Cases

Nussey Estate v. The Queen, 2001 DTC 5240, 2001 FCA 99

The two sons of the taxpayer had transferred to him shares of a family corporation. The shareholders' agreement provided that, on the death of a shareholder, his shares were deemed to have been redeemed by the company on the day preceding that of death.

The Court affirmed the finding of the Tax Court Judge that the deemed redemption provisions in the agreement did not effect a retroactive disposition of the shares the day before the taxpayer's death.

Stone's Jewellery Ltd. v. Arora, [2000] GSTC 168 (Alta. Ct. Q.B.)

A transaction in which a company paid for a real estate property but the shareholders (who were not registered for GST purposes and, therefore, were not entitled to input tax credits) took title and, later, transferred the property to a newly incorporated company in reliance on the s. 85(1) rollover, was rectified so that both transfers were void ab initio. The second transaction was done under the mistaken belief that it could be done on a rollover basis whereas the Minister had assessed on the basis that the land was transferred as inventory. Respecting the first transfer, the Court found that the parties shared a mistaken belief based on their professional advice that no adverse tax consequences would result from the transfer.

Sussex Square Apartments Ltd. v. The Queen, [1999] 2 CTC 2143 (TCC), aff'd [2000] 4 CTC 203 (FCA)

After the taxpayer had, for some time, been disposing of apartments suites which it held under a headlease by way of assignment rather than a sublease, it realized that a sublease would give rise to a more favourable income tax result (by accessing the reserve under s. 20(1)(m)). Accordingly, it entered into modification agreements with the bulk of the assignees under which one day of the term covered by the lease was reserved to the taxpayer, thereby effectively converting the assignment into a sublease. When the provincial Land Titles Office declined to register the modification agreements, the taxpayer obtained an order of the Supreme Court of British Columbia declaring that the assignments were so modified. The taxpayer then registered the court-approved modifications and a further 49 modification agreements were registered after the court order without the necessity of an application to the court.

Bowman T.C.J. found that the Dale decision applied to make the court-approved modification agreements effective ab initio but concluded at p. 451 (with respect to the remaining 49 modification agreements) that "it would be pushing the Dale principle too far if I applied it to contractually agreed fiscal revisionism without the benefit of a court order".

Barnabe Estate v. The Queen, 99 DTC 5387 (FCA)

The Court, in reversing a finding of the trial judge, found that the deceased taxpayer had entered into an oral agreement with his corporation (which was the lessee of the assets of a farming business) to transfer to it the ownership of all those assets on the day that he met with his accountant, communicated that intention, and signed a blank election form. The failure to fix, at that time, the fair market value of the assets, and to prepare a schedule specifically listing them, represented a delay in dealing with purely "housekeeping measures"; and given that under Manitoba corporate law, a corporation had the capacity and the powers of a natural person, it was not germane that the purchasing corporation had not ratified the oral contract on that date (nor was it relevant that there was a significant delay before the consideration was paid).

The Queen v. Larsson, 97 DTC 5425, docket A- 623-96 (FCA)

An order of the British Columbia Supreme Court made in 1993 that mortgage payments made from November 1989 onward by the taxpayer on a house that had been sold prior to 1993 were deemed to be periodic maintenance payments pursuant to s. 60.1(2) of the Act was intended by the Court to have been made nunc pro tunc, with the result that the payments were deemed to be allowances under s. 60.1(2) for the years in question.

Dale v. The Queen, 97 DTC 5252, Docket: A-15-94 (FCA)

Before finding that an order of the Nova Scotia Supreme Court retroactively confirming that preference shares had been issued to the taxpayers also had retroactive effect for taxation purposes, Robertson J.A. stated (at p. 5256):

"If the legislature of a province authorizes its courts to deem something to have occurred on a date already past, then it is not for the Minister to undermine the legislation by refusing to recognize the clear effect of the deemed event."

Greenway v. The Queen, 96 DTC 6529, Docket: A-392-91 (FCA)

Various conditions contained in an agreement for the acquisition of a MURB development by co-investors including the contractor's undertaking to obtain zoning and planning permissions, arrange financing, obtain a MURB certificate and convey title, did not represent conditions precedent the non-fulfilment of which would result in nullity of the agreement. Accordingly, various soft costs incurred by the investors after the effective date of the agreement were currently deductible by them.

Kettle River Sawmills Ltd. v. The Queen, 92 DTC 6525 (FCTD)

Timber rights were not acquired on the intended adjustment date of March 26, 1974 but instead were acquired no earlier than the time that the purchaser commenced using the rights and had the other incidents of title.

R. v. Hutton, [1990] 2 CTC 258 (Alta. C.A.)

The taxpayer fraudulently caused his employer to pay invoices for work on renovation to his home in 1983 and 1984. After the renovations were completed in 1984, he informed the company vice-president and controller that he had done so, following which it was agreed that the misappropriated funds would be treated as a loan to him. Because this subsequent agreement was in place when he filed his 1984 tax return, there was no failure to report a benefit from employment with respect to the 1984 misappropriation, albeit, not the 1983 misappropriation.

Shaw v. The Queen, 89 DTC 5194 (FCTD), aff'd 93 DTC 5213 (FCA)

The efficacy of a pre-incorporation contract was recognized.

Bouchard v. The Queen, 83 DTC 5193, [1983] CTC 173 (FCTD)

Before holding that the Statute of Frauds did not preclude a finding that the taxpayer held land in trust for his son and daughter-in-law, Cattanach J. indicd (p. 5200-5201) that a parol trust operates from the time of its creation even if writings evidencing the existence of the trust do not come into existence until a subsequent date.

Scandia Plate Ltd. v. The Queen, 83 DTC 5009, [1982] CTC 431 (FCTD)

Control of a corporation was not acquired until the date for closing the agreement of purchase and sale, when the purchaser acquired ownership of the shares, rather than on the earlier effective date of the agreement when there allegedly was a verbal executory contract in place for the acquisition of the shares. Cattanach J. applied the principle that where a preliminary contract (whether verbal or otherwise) is intended (as was the case here) to be superseded by, and is in fact superseded by, a contract of a superior character (here, the written agreement), then the later contract prevails.

Perini Estate v. The Queen, 82 DTC 6080, [1982] CTC 74 (FCA)

It was held that "interest" calculated from the closing date of a share purchase on outstanding instalments of a purchase price was taxable as interest rather than being capital receipts notwithstanding that the amount of each instalment of purchase price depended on the amount of after-tax net profits of the borrower earned subsequent to the closing date, with the result that the amount of interest could not be calculated until those earnings were ascertained. Le Dain, J. stated:

"it is my opinion that it was open to the parties to the agreement of sale in this case to treat the occurrence of the contingency as having such effect, insofar as interest was concerned. Cf. Trollope & Colls, Ltd. et al. v.Atomic Power Constructions Ltd., [1962] 3 All E.R. 1035, in which it was held that parties to a contract could give their contract retrospective effect. There is no rule of law that prevented them from treating an additional sum payable on account of the purchase price ... as owing, for the purposes of interest, from the closing date ...."

Kingsdale Securities Co. Ltd. v. The Queen, 74 DTC 6674, [1975] CTC 10 (FCA)

Since the settlors lacked the requisite intention prior to the execution of settled trusts, the execution of the trust deeds did not have retrospective effect to the time of alleged settlement, notwithstanding a clause in the deed purporting to make the trust effective on a date prior to its execution.

Howard v. The Queen, 74 DTC 6607, [1974] CTC 857 (FCTD)

The BC Supreme Court on February 16, 1970 ordered the taxpayer to pay $200 per month to his wife commencing February 1, 1970. On October 22, 1973 the B.C. Supreme Court confirmed a recommendation of the Registrar, dated April 22, 1971, that the support be increased to $270 per month commencing April 1, 1970. Since the second judgment, on a true construction, was a judgment nunc pro tunc the taxpayer was entitled to make a deduction under what now is s. 60(c) at a rate of $270 per month commencing on April 1, 1970.

Nelson v. The Queen, 74 DTC 6266, [1974] CTC 360 (FCA)

Although it was the intention of the four related shareholders of a corporation that father hold 100 voting participating shares and each of his three sons hold 100 non-voting participating shares following the incorporation of a partnership in which the four individuals were equal partners, at the time of the payment by the corporation of a $1,000 dividend to each of the four shareholders the three sons (due, in part, to an oversight of the company's solicitor) held one voting participating share of the corporation. It was held (at p. 6268) that "each of the four shareholders was entitled to the $1,000.00 actually paid to him by the company either because the 96 shares issued to the appellant as part of the consideration for the partnership property were held by the appellant on a resulting trust for the members of the partnership in equal shares, or because the agreement between them called for them to have equal equity shareholdings in the company and to share equally in any divisions of the profits of the company". S.56(2) accordingly did not apply to include approximately 97% of the dividend in the income of father.

Guilder News Co. (1963) Ltd. v. MNR, 73 DTC 5048, [1973] CTC 1 (FCA)

The sale in 1964 of shares by a corporation to its sole shareholder at an undervalue gave rise to a benefit to the shareholder notwithstanding that the shares had been purchased at the same undervalue by the corporation from the shareholder two years earlier. "If it had not been for the 1964 resale, the individual would have continued in the relatively impoverished state that resulted from the 1962 sale. As a result of the 1964 resale he was restored to his relatively affluent state at the expense of the company and ... the company thereby conferred a benefit on him." Under the jurisprudence, it was irrelevant that "when an individual benefits a company whose stock is all owned by him or when such a company benefits the individual, the individual's overall net assets may well have neither increased nor diminished ... ."

A price adjustment clause did not negate (although it arguably reduced) the amount of the benefit, given that there was no bona fide attempt to estimate a fair market value sale price. "If, in fact, a company simply sold property to its sole shareholder on expressed terms that the price payable was an amount equal to fair market value and provided a fair manner to determine such value, I would agree ... that there could not, as a matter of law, be a benefit arising out of the sale."

Rose v. MNR, 73 DTC 5083, [1973] CTC 74 (FCA)

It was held that a management services contract between a corporation ("Central Park Estates Limited") and a partnership with an effective date of November 1, 1965 was not executed, and approved by the directors of Central Park Estates Limited, until at least May 31, 1966, with the result that one of the corporate partners could not be said to be carrying on an active business during the interim seven-month period. "It may well be that, after Central Park Estates Limited subsequently executed the back-dated services contract and after the corporate partners accepted payment as though they had performed the services under that contract, the situation was the same, as among the parties, as though everything had been regularly done on November 1, 1965 ... However, in my view, no such back-dating of transactions can affect the fact that, during the period from November 1, 1965 to June, 1966, there was no services contract ..."

MNR v. Lechter, 66 DTC 5300, [1966] CTC 434, [1966] S.C.R. 655

In the taxpayer's 1955 taxation year, he accepted the Department of Transport's formal offer of settlement for compensation in respect of its expropriation of his land inventory, and in his 1956 taxation year, the Treasury Board ratified the agreement and authorized the payment to the taxpayer. Abbott J. found that "in accordance with the ordinary rules of mandate, [the ratification of the Treasury Board] had retroactive effect to [the date of the agreement]", with the effect that the gain of the taxpayer was realized in his 1955 taxation year rather than 1956 taxation year.

Falconer v. MNR, 62 DTC 1247, [1962] CTC 426, [1962] S.C.R. 664

The members of a syndicate that had acquired an oil farm-out agreement incorporated a private company ("Ponder") on June 15, 1951, and Ponder immediately took possession of the syndicate's assets. However, an agreement evidencing the transfer and the consideration therefor (the obligation of Ponder to issue shares to the syndicate members) was not executed until September 25, 1951, by which date the assets had significantly increased in value. Before finding that "the agreements of September 25 did no more than to evidence, in writing, agreements which already existed" (p. 1250), with the result that the taxpayer should not be regarded as having realized a taxable profit by virtue of receiving shares on September 25, 1951 with a value higher than the assets transferred by him to Ponder on June 15, 1951, Martland J. applied (at p. 1250) the principle in Howard v. Patent Ivory Manufacturing Co. (1888), 38 Ch. D. 156 at 163:

"'Where possession has been given upon the faith of an agreement, it is I think the duty of the Court, as far as it is possible to do so, to ascertain the terms of the agreement and to give effect to it.'"

See Also

Fiducie Claude Deragon v. The Queen, 2015 CCI 294

Vendors agreed to sell shares for a sale price of $16 million, of which $2 million was payable in subsequent years only if an EBITDA condition respecting the sold companies was satisfied. The sales agreements contained a simple price adjustment clause based on the final audited shareholders’ equity of the sold companies. When a substantial deficiency in shareholders’ equity subsequently emerged, a negotiated Settlement Agreement concluded more than a year after the sale reduced the sale price by $0.5 million (to $15.5 million), increased the portion of the sale price payable under the reverse earn-out to $3 million – and provided that the vendors would reimburse a further portion of the sale price out of amounts received by them under the earn-out.

Favreau J respected the retroactive downward adjustment, pursuant to the Settlement Agreement, of the proceeds of disposition by $0.5 million but, by the same token, considered that the reverse earnout amounts of $3 million could not be excluded from the proceeds of disposition notwithstanding their contingent nature. However, he did not permit a downward adjustment to the proceeds of disposition for the contingent obligation to refund the sale price to the purchasers.

See summary under s. 54 – proceeds of disposition – para. (a).

Charania v. The Queen, 2015 TCC 80

An individual shareholder of a corporation ("B&N") thought that he was the beneficial owner of his home, but everyone else, including his accountants (and ultimately the Tax Court) considered that it was beneficially owned by B&N. Immediately before his sale of the home at a gain, it was transferred to him by B&N, with the excess of its book value over the outstanding mortgage amount being treated as a shareholder advance to him.

In reversing a shareholder benefit assessment of the taxpayer equal to the excess of the property's fair market value over its book value (and stating an "understanding" that the shareholder loan amount would be increased by this difference), VA Miller J stated (at paras. 40-41):

The Appellant was not aware of the error in this case nor did he sanction the error. He believed that the Declaration of Trust was followed and that he already owned the Property.

It is clear that B&N did not intend to confer a benefit on the Appellant. It transferred the Property to him and included an amount with respect to the Property as a loan receivable from him. The problem was that the amount included was incorrect. This problem arose as a result of an error made by [the accountants] not from any intent of B&N or the Appellant to commit a fraud.

Murphy Estate v. The Queen, 2015 TCC 8

An estate unsuccessfully argued that the effect of the settlement of some estate litigation pursuant to a consent order, which provided for the transfer of the interest in the deceased's RRSPs, by the children who otherwise would have received the RRSP assets, to the deceased's surviving spouse, was to retroactively access the rollover for RRSP transfers to a surviving spouse. In connection with noting that the children had not disclaimed their interests in the RRSPs, V. Miller J stated (at para. 33) that the effect of a disclaimer (being "a refusal to accept an interest which has been bequeathed to a disclaiming party") is "to void the gift as if the disclaiming party never received it."

See detailed summary under s. 146(8.8).

Al-Hossain v The Queen, 2014 TCC 379

To secure mortgage financing for his home purchase, the appellant's friend ("Khandaker") agreed to co-sign the mortgage documents and to be placed on title as a co-owner. Less than three weeks after closing, they signed a statutory declaration stating that the appellant was the 100% beneficial owner and that Khandaker held a 0.01% interest in trust for the appellant. In rejecting a submission that the appellant was the sole beneficial owner (so that the new housing HST rebate was available to him), Lyons J stated (at para. 27):

The creation of a trust must be properly documented containing the requisite elements of a trust, dated, signed and in existence prior to or contemporaneous with the matter that is the subject of the trust arrangement.

See summary under ETA s. 254(2).

James v. The Queen, 2013 DTC 1135 [at 705], 2013 TCC 164

The British Columbia Court of Appeal ordered a retroactive increase in the monthly amount of the support payments the taxpayer paid to his spouse, and was thus made to pay a lump sum equal to the monthly increases. Pursuant to the finding in Dale that retroactive court orders are binding on the Minister for tax purposes, C Miller J found that the lump sum represented payments "on a periodic basis," and were therefore support payments.

The present case was distinguishable from Peterson, in which there was insufficient proof that the lump sum in question represented periodic payments.

Twomey v. The Queen, 2012 DTC 1255 [at 3739], 2012 TCC 310

In 2005, the taxpayer sold 78 of his 100 common shares of an Ontario corporation ("115") to the other shareholder ("D.K."), and claimed the capital gains exemption. Both shareholders had believed from the time of the organization of 115 in 1995 that they each held 100 common shares of 115, and this belief was reflected in 115's financial statements and accounting ledgers. However, in connection with the sale in 2005, they discovered that (due to some communication difficulties relating to a change in the taxpayer's counsel) the corporate minute books recorded only one share as having been issued to each of them. A shareholders' resolution was passed "acknowledging the initial intent of the parties and issuing share certificates totaling 99 common shares of 115 to each of the Appellant and D.K. to correct the error without further consideration to be paid for them" (para. 9). CRA denied substantially all of the taxpayer's capital gains exemption claim on the basis that 77 of the 78 shares sold by him had been issued within 24 months of the time of their disposition, contrary to the requirement of para. (b) of the qualified small business corporation share definition.

Pizzitelli J. found that in fact all 200 common shares (including those sold by the taxpayer) had been issued in 1995. He stated (at paras. 19, 24):

We frankly have inconsistent corporate records at best, but the reality is that the correcting resolution quite clearly speaks to the other documents, clearly superseding them for the simple reason of correcting an error. ...

...The correcting resolution resulted in the records being amended to give effect to the true facts.

Accordingly, the taxpayer satisfied the 24-month requirement and was eligible for the capital gains exemption.

Sommerer v. The Queen, 2011 DTC 1162 [at 845], 2011 TCC 212, aff'd 2012 FCA 207

In 1996, the taxpayer (a Canadian-resident individual) purported to sell shares of a Canadian company ("Vienna"), while retaining the rights to dividends and the voting rights, to an Austrian private foundation (privatstiftung) which had been contemporaneously formed and funded in Austria by his father, and with family members including the taxpayer named as beneficiaries. The selling price was equal to 1/2 the fair market value of the shares (i.e., 1/2 of $1.33 per share, or $0.665 per share). When the parties subsequently were advised that it was not legally possible to transfer shares excluding certain of the rights attaching to those shares, they amended the agreement (perhaps in 1998, but purportedly on a retroactive basis) so as to provide that the Vienna shares (including all of the rights attached to the shares) had been sold in 1996 at a price of $1.33 per share, and with the voting rights and the dividend rights on the shares then immediately being assigned by the foundation to the taxpayer for $0.665 per share.

C. Miller J found that these amendments were legally effective on a retroactive basis in light inter alia of a clause in the original sale agreement which provided that any parts of the agreement that were found to be unenforceable would be replaced so as to give effect to the business intent. Respecting a submission that the sale agreement instead was void for mistake, he stated (at para. 54);

With respect to the Vienna shares, there was no mistake that Mr. Sommerer owned the Vienna shares, and that he could transfer them; he simply could not carve out certain rights. But the parties could easily rectify the situation, which they did.

Gestion Forêt-Dale Inc. v. The Queen, 2009 DTC 1378, 2009 TCC 255

After the accountants, over a year later, realized that a reorganization plan resulted in Part IV tax because two corporations were not connected at the time of the redemption of shares giving rise to a deemed dividend, they had resolutions prepared by a notary dated as of the date of the previous reorganization effective date purporting to issue special voting shares to the corporation receiving the deemed dividend, followed immediately thereafter by the shares' redemption. Favreau, J. interpreted these measures as retroactive tax planning, not the correction of a mistake in the implementation of the plan, and noted, in any event, that under the articles of the corporation issuing the voting shares, such shares were not redeemable, nor did it appear that such shares were validly issued as it appeared that the corporation did not receive the subscription price therefor.

Gagnon v. The Queen, 2008 DTC 3111, 2006 TCC 194

The taxpayer originally signed an agreement for the sale of his half interest in a business (which was found to be held in a corporation) to his brother. Upon receiving the fifth and final cash instalment payment of the purchase price from the corporation, his brother purported to have the corporation retroactively issue two shares to the taxpayer and got the taxpayer to sign a second agreement providing for the purchase of those two shares by the corporation from the taxpayer in consideration for the four payments that the corporation had in fact made to him. In finding that the taxpayer had received deemed dividends, Lamarre J. stated (at para. 22) that "a person can be declared a shareholder retroactively" and found that the second agreement was the one that prevailed as it reflected the contractual reality negotiated by the two brothers.

Lloyd v. The Queen, 2002 DTC 1493, Docket: 2000-1146-IT-G (TCC)

Although the taxpayer signed an agreement with a holding company for the sale of shares in a company ("READ") to the holding company, Bowman T.C.J. found that the transaction was not completed, so that there was no disposition for purposes of s. 84.1. Among other things, none of the stipulated consideration was ever paid by the holding company and the directors of READ did not approve the transfer as required by the articles.

Bowman A.C.J. stated (at p. 1496):

"If the Minister can attack a transaction in this court or the Federal Court of Appeal on the basis it is legally ineffective or incomplete, so too can the taxpayer. There is no need to wait for a provincial court to set an incomplete or legally invalid transaction aside."

Fallis v. The Queen, 2002 DTC 1242, Docket: 2000-383-IT-G (TCC)

Following an assessment of the taxpayer under s. 160 she alleged that there had been a transfer of a one-half interest in a property to her from her husband in the summer of 1991 when there was a discussion between them that she should receive the equity in the property rather than, as alleged by the Crown, three years later when, on a sale of the property, the husband signed a direction authorizing the purchaser to pay the closing proceeds to her. McArthur T.C.J. stated (at p. 1244):

"It takes more than an intention or uncertain conversation to transfer an interest in real estate. The law of contract requires a clear statement of transfer, acceptance and delivery."

McAnulty v. The Queen, 2001 DTC 942, Docket: 2000-420-IT-G (TCC)

The time at which the taxpayer's employer agreed to issue shares to her was the time at which the president called her to his desk and told her that he was going to issue to her 45,000 stock options at a $1.50, rather than at the later date when a written stock option agreement was signed by the president and a related directors' resolution was passed. The president had ostensible authority to commit the company to issue shares to her (notwithstanding that the Board of Directors in fact had not delegated this authority to him as required by the stock option plan), and failure to comply, on the earlier date, with a stipulation in the stock option plan that the options be granted to her pursuant to a written and approved stock option agreement related to failure to comply with administrative rules rather than invalidating the grant.

Glassford v. The Queen, 2000 DTC 2531, Docket: 97-2826-IT-G (TCC)

O'Connor T.C.J. applied s. 8(3) of the Land Act (BC), which provided that "a disposition of Crown land is not binding on the government until the certificate of purchase ... is executed by the government under this Act" to find that the period of ownership of land by the taxpayer did not satisfy the 24-month holding period requirement in the definition of qualified farm property.

Horkoff v. The Queen, 97 DTC 621 (TCC)

Dividends that were purportedly paid to the taxpayers "as of" December 30, 1990 were dividend income to the taxpayers in their 1991 taxation years given that the dividends were not declared until February 13, 1991, the amount of the dividends was not known until that date, and the dividends would not have been declared or paid if a sale of shares of the corporation had not closed on that date.

Leung v. MNR, 92 DTC 1090 (TCC)

In rejecting a submission of the Crown that the taxpayers were not assisted by a price adjustment clause, Kempo J. noted that they had addressed the fair market value of the shares in question, had noted the historical sales and earnings of the corporation, had considered the effect of a recent material event and had felt at the time that the value fixed by them (which later was established to be excessive) was reasonable.

Voukelatos v. MNR, 92 DTC 1076 (TCC)

Following the exercise by the taxpayer of a "shot-gun" clause in the shareholders' agreement, it was understood by him and the other shareholder that the corporation would redeem the other shareholder's shares. However, the documents which were drawn up and signed called for the purchase of the other shareholder's shares by the taxpayer. When this was discovered by the taxpayer two years later, an amended agreement effective as of the earlier date was executed by all three parties providing for the transfer of the other shareholder's shares to the corporation for the same price.

Rip J. rejected an argument by the agent for the taxpayer that the defence of non est factum applied given that there was negligence on the part of the taxpayer in not reading the original agreement. The agent apparently did not argue that the subsequent amending agreement was a rectification of the first written agreement.

Seaman v. MNR, 90 DTC 1909 (TCC)

The Court refused to give retroactive effect to the replacement, as of a previous date, of a demand promissory note by a series of promissory notes payable at specified dates.

May Estate v. MNR, 89 DTC 534 (TCC)

A court order became effective from the date it was pronounced rather than not taking effect until the date of issuance.

Pellizzari v. MNR, 87 DTC 56 (TCC)

After finding that the taxpayer's employer had conferred a benefit on her in 1979 and 1980, Couture C.J. found that at the time of the decision (1986) it was not legally feasible to allow a retroactive deduction of those fees against loans that were outstanding in the books of the corporation. He stated (at. p. 59) "its fiscal years have been closed, and they reflected at the time its financial position as it legally existed then".

Robert Bédard Auto Ltée. v. MNR, 85 DTC 643 (TCC)

Before going on to find that the taxpayer had disposed of property on the effective date for a lease-purchase agreement in which land and building was leased by the taxpayer to the lessee for five years with an obligation to purchase within that period of time for a specified price, Tremblay T.C.J. found that the date of sale of the land and building was the subsequent date when the lease was terminated by purchase and stated (at p. 648):

"Consequently, where the parties have agreed for a future time, it cannot be decided under civil law that the transaction took place at a time other than the one determined and executed by them. A bi-lateral promise does not have the effect of making the promisor-purchaser an owner; it merely allows him to become one when the contract of sale is executed or when the judgment in lieu of contract is rendered."

Spence v IRC (1941), 24 TC 311 (Ct of Sess (1st Div'n))

The taxpayer sold shares to a third party in 1933 under a contract which he subsequently alleged to have been induced by fraud. In 1939 he obtained a judgment reducing (i.e., setting aside)the contract with effect from the date that it was made, together with orders that the shares be retransferred to him and the dividends which the purchaser had received be paid to him. After the judgment, the Revenue repaid the surtax assessed on the dividends in the hands of the fraudulent purchaser and assessed the taxpayer instead. In finding that the taxpayer was taxable on the dividends when they had been paid by the company, Lord President Normand stated (at p. 317):

In this case the party sued for rescission and in the end of the day he obtained a decree of reduction. The effect of that reduction was to restore things to their position at the date of the transaction reduced, with the result that as at that date and afterwards the successful pursuer in the action fell to be treated as having been the person in titulo of the shares which he had sold to the defender and therefore to have been in right of the dividends. No doubt it is true that in the interval the dividends had to be paid and were paid to the defender because his name stood in the register as the proprietor of the shares and no doubt also they were for the time being treated by the Inland Revenue as his income and while matters stood entire no other person had any right to the shares or to the dividends except the defender, Mr Crawford. But from the moment the reduction took place Mr Spence fell to be treated as having been throughout the proprietor of the shares and equally the person properly entitled to receive the dividends.

Waddington v. O'Callaghan (1931), 16 TC 187 (KBD)

A father instructed his solicitors that it was his intention to take in his son as a partner effective on the date of the instruction and requested them to prepare a deed of partnership. In finding that no partnership was intended to arise before the deed had been executed, Rowlatt J. stated (p. 197):

"When people enter into a deed of partnership and say that they are to be partners as from some date which is prior to the date of the deed, that does not have the effect that they were partners from the beginning of the deed [sic]. It cannot alter the past in that way. What it means is that they begin to be partners at the date of the deed, but then they are to take the accounts back to the date that they mentioned as from which the deed provides that they shall be partners."

Administrative Policy

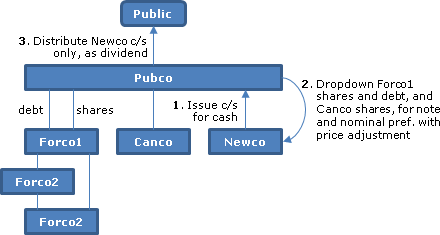

2013 Ruling 2013-0488291R3 - Reorganization of Corporations - Rollover

Pubco (a Canadian public company) wishes to spin-off non-strategic assets to its shareholders without incurring the expense of a plan of arrangement or holding a shareholders' meeting. In the preliminary transactions to pre-package Newco for distribution, Pubco will subscribe nominal cash for common shares, and the drop down the non-strategic assets for interest-bearing notes and for preferred shares whose redemption amount is nominal but would increase on application of a price adjustment clause. The amount of the taxable dividend to the shareholders is minimized by their being distributed only the Newco common shares.

The Directorate did not rule on the price adjustment clause "since such adjustment will be due to circumstances that do not constitute proposed transactions that are seriously contemplated."

Ruling letter described in greater detail under s. 52(2).

29 October 2013 T.I. 2013-0507881E5 - Price adjustment clause

A price adjustent clause in the share provisions for preferred shares issued by Opco to the taxpayer in Year 1 in consideration for the transfer of property to Opco provide that the redemption value of the shares issued will be changed if the FMV of the consideration for the shares is determined by CRA to be different than the determination at the time of the transaction (or an additional amount will be paid if the change is upward and the preferred shares issued are redeemed before the determination by CRA).

In year 5, Opco redeems all the preferred shares, in year 7, CRA determines that the FMV of the property and the redemption value of the preferred shares should have been higher, and "pursuant to the price adjustment clause" the taxpayer receives an additional payment from Opco in year 8.

When would the taxpayer have to include the additional payment as income? CRA stated:

[I]f the price adjustment… is valid…CRA's longstanding position is that the additional payment will be treated as a dividend that will be included in the taxpayer's income in the year of receipt under subsection 84(3) of the Act. …

However, as the additional payment is not determined at the time of the redemption of the shares… it should not be included in the income of the taxpayer in the year of the redemption as part of the amount paid under subsection 84(3)… .Rather, the CRA…[will] tax the additional payment pursuant to the general rules with respect to the dividends, that is, to tax such amount at the time it is received. …

[T]here would be no interest with respect to the income tax computed on that additional amount if the income tax is paid in a timely manner pursuant to the Act and if any instalment computed under the Act with respect to the income tax for the year of the receipt was remitted on time.

25 September 2013 T.I. 2013-0488571E5 F - Repayment of a dividend

A taxpayer refunded part of the dividends received from a corporation in 2006.

After citing Sussex Square Apartments v. The Queen., [1999] 2 CTC 2143 (TCC), [2000] 4 CTC 203 (FCA), Dale v. The Queen, 97 DTC 5252 (CFA) and Waddington v. O'Callaghan (1931) 16 T.C. 187, CRA stated (TaxInterpretations translation):

…CRA does not accept retroactive changes to a contract or a corporate act…at least where no court order is rendered to that effect. When a dividend is declared by the board of directors…it cannot be reduced or nullified by the board and the shareholders have no power to request its nullification.

10 June 2013 STEP Roundtable Q. 7, 2013-0480291C6

The requirement in IT-169 that CRA be notified of the existence of a price adjustment clause was not carried over into S4-F3-C1, and no longer represents CRA policy.

27 March 2013 Folio S4-F3-C1

A price adjustment clause will be recognized where there was a bona fide intention to transfer at fair market value as determined by a fair and reasonable method, with the price adjustment amount (based on the fair market value as determined by CRA or a court) actually paid (or a legal liability therefor adjusted) (para. 1.5). Where the purchase price is adjusted by issuing or cancelling shares (as opposed to adjusting the shares' redemption amount or adjusting a note), this may result in "a number of legal and technical difficulties" (para. 1.6)

Where shares with a price adjustment clause are redeemed before the adjusting payment is made, the adjusting payment will be included under s. 84(3) in the income of the redeemed shareholders when received (para. 1.10). A price adjustment clause in a butterfly reorganization "might" not prevent s. 55(2) from applying (para. 1.12).

5 October 2012 APFF Roundtable Q. , 2012-0453891C6 F

The summary (which is more specific than the actual question) describes an estate freeze in which a taxpayer exchanges his common shares of of a corporation for preferred shares of the same corporation, with the purchase price and the value of the preferred shares being subject to a price adjustment clause. (New) common shares of the corporation then are issued to a discretionary family trust.

CRA was asked whether the price adjustment clause will prevail if CRA seeks to apply s. 75(2), and whether this depends on whether the preferred shares are still held by the taxpayer at the time of such assessment. CRA stated (TaxInterpretations translation):

In the context of an estate freeze, if the price adjustment clause is valid and the taxpayer makes the necessary adjustments to the price for the common shares and to the redemption value of the freeze preferred shares received as consideration, and to the amount that is due for the preferred shares on their redemption (so that the corporation receives a reimbursement or makes a payment for the difference, as the case may be), the CRA considers that the tax consequences of the estate freeze take such clause into account. ... It thus is not necessary that the price adjustment clause specify that it applies as well for purposes of subsection 75(2)....

If the CRA recognizes a price adjustment clause as being valid in a given situation in accordance with the wording of the clause, it can engage a retroactive adjustment to the redemption amount of the freeze preferred shares. In the situation you described, the freeze preferred shares have not been redeemed. Consequently, where the estate freeze occurred in a particular year, the price adjustment clause causes an adjustment to the redemption amount of the freeze preferred shares which has an effect respecting subsequent years in which these shares are redeemed.

2010-0366301I7 dealt with the situation where the taxpayers had not implemented the terms of the price adjustment clause, and it was too late to do so.

24 May 2012 T.I. 2011-0429991E5

Mr. A engages in an estate freeze transaction in Year 1 in which all his common shares are exchanged in a s. 86 reorganization for preferred shares whose terms contain a price adjustment clause. Following his death in Year 16 years later, CRA determines that the redemption value of these preferred shares at the time of their issuance was less than the fair market value of the common shares.

If the price adjustment clause was "valid," i.e., it complied with IT-169 including that the valuation method used in Year 1 was "fair and reasonable," then the redemption amount of the preferred shares would be automatically increased retroactively to Year 1, thereby increasing the fair market value proceeds of the deemed disposition of those shares in Year 16 on the death of Mr. A. If the price adjustment clause was not valid, it "could be argued" that there was a misrepresentation that opened up Year 1 to reassessment under s. 86(2).

2011 APFF Roundtable Q. 4, 2011-0412071C6 F

where the directors declare a capital dividend and before the payment date for the dividend the corporation (which has individual shareholders) realizes a capital loss that causes the capital dividend account to be less than the amount of the capital dividend, the fact of there being an excessive capital dividend will not be solved by the corporation passing a further resolution, before the payment date, to split the dividend in two (given that the original dividend declaration continues to be valid).

21 November 2011 T.I. 2011-042219 F

if preferred shares with a redemption amount which is subject to a price adjustment clause are redeemed before there is an upward adjustment to the redemption amount pursuant to that clause, a payment of the resulting additional amount will be included in the shareholder's income in the year of receipt under s 84(3).

2011 APFF Roundtable Q. 23, 2011-0412111C6 F

notwithstanding that para. 26 of IC 76-19R3 has not been modified to this effect, the validity of a price adjustment clause does not depend on the provision of an amended election (on form T2057) under s. 85(7.1).

28 May 2012 2010 STEP Roundtable Q. 2, 2010-0363071C6

For an amount to be "payable" to a beneficiary in a trust's taxation year, the beneficiary must have an enforceable right to payment by the end of that year. It is possible for the beneficiary to obtain a right to payment of an unknown amount if the amount is unknown because of administrative delays, but not if it depends on a subsequent contingency or event.

The beneficiary must also be advised before the end of the trust's taxation year of the trustees' decision to pay and the basis on which payment is to be apportioned. Where the amount is known, ordinarily a demand promissory note will be given to the beneficiary (or the beneficiary's legal guardian) as acknowledgement of the existence of the debt. The note should be delivered in the trust's taxation year or as soon as possible (i.e. in the event of the aforementioned administrative delays).

8 October 2009 T.I. 2009-033886

A request to vary the income tax consequences of transactions that have already taken place will only be considered if such a variance would amount to a rectification of an error and only if there is unequivocal evidence substantiating the fact that an error was made.

14 January 2005 T.I. 2004-010941 -

A revival of a corporation under the CBCA would appear to have retroactive effect and the revived corporation will generally have all the rights (including tax attributes) and obligations that it would have had if it had not been dissolved.

18 April 2001 Memorandum 2001-006946 -

An amended distribution agreement would not be accepted as retroactively causing a film to no longer be an excluded production given that, prior to the entering into the amended agreement, a distributor had already acquired beneficial ownership of a portion of the production under the original agreement. "Generally, we do not accept retroactive amendments, for tax purposes. This position is consistent with the jurisprudence ... ."

10 March 1999 T.I. 5-982912

Although a price adjustment clause may be used for satisfying the requirements of s. 80(2)(g), "an acceptable price adjustment clause should not involve the cancelling of issued shares or the issuing of additional shares".

1996 Corporate Management Tax Conference Round Table, Q.9 (CTO "Plans of Arrangement")

Ordinarily, RC will respect the ordering of a series of transactions where the order is specified in a plan of arrangement.

1996 Calgary Round Table, Q. 17 (961680) (CTO Effective and Closing Date")

Discussion of when the date of disposition/date of acquisition for a transaction may be prior to the closing date.

94 CPTJ - Q.19

RC will accept situations where revenue between the effective date of a transaction and the closing date is reported differently for financial statement purposes than for taxation purposes, provided that the tax treatment accords with the position stated at 91 CPTJ, Q. 25.

92 CR - Q.30

RC generally will require that any elections under s. 85 that are affected by a price adjustment clause be amended.

17 August 1992, T.I. 921353 (April 1993 Access Letter, p. 135, ¶C20-1141)

Forgiveness of accrued interest has legal effect from the date of the amendment to the debt obligation or such later date as is provided in the amendment. It is not possible to retroactively waive the right to receive interest.

91 CR - Q.28

Any income earned prior to the adoption of a pre-incorporation contract by a corporation becomes its income for its first fiscal period and, where the income is from an active business, is eligible for the small business deduction.

91 C.R. - Q.41

The date of disposition of property (and, therefore, the date upon which income commences to be earned by the purchaser) is the date the beneficial ownership is intended to pass to the purchaser and the time the vendor has an absolute but not necessarily immediate right to be paid.

91 CPTJ - Q.25

There have been instances where RC has administratively accepted that income earned between the effective date of sale of an oil and gas property and the closing date was for the account of the purchaser rather than the vendor where both parties to the transaction agreed that the effective date should be utilized and no significant tax benefit arises from the use of this date.

16 September 1991 TI (Tax Window, No. 9, p. 9, ¶1451)

RC cautioned that in Dorcas v. MNR, 91 DTC 350 the Tax Court indicated that past events cannot be altered ab initio by steps taken ex post facto.

25 February 1991 TI (Tax Window, Prelim. No. 3, p. 29, ¶1123)

When a court judicially declares a person to have died on the day the person was last seen alive or the day on which it is likely that the person died, the date of the judgment should be regarded for tax purposes as the date of death.

10 December 1990 TI (Tax Window, Prelim. No. 2, p. 20, ¶1065)

An annulment of a bankruptcy does not invalidate the application of s. 128 for the period commencing on the date the taxpayer became bankrupt and ending on the date of the annulment.

90 CR - Q.58

If the parties fail to notify RC of a price adjustment clause in their tax returns, this failure by itself will not preclude the acceptance of their clause provided the other conditions contained in IT-169 are met.

27 March 1990 TI (August 1990 Access Letter, ¶1364)

RC will not respect a price adjustment clause which contemplates that a final judgment of a court of competent jurisdiction would be binding as to the fair market value of the property in question.

14 September 89 T.I. (February 1990 Access Letter, ¶1108)

In response to a submission that expenses incurred between the time of an agreement, and the time that the agreement is reduced to writing, are eligible under s. 66(15)(d.1), RC stated its view that agreements generally are not binding until they are written.

ATR-22R (14 April 89): RC indicates that its rulings do not pertain to a price adjustment clause described in the ATR.

ATR-36 (4 Nov. 88): With respect to a price adjustment clause in the share provisions for preference shares issued on an estate freeze, RC states that it is unable to provide a ruling as to the possible application of s. 15(1) if the price adjustment clause becomes effective:

"since the operation thereof is not a proposed transaction. In our opinion, however, if all the conditions mentioned in paragraph 1 of Interpretation Bulletin IT-169 are met, the provisions of subsection 15(1) of the Act would not be applied to tax a benefit to the shareholders in these circumstances."

87 CR - Q.70

Where the completion of an asset sale is subject to a true condition precedent (e.g., regulatory approval), then the vendor and purchaser cannot agree that income earned between an effective date and the date of completion will be income of the purchaser.

85 CR - Q.52

Efficacy of price adjustment clauses is recognized.

80 CR - Q.14

RC is prepared to issue favourable rulings respecting price adjustment clauses used in an estate freeze, provided that the clause involves adjusting the redemption amount of the frozen shares or the making of a cash payment.

IT-396R "Interest Income"

"Where an enforceable agreement for the sale of property is executed but the negotiated price is not paid until a subsequent date, any interest that is receivable by the vendor for the period from the date of the agreement to the date of payment is interest income in the vendor's hands." On the other hand, if no enforceable agreement existed prior to the payment date, the amount paid instead simply represents "an upward adjustment to the sale price of the property".

IT-169 "Price Adjustment Clauses"

This bulletin has been cancelled and removed from the CRA website. It previously stated:

1

. ...If the parties have agreed that, if the Department's value is different from theirs, they will use the Department's value in their transaction, that is their choice and the Department will recognize that agreement in computing the income of all parties, provided that all of the following conditions are met:

(b) Each of the parties to the agreement notifies the Department by a letter attached to his return for the year in which the property was transferred

(i) that he is prepared to have the price in the agreement reviewed by the Department pursuant to the price adjustment clause,

(ii) that he will take the necessary steps to settle any resulting excess or shortfall in the price, and

(iii) that a copy of the agreement will be filed with the Department if and when demanded.

S4-F3-C1 does not contain an analogous provision.

IT-216 (Cancelled) "Corporation Holding Property as Agent for Shareholder" 20 May 1975

- A corporation may hold in trust, as agent for a shareholder, property that was acquired specifically to be held in this way. This situation, however, will only be accepted as a fact where there is an agreement or declaration of trust, entered into before or at the time the property was acquired, between the corporation and the shareholder, which clearly sets out the intention of the parties to the agreement and the degree of participation of the shareholder in the property so held in trust.

Articles

Douglas S. Ewens, Paul Lynch, "Comments on Rectification", 2005 Conference Report, c. 23

Includes comments on CRA's position.

Darcy De Moche, Greg Johnson, "Recent Developments and Transactions Affecting Income Funds and Royalty Trusts", 2005 Conference Report, p. 17:6

Discussion of effect of releasing documents from escrow.

Michel Bourque, "Requirement of Notice to the Canada Customs and Revenue Agency", Tax Litigation, Vol. IX, No. 4, 2001, p. 590.

Jules Lewy, "Making Amends", CA Magazine, January/February 2002, p. 41

Discussion of Juliar by the taxpayer's counsel.

Wilfred M. Estey, "Pre-Incorporation Contracts: The Fog is Finally Lifting", Canadian Business Law Journal, Vol 33, No. 1, February 2000, p. 3.

Wertschek, "The Tax Advisor and Commercial Law: Some Issues", 1993 Conference Report, C. 24, pp. 24:31-39

Discussion of escrow arrangements, and of transactions that cannot be conditional.

Commentary

The tax consequences of transactions often turn upon when they occurred. Documents to legally implement a transaction often are not executed (or been drafted) on the date on which they are desired to take effect. Furthermore, even if a document is executed on or before the date in the document on which it is stipulated to be effective, there may be a subsequent amendment to the document - and the parties may wish the transaction to be considered to occur for tax purposes on the original effective date on the basis described in the amended document.

Except for transactions where the Statute of Frauds has been pleaded and found to be applicable ([pin type="node_head" href="772-Bouchard"]Bouchard[/pin]), or where a specific statute requires implementation through a specific document (e.g., amending share capital through filing articles of amendment, or amalgamating through filing articles of amalgamation), many transactions can be implemented orally, i.e., without written documentation (although for obvious reasons, this often will be undesirable). It follows that when a transaction is evidenced in writing, the agreement or other document may record an earlier effective date on which the transaction was actually implemented. For example, taxpayers have successfully established that they transferred assets to a corporation on a date prior to the execution of any documents evidencing that transfer ([pin type="node_head" href="772-Barnabe"]Barnabe[/pin], [pin type="node_head" href="772-Falconer"]Falconer[/pin], Cf. [pin type="node_head" href="772-Rose"]Rose[/pin]). Similarly, property has been found to be held on and after a date on trust or a resulting trust notwithstanding the lack of a contemporaneous trust deed or other document ([pin type="node_head" href="772-Nelson"]Nelson[/pin], [pin type="node_head" href="772-Bouchard"]Bouchard[/pin]). An agreement has been found to be effective at a rate prior to the date on which it was evidenced in writing even where the written agreement did not refer to the prior date ([pin type="node_head" href="772-McAnulty"]McAnulty[/pin]).

It is common for parties to enter into an agreement for a transaction that will only be implemented on a subsequent date when various conditions have been satisfied ([pin type="node_head" href="415-ImperialGeneral"]Imperial General[/pin]). In such a case the transaction typically occurs on the subsequent date, and not on the date of the agreement. Accordingly, the existence of an oral agreement on a particular date does not necessarily establish that the transaction described by that agreement occurred on that date ([pin type="node_head" href="772-Scandia"]Scandia Plate[/pin], [pin type="node_head" href="772-Barnabe"]Barnabe[/pin], [pin type="node_head" href="772-KettleRiver"]Kettle River[/pin] Cf. [pin type="node_head" href="772-Perini"]Perini Estate[/pin]). Similarly, a trust deed cannot have retrospective effect if at the earlier time the settlor lacked the requisite intention ([pin type="node_head" href="772-Kingsdale"]Kingsdale Securities[/pin]), and it would appear that a purported share redemption will not be effective on a stipulated date that is prior to the date on which a condition precedent to the share redemption occurrs ([pin type="node_head" href="772-Nussey"]Nussey[/pin]).

Where parties agree that income will be distributed or allocated on the basis of an earlier effective date, and it is found that their transaction did not occur for income tax purposes on that earlier date, then as a matter of commercial law that agreement nonetheless should be respected. For example, if an asset purchase agreement specifies an effective date of January 1 but it is found that the asset purchase did not actually occur until March 1, the characterization of the transaction under the Act should respect the fact that the income earned between January 1 and March 1 is the property of the purchaser rather than of the vendor. However, the March 1 effective date might mean that the transfer of that property from the vendor to the purchaser on closing is characterized as an adjustment to proceeds of disposition, rather than as a transfer of income that has been earned by the purchaser. See [pin type="node_head" href="772-Waddington"]Waddington v. O'Callaghan[/pin] and 91 CR - Q.41.

There are exceptions to the rule that persons should not be considered to have effected a particular transaction in a specific way on a date if at that time they lacked the requisite intention to do so. First, a retroactive (nunc pro tunc) order of a provincial Supreme Court will be respected as having retroactive effect for purposes of the Act ([pin type="node_head" href="772-Dale"]Dale[/pin], [pin type="node_head" href="772-Larsson"]Larsson[/pin], [pin type="node_head" href="772-Howard"]Howard[/pin], [pin type="node_head" href="772-Sussex"]Sussex[/pin]). Second, the corporate doctrine of pre-incorporation contracts potentially means that an agreement that was made before a corporation came into existence may be treated as giving rise to a transaction of the corporation (see [pin type="node_head" href="772-Shaw"]Shaw[/pin]). Third, where a contract provides that where any provision thereof is found to be invalid, the contract shall be rectified so as to give effect to the business intent of the parties, a subsequent rectification of the contract pursuant to this clause by the parities themselves very well may be respected as having retroactive effect for tax purposes ([pin type="node_head" href="772-Sommerer"]Sommerer[/pin]).

Agreements for non-arm's length transfers of property by taxpayers to a corporation for share consideration typically contain a price adjustment clause under which the redemption amount of preferred shares received by the taxpayers, or the quantity of common shares issued to them, will be adjusted if the initially stipulated redemption amount or number of common shares issued to them proves to be different than the fair market value (net of assumed liabilities or debt issued to them) of the property they transferred to the corporation. Price adjustment clauses also may be utilized in other types of transactions. The efficacy of price adjustment clauses rests, in part, on the notion that the operation of a price adjustment clause is not a subsequent attempt to change the terms of a transaction that has already occurred but, rather, gives effect to the intention of the parties at the previous time of implementation to transact on fair market value terms. See [pin type="node_head" href="772-Guilder"]Guilder News[/pin], [pin type="node_head" href="772-Leung"]Leung[/pin] and the various statements of the Agency set out below (including IT-169 and 90 CR - Q. 58).