii) and (b)(ii)), 62(a)(ii) and (b)(ii))

2000 Ruling 2000-004066 -

No look-through approach was applied to holdings in public corporation where each holding was less than 20% and neither the taxpayer nor persons related to it were on the board or participated in the decision-making processes of the investees.

1999 Ruling 3-990262

Where the distributing corporation or a look-through corporation has limited partnership interests, the consolidated look-through approach will be used only in cases where such holder on a consolidated basis can exercise significant influence over the affairs of the partnership. (para. 43(a)).

Since space that was subleased was generally either previously occupied or potentially needed for future expansion, the entire leasehold interest will be classified as business property (para. 43(n)(ii)).

Certain "look-through" entities ... have in the past acquired land for future expansion of the business operations. In some circumstances, the expansion plans have been abandoned and such vacant lands are currently held for resale pending of the locating of an acceptable purchaser. Since in all the circumstances, the vacant land was initially acquired for future expansion and either continues to be held for such expansion or for resale, these interests in vacant lands will be classified as "business property" (para. (n)(v)).

1998 Ruling 3-980180

In determining the net fair market value of property of the distributing corporation, liabilities should be valued at their principal amount rather than their fair market value (per summary).

Where the terms of debt require payments to a sinking fund, the liability arising from that debt should be allocated first to the sinking fund assets (per summary).

An amount of cash or near cash assets equal to the amount of unconditional purchase commintments to fund the acquisition cost of business property which will be acquired in the ordinary course of business regardless of whether the butterfly distribution will occur, is classified as business property (para. III.27). Conversely, where there are unconditional commitments to sell business property in the ordinary course of business, an amount equal to the sales proceeds to be received will be classified as cash or near cash property (para. III.28).

Intellectual property which has been primarily developed or acquired for application and use in the business activities of the group is classified as business property notwithstanding that there is incidental licensing of the property (para. III.30).

Real property interests consisting of redundant space within structures which are used, or held for use, in the business activities wthin the group, and real property interests whcih consist of residential properties acquired from relocated employees, are classified as business property (para. III.31).

Where a subsidiary has a net FMV of cash or near cash property of -$200, and a net FMV of business property of $1,200 and a net FMV of investment property of nil, and if the FMV of the shares and debt of the corporation are $900, then the amount added to the consolidated net FMV of the distributing corporation cash or near cash property and net business property will be -$180 and $1,080, respectively (para. III.23.(3)).

1998 Ruling 3-980097

sales proceeds, in the form of cash and a non-convertible note receivable, which DC received on the sale of its interests in [unspecified assets] were treated as business assets because DC directly or indirectly entered into unconditional commitments to use the proceeds to acquire business assets including corporations over which it would exercise significant influence.

1996 Ruling 3-963259

Vacant land held for development, which was capital property, was categorized as investment property. Any tax accounts, such as the balance of any RDTOH account or capital dividend account would not be considered to be property.

Permitted Exchange

Administrative Policy

2012 Ruling 2011-0431101R3 - Cross-border spin-off butterfly

As preliminary transactions to a butterfly distribution by DC, which is owned by a non-resident subsidiary (Foreign Sub 1) of a non-resident publicly-traded corporation (Foreign Pubco), each common share of DC will be changed into one redeemable retractable non-voting DC special share and one DC New Common Share.

Permitted exchanges/Three-Party Share Exchange

Foreign Sub 1 will concurrently make the following transfers of its shares of DC:

(i) transfer all the DC Special Shares to TC, a newly-incorporated private corporation subsidiary of Foreign Sub 1 (para. 126(a)) in consideration for the issue of common shares of TC; and

(ii) transfer all the DC New Common Shares to Foreign Sub 15, a newly-incorporated LLC subsidiary of Foreign Spinco 1 which, in turn will be a non-Canadian subsidiary of Foreign Sub 1 (para. 126(b)).

In connection with the transfer in (ii) above, Foreign Sub 1, Foreign Sub 15, and Foreign SpinCo 1 will enter into a three-party agreement (the "Three-Party Share Exchange"), whereby:

(a) Foreign Sub 15 will agree to pay the purchase price for the DC Common Shares transferred to it by Foreign Sub 1 by issuing membership interests in the capital of Foreign Sub 15 to Foreign SpinCo 1 having an aggregate FMV at that time equal to the aggregate FMV of the DC Common Shares so transferred to it by Foreign Sub 1 as described in [para. (b) below]...;

(b) Foreign Sub 1 will pay the purchase price for the Foreign SpinCo 1 Common Shares issued to it by Foreign SpinCo 1 as described in [para. (c) below], by transferring all of the DC Common Shares to Foreign Sub 15; and

(c) Foreign SpinCo 1 will agree to pay the purchase price for the membership interests in Foreign Sub 15 by issuing common shares to Foreign Sub 1 having an aggregate FMV at that time equal to the aggregate FMV of the membership interests in Foreign Sub 15 so issued by Foreign Sub 15 to Foreign SpinCo 1 described in para. (a) above.

The ruling letter states that, immediately before the butterfly "distribution" by DC described below, the common shares of Foreign Spinco 1 (viewed as the "acquiror") owned by Foreign Sub 1 (viewed as the "participant") will have a fair market value that accords with the formula in (b)(iii) of the "permitted exchange" definition (para. 130). Immediately before that "distribution", the common shares of Foreign Spinco 1 (viewed as the "acquiror") owned by Foreign Sub 1 (viewed as the "participant") also will have a fair market value that accords with the formula in (b)(iii) of the "permitted exchange" definition (para. 131).

Safe Income Determination Time

See Also

Les Placements E&R Simard Inc. v. The Queen, 97 DTC 1328 (TCC)

On September 10, 1988, the taxpayer transferred its assets to a subsidiary ("Alimentation 1988") in consideration for a demand promissory note and 506,125 Class B shares having a redemption value of $1 per share and nominal paid-up capital. 151,125 of the Class B shares were redeemed in the fiscal years of Alimentation 1988 ending on May 31, 1990, 1991 and 1992.

In finding that the redemptions did not occur as part of the same series of transactions that included the 1988 sale, Tardiff TCJ. noted that they did not occur close in time to the first transaction, the transactions were not interdependent in the sense that there was a real possibility that Alimentation 1988 might never have redeemed the shares, and the fundamental objective underlying the 1988 transaction was for one of the two principals of the taxpayer to retire from the business of the taxpayer. The financial objective of converting, at some time, the Class B shares into cash was secondary. Accordingly, when the shares were redeemed, the relevant time for determining the safe income of Alimentation 1988 under former s. 55(2) was subsequent to September 10, 1988.

Subsection 55(2) - Deemed proceeds or capital gain

Cases

Ottawa Air Cargo Centre Ltd. v. The Queen, 2007 DTC 661, 2007 TCC 193, aff'd 2008 DTC 6177, 2008 FCA 54

Lamarre J. rejected the taxpayer's submission that deemed dividends received by the taxpayer were "subject to" Part IV tax in the sense that the taxpayer could have remitted Part IV tax on those taxable dividends and thus would have been entitled to a refund of Part IV tax. The taxpayer, in fact, did not do this and instead applied non-capital losses against an assessment of Part IV tax when it was made by the Minister on the basis that s. 55(2) did not apply to the deemed dividends. Lamarre J. found (at para. 21) that "the requirement of an actual refund of Part IV is mandatory for the dividend to be re-characterized as a capital gain under subsection 55(2)".

The Queen v. VIH Logging Ltd., 2005 DTC 5095, 2005 FCA 36

Cash dividends paid by a corporation ("Old VIH") to its parent (the taxpayer) in February 1993 came out of safe income of Old VIH given that the computation of Old VIH's safe income included significant income that it had earned after its last fiscal year end (March 31, 1992) and before the date of payment of the dividends. Sharlow J.A. stated (at p. 5101) that

"It does no violence to the language of subsection 55(2) to interpret the phrase 'before the commencement of the series of transactions' to mean 'immediately before the commencement of the series of transactions', rather than 'as of the end of the fiscal year ending before the commencement of the series of transactions', as the Crown contends."

In addition, it was open to the trial judge to find that a stock dividend paid shortly after the payment of the cash dividends, and which reduced the capital gain on a subsequent sale of the shares Old VIH by approximately $45,000, did not result in a significant reduction of the capital gain realized on such sale in the context of transactions which involve dividends totaling over $1.7 million.

Canutilities Holdings Ltd. v. The Queen, 2004 DTC 6475, 2004 FCA 234

The two taxpayers, which were subject corporations, indirectly sold their investment in another public corporation ("ATCOR"). This was accomplished by their common shares of ATCOR being exchanged on the amalgamation of ATCOR with a newly incorporated subsidiary of a related corporation for Class A or B non-voting redeemable shares of the amalgamated corporation having a paid-up capital approximating the respective adjusted cost base of their ATCOR common shares, with the special shares then being redeemed. The Part IV tax payable on the deemed dividends arising on this redemption was refunded because of normal-course dividends paid by the taxpayers to their shareholders that year (and, in one case, the following year).