Subsection 246(1) - Benefit conferred on a person

Cases

Les Consultants Pub Création Inc. v. The Queen, 2008 DTC 6610, 2008 FCA 60, aff'g Massicotte v. The Queen, 2006 TCC 618

The taxpayer wholly owned a corporation ("Amadéus") which, in turn, wholly owned another corporation ("Pub Création"), and the taxpayer was also the president and director of Pub Création. He assigned a $240,000 debt to Pub Création in exchange for a $240,000 "employee advance." As the debt which he assigned was essentially worthless, the Minister included $239,000 in the taxpayer's income. By the Tax Court trial, the position of the Minister (consistent with the pleadings, which did not refer to s. 6(1)(a)) was that this amount was included in the taxpayer's income under s. 246(1), on the basis that Amadéus had indirectly conferred a benefit on the taxpayer by arranging for the debt assignment at an inflated value, and such benefit would have been included in the taxpayer's income under s. 15(1) if Amadéus had paid this benefit directly to the taxpayer. The Tax Court found that the amount was included in the taxpayer's income under s. 6(1)(a), but found in the alternative that the Minister's position was correct.

The taxpayer argued that, because the benefit "could" have been included under s. 6(1)(a), the Minister lost the right to include the benefit in income under s. 246(1), which only applies "to the extent that [the benefit] is not otherwise included in the taxpayer's income ... under Part I." Before dismissing the taxpayer's appeal, Noël J.A. stated (at para. 25):

The question the TCC judge should have asked was not whether the benefit "could be included" under paragraph 6(1)(a), but rather whether the value of the benefit was "included" in computing Mr. Massicotte's income under paragraph 6(1)(a) or any other provision in Part I. While subsection 246(1) is generally used as an alternative basis, nothing prevents the Minister from relying on this provision as the sole basis of assessment when the circumstances require.

The Queen v. Kieboom, 92 DTC 6382 (FCA)

S.245(2)(c) applied where the taxpayer permitted his wife and, later, his children, to subscribe for non-voting common shares of his private company at a nominal price, with the result that he realized a capital gain under s. 69(1)(b)(ii) as a result of a deemed disposition of the appropriate fraction of his common shares in the company.

Sweeney v. The Queen, 90 DTC 6507 (FCTD)

In 1950, a written agreement between the taxpayer's father and the taxpayer provided that the son could purchase his father's shares in a company for a stipulated sum upon the father's death. The price per share was reviewable by the father, gave the son a right of first refusal in the event of a sale of the shares, and was revocable by either party upon 60 days' notice. Following the repudiation of this agreement by the executors of the father's estate following his death in 1983, the taxpayer was paid $625,000 in lieu of damages.

The taxpayer's counsel unsuccessfully submitted that what now is s. 246(1) governed the transaction because the failure of the father to revoke the agreement had the effect of conferring a benefit on the taxpayer.

Boardman v. The Queen, 85 DTC 5628, [1986] 1 CTC 103 (FCTD)

Since the taxpayer's legal obligations to his divorced wife were met by a court order which ordered the Registrar of Land Titles to transfer title to two houses held by the taxpayer's company to his wife, a benefit was conferred on the taxpayer by his company equal to the fair market value of the equities of redemption of the houses. "Transaction" in s. 245(2) has a broad meaning.

Mansfield v. The Queen, 83 DTC 5136, [1983] CTC 97 (FCTD), aff'd 84 DTC 6535, [1984] CTC 547 (FCA)

A company netted no cash from the sale of a $5,000 convertible debenture to its employee because it deposited with a bank an amount equal to the amount of a loan, made by the bank to the employee to finance his purchase of the debenture, in order to partially secure that loan. Nonetheless, there was no conferral of a benefit on the employee: the company "still owed the Plaintiff [employee] $5,000, payable according to its terms. It was no sham".

The Queen v. Immobiliare Canada Ltd., 77 DTC 5332, [1977] CTC 481 (FCTD)

By purchasing debentures of a sister Canadian resident corporation from its non-resident parent the taxpayer eliminated withholding taxes that ultimately would have been exigible on payments of the heretofore unpaid interest on the debentures, and thereby conferred a benefit equal to 15% of the total accrued interest at the time of sale. However, it was found that the accelerated receipt of an amount equal to the interest accrued at the time of the sale did not constitute a benefit: "the benefit must be of a more tangible and identifiable nature".

The Queen v. Esskay Farms Ltd., 76 DTC 6010, [1976] CTC 24 (FCTD)

The taxpayer, wished to sell land to the City of Calgary in consideration for two annual instalments in order to defer a portion of the gain to its second taxation year, but was informed that the City was precluded by statute from purchasing land over a period of years. As a result: the taxpayer sold the land to a trust company for the same purchase price, but payable in two instalments with the second instalment bearing interest at 7.5% per annum, and with a clause in the purchase agreement that the trust company could elect within 60 days of the date of the agreement of sale to void the agreement; and the trust company sold the land to the City for the same purchase price, paid in cash. Title was transferred directly from the taxpayer to the City.

In finding that the transactions did not entail a conferral of a benefit by the trust company on the taxpayer, Cattanach J. noted (at p. 6018) that the taxpayer acknowledged its obligation to pay income tax on the profit realized by it on the sale of the land when the deferred payments were received by it.

David v. The Queen, 75 DTC 5136, [1975] CTC 197 (FCTD)

As a result of transactions wherein the shares of a company held by the taxpayers were purchased on behalf of a pension plan which then caused the distribution of the company's assets, a benefit was conferred on the taxpayer because "they were able to withdraw the undistributed surplus of the company without paying taxation".

Indalex Ltd. v. The Queen, 88 DTC 6039, [1988] 1 CTC 60 (FCA)

It was found that the taxpayer, by purchasing aluminium from a Bermudan affiliate at a price that was 5% higher than what it would have paid if it had purchased the aluminium directly from the ultimate supplier, had conferred a benefit on the Bermudan affiliate, and withholding taxes were exigible on the amount of the benefit by virtue of s.s.245(2)(b) and 212(1).

Laxton v. The Queen, 88 DTC 6008, [1988] 1 CTC 19 (FCTD), rev'd , in part, 89 DTC 5327 (FCA)

In a joint venture agreement it was agreed that an individual member of the joint venture ("Laxton") would be paid an annual management fee equal to $450,000 minus the product of the Bank of Montreal prime rate and the amount of interest free loans made by the other members of the joint venture to Laxton. Imputed interest on interest-free loans made to Laxton by the joint venture (which previously had borrowed from the Bank) was included in his income as a benefit. Reed, J. stated: "Where an agreement explicitly provides that a taxpayer's remuneration for services is to take the form of an interest free loan, the taxpayer should be required to recognize that remuneration in some form in his taxable income."

MNR v. Enjay Chemical Co. Ltd., 71 DTC 5293, [1971] CTC 535 (FCTD)

In finding that a forgiveness of a portion of the trade indebtedness owing by the taxpayer to a U.S. affiliate would have given rise to a taxable benefit under s. 137(2) of the pre-1972 Act, Walsh J. stated (p. 5304):

"I believe that the words 'transactions of any kind whatsoever' are broad enough to cover the forgiveness of debt which took place in this case in that Esso International Inc. therefore conferred a benefit on respondent and this despite the fact that the rebate was made for a legitimate purpose and not with an intention to avoid or evade taxes."

See Also

Pelletier v. The Queen, 2004 DTC 3176 (TCC)

Although benefits were conferred on the taxpayers by virtue of their being able to acquire shares of a private company worth $300,000 for a purchase price of $10,000, this essentially was the result of the vendor's decision to accept the lower amount in order to settle a dispute. As the company did not directly or indirectly give shares to the taxpayers, there was no income to them under s. 246(1). It was not relevant that the company had consented to a waiver by the shareholders of the transfer restrictions in the shareholders' agreement.

Husky Oil Ltd. v. The Queen, 95 DTC 316 (TCC), aff'd 95 DTC 5244 (FCA)

The taxpayer, which needed to "shelter" a capital gain previously realized by it, purchased from a vendor with which it dealt at arm's length the shares of a holding company whose assets consisted of shares of operating companies whose adjusted cost base substantially exceeded their fair market value, and further agreed that following the winding-up of the holding company it would sell the shares of the operating companies back to the vendor for their respective fair market values.

Kempo TCJ. found that what then was s. 245(2) did not apply to these transactions (and to similar loss utilization transactions) because no "benefit" could arise to the taxpayer from its purchase of the shares of the holding company where it had provided fair market value consideration.

Brooks v. MNR, 91 DTC 639 (TCC)

The taxpayer was deemed under former s. 245(2) to have disposed of an "economic interest" in a corporation wholly-owned by him when he caused it to issue shares to his wife and children at a substantial undervalue.

Administrative Policy

2013 May ICAA Roundtable Q. 22, 2011-0411491E5

In…2011-0411491E5, CRA commented on an interest in a United States Limited Liability Corporation (LLC) held by an Alberta Unlimited Liability Corporation (AULC) owned by a Canadian resident individual. …[T]he individual would be subject to US taxation on…LLC income attributed to the AULC. CRA indicated that payment of these taxes on the individual's behalf would constitute a taxable benefit, either under S 15(1) if paid by AULC or under S 246(1) if paid by LLC. Can CRA explain the economic enrichment of the individual which it perceives to arise through the ownership structure? CRA responded:

[A]n amount paid by a corporation to its individual shareholder as a reimbursement of that shareholder's personal tax liability would result in an impoverishment of the corporation and an enrichment of the shareholder for purposes of subsection 15(1). A similar enrichment would result for purposes of subsection 246(1) where the shares are held by that individual indirectly through another corporation.

24 June 2015 T.I. 2015-0575911E5 F - Benefit to shareholder or conferred on a person

Corporation A, is wholly owned by Holdco, which has equal unrelated Shareholders 1, 2, 3 and 4. Corporation A disposes of a capital property to the spouse (who is not herself a shareholder) of Shareholder 4 at a price which is determined to be less than the property's fair market value. What are the consequences? After discussing the potential application of ss. 15(1.4)(c) and 56(2), CRA stated (TaxInterpretations translation):

…[Respecting s. 246(1)], it appears that if Holdco had made a payment directly to Shareholder 4, such payment would be required to be included in computing the income of Shareholder 4 pursuant to subsection 15(1). Accordingly, to the extent that subsection 246(1) was applicable, the value of the benefit that Holdco indirectly conferred on Shareholder 4 (through would be included in computing the income of the latter pursuant to paragraph 246(1)(a). Corporation A

See summaries under s. 15(1.4)(c) and s. 56(2).

3 March 2015 Memorandum 2014-0527841I7 F - Avantage imposable pour aéronef

In a wholly-owned stacked structure of three Corporations (C holding D, holding E), Corporation E acquired an aircraft for business use but with some percentage use by Mr. A, the sole shareholder of Corporation C, and by his father (Mr. B), who also was the director of Corporations D and E. Was CRA required (as submitted by the taxpayer) to apply IT-160R3 (which was archived for the years under review, and then cancelled in September 2012), under which the taxable benefit to Mr. A was computed on the basis of the cost of a first class ticket for an equivalent trip or should the benefit be based on the quantum of the denied expenses of Corporation E (based on application to those expenses of the personal-use percentage)?

The Directorate stated (TaxInterpretations translation, para. 23) that it "was in agreement with you that subsection 246(1) applied," (at para. 30) that "the benefit from personal use of the Aircraft was conferred on Mr. A in his capacity of shareholder and on Mr. B in his capacity of person related to the shareholder, Mr. B and that "subsection 15(1) does not apply in a situation where an advantage is conferred…on an indirect shareholder." Although it was "not clear…in considering the advantage to have been conferred by Corporation E, that it would be possible to support an income inclusion under subsection 246(1), …however… subsection 246(1) can apply…if it is established that Corporation C conferred the benefit respecting personal use of the Aircraft" (para. 32)." In particular (paras. 33, 34):

Notwithstanding that it could be established that Corporation E conferred a benefit on Mr. A, the value of a benefit would not be included in the calculation of the income of Mr. A…if it arose from a payment that Corporation E made directly to Mr. A, since Mr. A is not a shareholder of Corporation E. From tis perspective, subsection 246(1) does not apply respecting a benefit conferred by Corporation E on Mr. A… .

However, in … Masicotte the judge concluded that subsection 246(1) can apply when a corporation confers a benefit on an indirect shareholder.

In order to consider that:

Corporation C conferred directly or indirectly a benefit on Mr. A…it is necessary to demonstrate that Corporation C had an influence on Corporation E. (para. 35)

This condition was satisfied in light of the control of Corporations C and E by Mr. A.

[T]he value of the benefit conferred on Mr. B cannot be included in his income by virtue of subsection 246(1), because…if Corporation C had made a direct payment to Mr. B, this payment would not be included in the computation of the income of Mr. B by virtue of subsection 15(1) or paragraph 6(1)(a)… .

In accordance with paragraph 15(1.4)(c), the benefit conferred by Corporation C on Mr. B will instead be a benefit conferred on Mr. A wo is a shareholder of Corporation C, because Mr. B does not deal at arm's length with Mr. A. Hence, subsection 246(1) must be applied to such benefit on the basis that Corporation C conferred a benefit on Mr. A.

However, for a benefit conferred on Mr. B before November 1, 2011…it would not be possible to include [it] in the income of Mr. B or Mr. A… (paras. 36-38).

After discussing Youngman, Fingold, Schroter and Anthony (and before discussing Spence to the same effect), the Directorate stated (at para. 57):

[T]he value of the benefit to Messrs. A and B from personal use of the Aircraft corresponds to its FMV and not the cost to Corporation E.

These decisions were more authoritative and helpful than decisions dealing specifically with personal aircraft use (paras. 66-67). However (at para. 77):

[T]he denied operating expenses and CCA of Corporations E could be utilized in establishing the value of the benefit conferred on Mr. A and Mr. B to the extent that it could be demonstrated that this value approximated the FMV of the benefit received.

Respecting IT-160R3, the Directorate noted that as the personal usage percentage was under 33%, para. 5 thereof did not apply but that, in light of the level of operating expenses, referencing the price of first class tickets for comparable trips would result in too low an estimate of the taxable benefits – so that the guidelines in IT-160R3, paras. 3-5 should not be followed. Instead, the more general guideline in para. 1 "for determining the value of a benefit on the basis of what is reasonable" should be followed, so that "the value of the benefit from personal use of the Aircraft should be established on the basis of the FMV of the benefit received" (para. 91). "Such FMV corresponds to the price which the shareholder would have to pay, in comparable circumstances, to obtain the same benefit from a corporation of which he was not a shareholder" (para. 99).

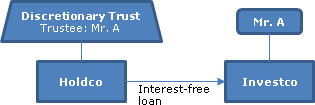

12 December 2012 Memorandum 2012-0464411I7 - Indirect Benefit

A taxable Canadian corporation (Holdco) which is wholly-owned by a trust of which Mr. A is the sole trustee and is a discretionary beneficiary, makes an interest-free loan to another taxable Canadian corporation (Investco) of which Mr. A is the sole shareholder. In finding that this did not give rise to a taxable benefit, CRA indicated that:

- "for the purposes of 15(1) we have generally not considered that a benefit is conferred on a shareholder by reason of the making of a loan to that shareholder…[except] where, for example, there is no reasonable expectation of repayment of the loan amount"

- furthermore, applying s. 15(1) also is problematic as the "loan has been made to Investco, which is not, itself, a shareholder of Holdco"

- "since the amount advanced by Holdco to Investco was a "loan", there is no "payment" that would be considered to have been made that would allow the provisions of s. 56(2) to apply to include the loan amount in the income of Mr. A"

- unlike Massicotte, the case "does not involve a holder of shares of a parent corporation obtaining a benefit from a subsidiary corporation"

- s. 246(1) "does not permit characterizing a loan to a corporation as, instead, one made to the individual who controls that corporation in order to then calculate a benefit under paragraph 80.4(2"

- As there have been no relevant changes since Cooper, s. 105(1) "would not be considered favourably as a ground for including a foregone interest benefit in the income of Mr. A"

16 April 2012 T.I. 2011-041149

A Canadian-resident individual owns all the shares of an Alberta unlimited liability company which, in turn, owns a majority of the membership units of a US LLC. As a result of both corporations being fiscally transparent entities under US tax law, the individual is required under US tax law to pay tax on his proportionate share of the income of the LLC.

The determination of the management of the LLC to pay the US tax liability of the individual would result in an income inclusion to the individual under s. 246(1) given that a payment of that amount by the Alberta ULC would have resulted in an income inclusion under s. 15(1).

10 January 2011 Memorandum 2009-034425

In a situation where a second-tier subsidiary provides a benefit to the shareholder of a first-tier corporation, s. 246(1) can be applied on its own to assess the taxpayer for that benefit. (If the first-tier corporation had provided the benefit directly, the benefit would have been taxable under s. 15(1).)

25 March 1994 T.I. 933550 (C.T.O. "Interest Reduced 15(1) Benefit")

"It our general position that the term 'shareholder' as used in subsection 15(1) of the Act would not include a person who indirectly controls a corporation through a holding corporation. Although the provisions of subsection 15(1) of the Act would not normally apply in respect of the value of any benefit conferred by a corporation on an indirect shareholder, the provisions of subsection 246(1) of the Act could apply to include the amount of the benefit in the hands of the indirect shareholder."

93 A.P.F.F. Round Table, Q.17

Where a taxpayer transfers assets to an unrelated corporation applying the s. 85(1) rollover, it is not possible to rule out the application of ss.246(1) and 56(2).

24 March 1993 T.I. (Tax Window, No. 38, p. 1, ¶2490)

Re potential application of s. 246(1) to a holder of common shares where his father exchanges preferred shares of the corporation for preferred shares having a lower redemption amount and for options.

90 C.R. - Q.47

Where a Canadian corporation borrows funds from an arm's length lender and the Canadian corporation's non-resident parent guarantees the loan for no consideration, the Canadian corporation will not be considered to have received a taxable benefit from the parent.

80 C.R. - Q.55

The listing in IT-453 of conferral-of-benefit situations was not intended to be comprehensive.

IT-239R2 "Deductibility of Capital Losses from Guaranteeing Loans for Inadequate Consideration and from Loaning Funds at less than a Reasonable Rate of Interest in Non-arm's Length Circumstances"

Former s. 245(2) may have been applied in situations where there is a material benefit to other shareholders as a result of a minority shareholder making a loan to, or honouring a guarantee in respect of, a Canadian corporation controlled by him and members of his family.

Subsection 246(2) - Arm’s length

Cases

Jobin v. The Queen, 78 DTC 6538, [1978] CTC 493 (FCTD)

What is now s. 245(3) did not apply to an arm's length sale of all the shares of a company, an operation which admittedly entailed the stripping of dividends, because the sole purpose of the vendor was to sell his business for a good price: "il a conclus la vente, non en conformite de quelque autre operation, ni pour effectuer la paiement de quelque obligation, mais pour se departir de son commerce a un prix convenable".

See Also

Extendicare Health Services Inc. v. MNR, 87 DTC 5404, [1987] 2CTC 179 (FCTD),

"[T]he term 'bona fide', when used as an adjective, is generally taken to mean 'honestly', 'genuinely' or 'in good faith'."