Subsection 110.6(1) - Definitions

Annual Gains Limit

Administrative Policy

86 C.R. - Q.49

The exemption will be available in respect of capital gains allocated by a partnership.

Cumulative Net Investment Loss

Administrative Policy

1990 Answers of Calgary District Office (May 1990 Access Letter, ¶1200, Q. 11)

Where an employee has received an interest-free loan to acquire shares of his employer, his cumulative net investment loss will be increased by the amount of the deduction under section 80.5. However, taxable dividends will decrease his cumulative net investment loss.

Eligible Real Property Gain

Administrative Policy

21 June 1993 T.I. (Tax Window, No. 32, p. 8, ¶2600)

Re whether property last acquired by an individual after February 1992 from the individual's spouse will give rise to an eligible real property gain.

Interest in a Family Farm Partnership

Administrative Policy

21 January 1991 T.I. (Tax Window, Prelim. No. 3, p. 23, ¶1098)

A residence located on a farm which is occupied by members of the family partnership who operate the farm is property used in a farming business if the individual in question takes an active part in the farming business on a regular basis.

Investment Expense

Administrative Policy

3 July 1991 T.I. (Tax Window, No. 5, p. 21, ¶1336)

The taxable benefit from an interest-free loan which is deemed to be interest under s. 80.5 and to be deductible under s. 20(1)(c) is properly included in "interest expense".

13 March 1991 T.I. (Tax Window, No. 1, p. 17, ¶1142)

Where a partner uses borrowed money to acquire an interest in a partnership that has income from an active business and from property, the interest will be "investment expense" to the extent that it relates to the partner's share of the partnership's property income.

28 May 1990 T.I. (October 1990 Access Letter, ¶1446)

A loss from a rental operation carried on without a reasonable expectation of profit is not an investment expense.

89 C.P.T.J. - Q8

A taxpayer with working interest CEE and also flow-through share CEE should set up notional CCEE pools to assist in the CNIL calculation. The allocation of deductions by the taxpayer between working interest CEE and flow-through share CEE must be made on a reasonable basis.

Where a taxpayer invest in a limited partnership, has CEE and CDEL allocated to him at the partnership's year-end (December 31) and claims a deduction in respect of those amounts in the following calendar year, the addition to the taxpayer's CNIL will take place in that year where the taxpayer claims a deduction.

Investment Income

Administrative Policy

13 January 1993 T.I. 923208 (November 1993 Access Letter, p. 505; Tax Window, No. 28, p. 15, ¶2382)

A guarantee fee ordinarily will be considered to be business income rather than investment income.

Non-Qualifying Real Property

Administrative Policy

22 July 1994 T.I. 5-940136

None of the exclusions in s.(a)(iii)(C) to (G) is available where the real property is used in a business carried on by another partnership.

Where the real property is owned in co-ownership by individuals and is used in the active business of a partnership owned by their respective spouses, the exception in s.(a)(ii)(G) will not be available because, in RC's view "the expression 'a spouse of the individual' [in s.(a)(ii)(E)] cannot be interpreted as a reference to more than one individual".

12 January 1993 T.I. 923151 (November 1993 Access Letter, p. 503, ¶C109-154)

The use of the word "principally" requires that the property as a whole be considered rather than a percentage or a portion of the property. Provided that the principal or primary use test (as described in IT-195R4) is met, the entire property will not be a non-qualifying real property.

8 January 1993 T.I. 922776 (November 1993 Access Letter, p. 503, ¶C109-155; Tax Window, No. 28, p. 5, ¶2367)

Real property owned equally by two unrelated individuals that is leased by them to a corporation owned equally by them to be used by it in carrying on its active business will not qualify because, in the case of each individual, the shares owned by him will not represent all or substantially all the fair market value of all the issued and outstanding shares of the corporation. Similar conclusions would apply in the case of two individuals in a 50/50 general partnership.

Articles

Hirsch, "Capital Gains Exemption in Real Property", 1992 Conference Report, c.11.

Qualified Farm or Fishing Property

See Also

Otteson v. The Queen, 2014 DTC 1173 [at 3637], 2014 TCC 250,

The taxpayers, spouses, bought a farm in 2003 to start a tree farming business. Following the discovery of gravel deposits, and before the business generated revenue, the taxpayers sold the land in 2008 and claimed the capital gains exemption under s. 110.6(2). The taxpayers rented approximately 50% of the acreage, on which they had not planted trees, to a hay farmer.

Hogan J concluded that the portion of the property that was never rented to a third party was "qualified farm property."

First, he found that although the property was owned by the taxpayers directly, it was used by a partnership the interests in which were a farm partnership, so as to satisfy (a)(v) of the definition (see summary under s. 96(1)).

Second, the land "was used in the course of carrying on the business of farming in Canada," which Hogan J found did not entail a requirement that the land be used in a farming business at the time of disposition (para. 49), so that it was irrelevant that the taxpayers had sold their equipment by then. In particular, as the business was carried on through a partnership, the "50% income" requirement in clause (i)(A) (now (ii)(I)) of s. 110.6(1.3)(a), and the 24-month regular and continuous business requirement in s. (b)(ii) (now (a)(ii)(B)) was satisfied, as the evidence showed that the taxpayers were both actively involved in the tree-farming business.

Third, the taxpayers' partnership interests were "interests in a family farm partnership," as defined in s. 110.6(1). The "50%" threshold in para. (a) of that definition must be satisfied throughout the 24-month period, while no such requirement applies to the "all or substantially all" threshold in para (b) (para. 56). Based on Hogan J's finding that taxpayers were involved in the tree-farming business, the partnership interests were interests in a family farm partnership. The taxpayers' renting part of the land to a third party was irrelevant, given the finding below that the rented land was not used in the partnership business.

The rented portion of the lands was not qualified farm property. Hogan J found (at para. 61) that there was nothing in the definition that would imply that land be treated indivisibly for the purpose of determining what constituted qualified farm property ("otherwise land that has been legally subdivided would be preferred to land that has not been.") He excluded a percentage of the land based on the greatest number of acres rented in any of the years coinciding with the tree-farming business (para. 63).

Administrative Policy

11 June 2015 T.I. 2014-0522641E5 F - Usufruct

A father, who has carried on a farming business for a number of years, grants the bare ownership of the property for consideration to his son while retaining rights as the usufructuary. He continues to exploit the farm land and the, subsequently transfers his rights as usfructuary to his son for a stipulated sum. Is the father's usufruct a qualified farm property as per s. 110.6(1)?

After noting that under s. 248(3)(a) "the property which is transferred to the son is an interest in a deemed trust," and indicating that "as the bare owner did not transfer, assign or dispose of any property to the deemed trust,…paragraph 108(7)(b) cannot apply to deem the beneficial interest of the bare owner to have been acquired for nil consideration," so that the deemed trust was not a personal trust, CRA stated:

A right of a usfructuary, which is an interest in a trust…is not a QFP. …

At the termination of the usufruct and, thus, of the deemed trust, there is a disposition of property held by the deemed trust in favour of the bare owner. However, such property cannot be a QFP for the trust because the definition of QFP indicates that a property is a qualified farm property of a taxpayer, except for a trust which is not a personal trust.

28 January 2014 T.I. 2014-0517601E5 - Qualified farm Property

Father acquired land which he actively farmed for a number of years, and then rented the land to his son. On father's death the taxpayer and the taxpayer's sisters inherited the land and continued to rent the land to their brother, after which they sold it to him. In indicating that the gain on such sale likely qualified, CRA noted that the 24-month ownership test appeared to be satisfied, and then stated:

[I]f in at least 2 years during the period the land was owned by your father, his gross revenue from the farming business he carried on in Canada exceeded his income from all other sources for that period, and such land was used principally by him in that farming business in which he was actively engaged on a regular and continuous basis, the land would be QFP.

16 March 1998 T.I. 5-963813

With respect to a 300-acre property, 50 acres of which were used for agricultural purposes and the balance, because of the steep terrain, lack of water and difficult access were not, RC indicated that it would not seek to deny that an asset had been used principally in the course of carrying on the business of farming where a portion of the total area was not suitable for any use.

27 December 1995 T.I. 953277 [grazing leases]

Grazing leases (which qualify as real property, i.e., leasehold interests) may qualify as qualified farm property.

1994 Institute of Chartered Accountants of Alberta Roundtable Q. 20, 7-940973

Taxable capital gains (including taxable capital gains arising from the transfer of qualified farm property to a corporation in order to utilize the capital gains exemption) would be income from a source other than farming for purposes of s.(a)(vi)(A).

The two-years' test in s.(a)(vi)(A) need not be satisfied in two consecutive years.

5 April 1994 T.I. 5-933648

In response to an inquiry as to whether a personally owned property of a deceased spouse which was used in a farming operation but is not used by the surviving spouse in farming but is rented to arm's length tenants would meet the definition of a "qualified farm property", RC indicated that the individual taxpayer need not use the property in the course of carrying on the business of farming at the time of its disposition.

12 May 1994 T.I. 940692

For purposes of the gross revenue test in paragraph (vi)(A) of the definition of "qualified farm property", gross revenue from farming would not include taxable capital gains or gross proceeds from the sale of farm property.

23 June 1993 T.I. (Tax Window, No. 32, p. 14, ¶2609)

Real property rented by an individual to a corporation would be considered to be used by the corporation for the purposes of the definition of qualified farm property.

11 February 1993 T.I. (Tax Window, No. 29, p. 18, ¶2423)

The two-year gross revenue test in the definition may be applied to any one of the persons described in ss. (a)(i) to (iii) without that person necessarily having to own the property at the time the test was met.

7 December 1992 T.I. (Tax Window, No. 27, p. 18, ¶2325)

Property that is held by a spousal trust and used by a nephew of the deceased in the business of farming will not qualify because a spousal trust cannot designate capital gains under s. 104(21.2) to the nephew.

92 C.R. - Q.52

The fact that a farm property has been subject to the "restrictive farm loss" provisions of section 31 does not preclude it from qualifying as a qualified farm property.

30 July 1992 T.I. 921204 (January - February 1993 Access Letter, p. 26, ¶C109-125)

Comprehensive discussion of the meaning of the phrase "qualified farm property".

9 October 1990 T.I. (Tax Window, Prelim. No. 1, p. 17, ¶1035)

GAAR will not apply to a transfer of farmland by an individual to his child pursuant to s. 73(3) following shortly thereafter by a sale by the child to an arm's length third party at a gain.

7 October 1991 T.I. (Tax Window, No. 10, p. 13, ¶1508)

A farming business and a relatively large-scale brokerage business for vegetables not grown by the corporation are separate businesses.

Discussion of when residence would be considered to be used in the farming business.

19 June 1990 T.I. (November 1990 Access Letter, ¶1526)

Where a full-time farmer commenced another occupation but retained the farmland and continued to live in the farmhouse, the land would still meet the definition of qualified farm property.

28 May 1990 T.I. (October 1990 Access Letter, ¶1472)

General discussion.

8 September 89 T.I. (February 1990 Access Letter, ¶1116)

Farm land used in an operation subject to the loss limitation in s. 31 will be regarded as used in a farming business.

Qualified Small Business Corporation Share

Cases

Hudon v. The Queen, 2001 DTC 5630, 2001 FCA 320

In the years in question a corporation ("Hall River") which owned forest concessions and rights to develop the hydro electric potential of a river was engaged in negotiations with Hydro-Quebec and other activities with a view to developing that potential. The Court reversed the finding of the Tax Court that Hall River was not carrying on business. Desjardins J.A. stated (at p. 5639) that "to require the existence of an agreement on the sale of electricity before Hall River may be considered to be 'carrying on business' is to add an element not found in the legislation" and noted that the exemption for the disposition of qualified small business corporation shares found in s. 110.6(2.1) of the Act was intended to unleash the entrepreneurial dynamism of individual Canadians.

See Also

Pellerin v. The Queen, 2015 CCI 130

The taxpayer (Mika), who was born on March 8, 2007, received a distribution of shares qua beneficiary of a Quebec family trust (and personal trust) on October 1, 2008 (and again on November 27, 2008) and (in each case) immediately sold the shares (i.e., at times that he was less than 24 months' old but had been in existence more than 24 months from conception). The resulting taxable capital gains qualified for the deduction under s. 110.6(2.1) if the shares satisfied the test in para. (b) of the "qualified small business corporation share" definition that throughout the 24 months preceding their disposition they were not owned by anyone other than Mika or a person related to him. In finding that this test was satisfied, Boyle J stated (at para. 12, TaxInterpretations translation):

In accordance with the Quebec law applicable to Mika and the trust, …from the moment that Mika was born alive and viable, he was retroactively considered as a beneficiary, indeed as a person, from his conception, insofar as the laws of general application respecting the public interest were concerned, and as the interests of Mika required.

This finding was not contradicted by a stipulation in the trust deed, which provided that children were beneficiaries only from birth, given that under the above general law, Mika only (retroactively to conception) became a beneficiary at birth.

Although this meant that for the portion of the 24-month period that Mika was a fetus, he was not a beneficiary of the trust (and, therefore, was not related to the trust under s. 110.6(14)(c)(i)) as his birth had not yet retroactively triggered his status as a beneficiary, this did not matter. Boyle J stated (at paras. 18, 20 and 22):

[T]he expression "throughout the 24 months" applies to the requirements of ownership, and does not require that the related person status existed throughout the period.

…[The] object [of s. 110.6(1)(b)] can be achieved by considering, as third parties, persons who are not related to the person who disposed of the share at the moment of its disposition.

…I would respond in the same manner if the facts concerned a parent and child born during the holding period of 24 months, two person who became spouses during the period of 24 months or a person adopted as a child during the period of 24 months (except that, in the latter case, question 1 [respecting timing of beneficiary status] would not arise.

Twomey v. The Queen, 2012 DTC 1255 [at 3739], 2012 TCC 310

In 2005, the taxpayer sold 78 of his 100 common shares of an Ontario corporation ("115") to the other shareholder ("D.K."), and claimed the capital gains exemption. Both shareholders had believed from the time of the organization of 115 in 1995 that they each held 100 common shares of 115, and this belief was reflected in 115's financial statements and accounting ledgers. However, in connection with the sale in 2005, they discovered that (due to some communication difficulties relating to a change in the taxpayer's counsel) the corporate minute books recorded only one share as having been issued to each of them. A shareholders' resolution was passed "acknowledging the initial intent of the parties and issuing share certificates totaling 99 common shares of 115 to each of the Appellant and D.K. to correct the error without further consideration to be paid for them" (para. 9). CRA denied substantially all of the taxpayer's capital gains exemption claim on the basis that 77 of the 78 shares sold by him had been issued within 24 months of the time of their disposition, contrary to the requirement of para. (b) of the qualified small business corporation share definition.

Pizzitelli J. found that in fact all 200 common shares (including those sold by the taxpayer) had been issued in 1995. He stated (at paras. 19, 24):

We frankly have inconsistent corporate records at best, but the reality is that the correcting resolution quite clearly speaks to the other documents, clearly superseding them for the simple reason of correcting an error. ...

...The correcting resolution resulted in the records being amended to give effect to the true facts.

Accordingly, the taxpayer satisfied the 24-month requirement and was eligible for the capital gains exemption.

Administrative Policy

17 July 2013 T.I. 2012-0473261E5 F - Actif d'impôts futurs / Future income tax assets

Is a future income tax asset an asset that is used principally in an active business carried on in Canada for purposes of the "qualified small business corporation share" ("QSBCS") and "small business corporation" ("SBC") definitions?

After indicating that there was "no significant difference" between the terms "future income tax assets" and "deferred tax assets" used in Chapter 3465 of Part II of the CICA Handbook, and in IAS 12, respectively, CRA stated (TaxInterpretations translation):

[A] future income tax asset is not an asset for purposes of the definition of QSBCS and of SBC. … However, when a future income tax asset becomes a tax receivable, such tax receivable must be considered as an asset for determining if a share is a QSBCS or a corporation is a SBC. The tax receivable can constitute an asset used in carrying on an active business…if it arises from the active carrying on of the business. For example…a tax receivable arising from a loss-carryback derived from an active business constitutes an asset used principally in [that] business… .

11 October 2013 APFF Roundtable Q. , 2013-0495631C6 F

Mr. X holds all the common shares of Holdco, whose only asset is shares of Opco with a fmv of $1M. Opco's has $1.5M of cash, $3.5M of active business assets and debt of $4M, so that it satisfies the 90% test, and the percentage tests were satisfied during the last 24 months. Immediately prior to a sale of Holdco, the cash of Opco is dividended to Holdco, and by Holdco to Mr. X, so that for a moment in time, Holdco does not satisfy the 50% test. Is such a momentary breach acceptable?

CRA stated (TaxInterpretations translation):

[A] share of SBC cannot fail to satisfy one of the above-described three tests, even if for only a moment, in order to qualify as a QSBC.

7 October 2013 T.I. 2013-0500941E5 F - Actif utilisé dans une entreprise active

A corporation carrying on an active business has a 9.9% interest in a limited partnership (an SENC), whose sole property is a rental builiding which, as to 17% of the space, is rented to the corporation. The other partners of the LP are the father of one of the two shareholders of the corporation (as to 79.6%) and his three sons (as to 10.5% in total). Is the 9.9% interest an asset used in an active business for purposes of the definition of "qualified small business corporation share"?

Before responding negatively, CRA stated (TaxInterpretations translation):

…17% of the building is used in an active business carried on by XXX. In our view, it is clear that the building is not, for SENC and its partners, an asset used in the course of an active business.

10 May 2013 T.I. 2012-0449651E5 F - SENC - revenu d'entreprise exploitée activement

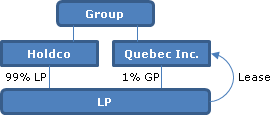

Holdco holds (as its only assets) a 99% limited partner interest in a limited partnership (LP), and the general partner (Quebec Inc.) holds a 1% interest. LP leases real estate to Quebec Inc., which operates an active business. Holdco and Quebec Inc. are controlled by the same group of persons and, accordingly, are associated and related.

CRA stated (TaxInterpretations translation):

In a situation not involving a limited partnership, subparagraph 110.6(1)(c)(i) contemplates that an asset, that is the property of a corporation but is leased to a related corporation, can be an asset used principally in an active business.

When a corporation holds an interest in a limited partnership (SENC), it is necessary to refer to the use of the assets of the SENC to determine if all or substantially all of the assets of the corporation are used principally in an active business within the terms of the definition of "small business corporation" in subsection 248(1).…

Generally, when the assets are used principally in an active business carried on in Canada by a partnership, [CRA] will consider that such assets are used principally by a partner in a Canadian active business….

2003 APFF Roundtable Q. 7, 2003-0030045

In order that the vendors of a corporation may receive repayment of amounts owing to them, one day before the sale of their shares the purchaser advances cash to the target corporation in order that it can refund amounts owing by it to the vendors. The advances received by the corporation from the purchaser generally would not be considered to be assets used principally in active business carried on primarily by the corporation, with the result that if such cash exceeded 50% of the total value of the target corporation's assets, its shares would cease to qualify.

7 March 2002 T.I. 2001-009178

in finding that cash accumulated to pay annual bonuses to the shareholder-managers was used in the corporation's active business and generated interest income that was income from an active business, CRA stated:

Generally, where a corporation has short-term cash reserves or near cash short-term investments as a result of accumulating cash in order to pay bonuses pursuant to the corporation's established policy, and the corporation actually uses the cash reserves and/or converts the short-term investments to cash in order to pay the bonuses, we would consider the cash reserves and/or the short-term investments to be active business assets.

CRA also stated:

...

2. Cash or near cash property is considered to be used principally in the business if its withdrawal would destabilize the business.

3. Cash which is temporarily surplus to the needs of the business and is invested in short-term income producing investments could be considered to be used in the business.

4. Cash balances which accumulate and are then depleted in accordance with the annual seasonal fluctuations of an ongoing business will generally be considered to be used in the business but a permanent balance in excess of the company's reasonable working capital needs will generally not be considered to be so used.

5. The accumulation of funds in anticipation of the replacement or purchase of capital assets or the repayment of a long-term debt will not generally in itself qualify the funds as being used in the business.

6. Cash or near cash property is considered to be used principally in the business if its retention fulfills a requirement which had to be met in order to do business, such as certificates of deposit required to be maintained by a supplier.

7. The CCRA recognizes that prudent financial management requires businesses to maintain current assets (including inventories and accounts receivables, as well as cash and near cash properties) in excess of current liabilities and will consider this requirement in assessing whether cash or near cash assets are used principally in a business. In the CCRA's view, cash and near cash assets held to offset the non-current portion of long term liabilities will not generally be considered to be used in the business.

4 July 1997 Technical Interpretation 5-9636

A residual interest (as defined in s. 98.1) is an asset used principally in an active business carried on primarily in Canada by the partner if the particular assets to which the residual interest relates are used principally in such a business by the partnership and the right to those assets is the only right of the partner.

An income right described in s. 96(1.1) is not an asset used in an active business carried on primarily in Canada by the partner.

9 September 1996 T.I. 5-961998

Where the only significant asset of a corporation was a large development property in the planning stages of development, RC questions whether the corporation has commenced to carry on a land development business.

13 October 1994 T.I. 5-941675 -

"Where ... a corporation has significant short term cash reserves as a result of receiving insurance proceeds and the corporation immediately uses the proceeds to replace a business asset, we would generally consider the insurance proceeds to be an active business asset."

General discussion of when cash or near cash property is considered to be a business asset.

21 October 1994 T.I. 5-942219 -

"A seasonal temporary closure of operations of a business done on a recurring basis, does imply that an active business has, notwithstanding such seasonal closure, been carried on throughout the business taxation year ... . [Normally] a full-service motel operation will be providing a sufficient level of services such that it would not be considered to constitute a business the principal business of which is to derive income from property."

12 April 1994 T.I. (C.T.O. "Active Assets")

Whether an investment in shares qualifies as an asset used principally in an active business turns on whether such asset is used principally in the corporation's business and is at risk with respect to that business. If its withdrawal would not have a decidedly destabilizing effect on the company, the asset would not be considered an asset used principally in an active business.

12 April 1994 T.I. 5-940236 -

List of seven factual guidelines that may be applied to determine whether cash held by a corporation is used in its active business.

28 June 1994 T.I. 5-933061 -

Where the fair market value of the assets of a corporation ("Parentco 1") comprise active business assets (40%), shares of one subsidiary (12%), shares of a second subsidiary (1%) and investments (47%), the shares of Parentco 1 will qualify as QSBCs since more than 50% of the fair market value of its assets are attributable to assets used in an active business carried on in Canada (40%) and shares of a subsidiary more than 90% of the fair market value of whose assets are attributable to such assets (12%). Similarly, where the fair market value of the assets of a corporation ("Parentco 2") comprise shares of a subsidiary 96% of whose assets are active business assets (53%), shares of a second subsidiary all of whose assets are investments (1%) and investments (47%), the shares of Parentco 2 will qualify as shares of QSBCs.

5 May 1994 T.I. 933027

Where two unrelated corporations each have a 1/2 undivided interest in a building and each use 1/2 of the building as their business premises, neither corporation will be considered to use that asset principally in its business because each co-owner has a right to occupy the whole property and cannot point to a particular part which represents its area.

14 February 1994 T.I. 5-933040 -

The position in IT-268R3, that a residence owned by a corporation will be regarded as used in the business of farming if more than 50% of its use is as accommodation for persons who are actively employed in the farming business or their dependents, assumes that the nature of farming operations is such that it may demand an employee's attention at virtually any time.

9 August 1994 T.I. 9333125

The respective corporations of a husband and wife together hold 100% and 40%, respectively, of Opco 1 and Opco 2 "through" a general partnership in which the husband's and wife's corporation have respective partnership interests of 60% and 40%. In addressing whether Opcos 1 and 2 are related to the corporations of husband and wife for purposes of the the definition of qualified small business corporation share in s. 110.6(1), the Directorate stated:

Indirect control of a particular corporation includes ownership of the controlling shares of an intermediary corporation that, in turn, owns the controlling shares of the particular corporation. This would also be our view where the intermediary shareholder is a partnership. In other words, where a partnership owns more than 50% of the issued voting shares of a corporation and where a particular partner is entitled without restriction, to exercise more than 50% of the votes that may be cast at a meeting of the partnership, it is our view that the particular partner controls the corporation.

1994 A.P.F.F. Round Table, Q. 35

Favourable analysis of a purification transaction in which a subsidiary whose shares represent 30% of the fair market value of the assets of a holding company and that has 40% of its assets invested in funds not used in its business, pays a dividend of those funds to the holding company which, in turn, pays the same amount as the dividend to its individual shareholder.

93 C.R. - Q. 58

RC considers that a corporate limited partner uses its proportionate share of each asset of the limited partnership for purposes of the definition of a qualified small business corporation share.

9 February 1993 T.I. (Tax Window, No. 29, p. 3 ¶2436)

Unless a corporation's business includes the lending of money, a loan receivable from the son of a controlling shareholder will not qualify as an asset used principally in the active business.

13 January 1993 T.I. 923260 (November 1993 Access Letter, p. 504, ¶C109-156)

Where a corporation owned by an individual ("Holdco") sold its shares of Opco to Newco, a newly-incorporated corporation owned by the same individual, and the individual then sold his Holdco shares, the Newco shares of the individual would not be considered to be shares substituted for the Holdco shares. Generally, there must be a disposition of the former property and an acquisition of the new property in exchange therefor in order for there to be substituted property.

2 December 1992 T.I. (Tax Window, No. 27, p. 22. ¶2320)

Refundable deposits paid under the Pits and Quarries Control Act are assets used in the active business of a pit operator.

7 December 1992 T.I. (Tax Window, No. 27, p. 18, ¶2326)

Where a private corporation goes public and a shareholder receives shares of the public corporation under the rollover in s. 86, the status of shares of the private corporation as a qualified small business corporation will not flow-through to the shares of the public corporation.

92 C.R. - Q.54

Prepaid expenses relating to an active business of the corporation could be considered as an asset used principally in an active business provided that their amount is reasonable, having regard to all the circumstances, and they were incurred in the normal course of the business.

It will be a question of fact whether land purchased for future development is used principally in an active business, as discussed further at 90 C.R. - Q.18.

92 C.R. - Q.24

Transactions whereby a stock dividend is issued to the sole shareholder of a corporation who transfers the stock dividend shares to Newco, followed by a redemption of the shares by Newco in order to "purify" the corporation for super-exemption purposes, should generally not be subject to the general anti-avoidance rule.

28 July 1992 T.I. (Tax Window, No. 21, p. 7, ¶2054)

Where an individual controls a corporation (Holdco) which in turn controls another corporation (Opco), indebtedness of Holdco owing to Opco will constitute indebtedness of a corporation connected with Opco by virtue of the control test in s. 186(2).

29 July 1992 T.I. 5-921123 -

Discussion of the application of the requirement for ownership for 24 months by none other than the individual or a person or partnership related to the individual where the shares are bequeathed directly to a surviving spouse, are transmitted to her via a testamentary trust, or are transferred to a spousal trust.

25 August 1992 T.I. 5-920191

Re whether cash and term deposits qualify as assets used primarily in an active business.

23 June 1992 T.I. (April 1993 Access Letter, p. 146, ¶C109-128)

Paragraph (d) of the definition can have no application where there are only two corporations and one of the corporations (Holdco) has, as its only assets, shares and debt of a second corporation (Opco) which satisfies the 50% test at all times.

1992 A.P.F.F. Annual Conference, Q. 9 (January - February 1993 Access Letter, p. 53)

Where Opco pays a dividend in kind with the appropriate amount to two Holdcos, each owing 50% of its shares, who then, by mutual agreement, purchase a portion of the shares of Opco held by the other Holdco for a purchase price equal to the dividend received by them, RC is prepared to regard the shares of Opco as qualifying immediately after that time.

10 January 1992 Memorandum (Tax Window, No. 17, p. 13, ¶1773)

A building only 40% of which is used in an active business is not an asset used principally in an active business.

25 March 1992 T.I. (Tax Window, No. 18, p. 14, ¶1828)

Amounts put in trust by clients of a funeral home corporation are not assets of the corporation for purposes of determining whether it is a small business corporation or its shares are qualified small business corporation shares.

19 March 1992 T.I. (Tax Window, No. 18, p. 5, ¶1823)

Where an individual acquires shares from her husband before their divorce (at which time their shares have been held by him for more than 24 months), the shares will meet the 24-month requirement even if she sells them before owning them personally for 24 months. However, the test will not be met if she acquires the shares from him after the divorce.

11 February 1992 T.I. (Tax Window, No. 16, p. 18, ¶1743)

The rental of a fishing licence would not necessarily preclude that asset from being considered to be used in an active business.

91 C.R. - Q.13

Re meaning of "primarily".

91 C.R. - Q.14

Where the sole asset of a Canadian-controlled private corporation is a 50% interest in a partnership 60% of whose assets are used in an active business carried on primarily in Canada, the shares of the corporation will not qualify because substantially all (generally, more than 90%) of the assets of the partnership are not used in an active business.

24 January 1992 T.I. (Tax Window, No. 12, p. 11, ¶1575)

Four numerical examples illustrating the application of the "all or substantially all" test in paragraph (d).

7 and 29 October 1991 T.I. (Tax Window, No. 10, p. 1, ¶1504)

In order for a loan owing to a corporation to be a qualifying asset for purposes of s.(c)(ii) it must be issued by a subsidiary rather than a parent corporation.

16 September 1991 TI (Tax Window, No. 9, p. 9, ¶1451)

The extended meaning of "control" in s. 186(2) may also apply in determining whether corporations are connected for purposes of the definition of qualified small business corporation share.

4 June 1991 Memorandum (Tax Window, No. 4, p. 22, ¶1276)

A shelf company will be treated as newly-incorporated at the time it is transferred by the lawyer to the taxpayer, provided that prior to the transfer 2the shares and assets involved were nominal (i.e., not more than three shares, not more than $1 in asset per share).

15 May 1991 T.I. (Tax Window, No. 6, p. 2, ¶1357)

Where the shares of Parentco are owned by related persons, its subsidiary will be deemed for purposes of Part IV and the definition of a qualified small business corporation share to control it.

24 April 1991 T.I. (Tax Window, No. 2, p. 12, ¶1211)

A corporation which meets the other tests will be a qualified small business corporation if 51% of its directly held assets are active business assets; whereas if less than 50% of its directly-held assets are active business assets, active business assets held indirectly through a wholly-owned subsidiary will not qualify it unless 90% of the value of the shares of the subsidiary are attributable to qualifying assets.

12 April 1991 T.I. (Tax Window, No. 2, p. 5, ¶1187)

Mortgages held by a developer which were the consideration for sales of its land inventory would not qualify as being used in an active business because the funds tied up in the mortgages are not used in the active business.

24 January 1991 T.I. (Tax Window, Prelim. No. 3, p. 7, ¶1106)

Discussion of the loss of the exemption as a result of the transfer of shares to a holding company controlled by unrelated individuals.

23 October 1990 T.I. (Tax Window, Prelim. No. 1, p. 21, ¶1026)

The business of a corporation may be considered to have commenced when essential preliminaries to the carrying on of that business in an active way are undertaken.

1 October 1990 T.I. (Tax Window, Prelim. No. 1, p. 15, ¶1034)

Where the sole asset of a corporation was land leased by it to its sole individual shareholder for use in his active business, such use will not qualify as use of assets by the corporation or a related corporation for purposes of the 24-month test.

90 C.R. - Q18

Where land is acquired and a building is constructed for use in an active business which will be expanding or relocating to the new facility, and the new facility is in fact used in the active business within a reasonable period of time after completion, the land and building will be considered to have been used in an active business from the date of acquisition of the land to the date of occupancy.

19 March 1990 T.I. (August 1990 Access Letter, ¶1378)

Where a franchisee corporation has a substantial investment in special shares and notes of the franchisor, such shares and notes would be considered as being used in an active business where they fulfill a contractual business obligation which is necessary for obtaining and maintaining the franchise.

8 March 1990 T.I. (August 1990 Access Letter, ¶1379)

Property is used in an active business if it is used principally with respect to that business and put to risk in the venture. However, engaging in an adventure in the nature of trade is not ipso facto carrying on a business.

8 March 1990 T.I. (August 1990 Access Letter, ¶1379)

A corporation doing business in the real estate development field and which holds some parcels of inventory which have not yet been developed will be considered to be using them in an active business provided that the parcels had been acquired, and or held for the purpose of being sold, or developed and sold in the course of the business.

2 March 1990 T.I. (August 1990 Access Letter, ¶1376)

If within 24 months of the determination time, the corporation in question had transferred 60% of its active business assets to a wholly-owned subsidiary, the shares of that subsidiary would not constitute qualifying asset described in subparagraph (c)(ii) by virtue of s. 110.6(14)(f).

27 February 1990 T.I. (July 1990 Access Letter, ¶1326)

A stock split which does not increase the appropriate stated capital account is not considered to result in new shares being issued for purposes of the definition.

26 February 1990 T.I. (July 1990 Access Letter, ¶1327)

Shares of a public corporation which supplies products to the CCPC in question ("Opco") will qualify as assets used in the active business of Opco where the shares are "vitally associated" to the operations of Opco, e.g., Opco obtains important benefits (volume discounts, terms of payment, etc.) if it holds a number of shares of the public corporation.

20 February 1990 T.I. (July 1990 Access Letter, ¶1325)

Where Holdco has an intercompany receivable owing to it from its wholly-owned subsidiary, Opco, and such intercompany receivable represents more than 10% of the assets of Holdco at a time during the 24-month period when the intercompany receivable is not evidenced in writing, then the shares of Holdco will not be qualified by virtue of paragraph (d) if Opco does not meet the all-or-substantially-all test throughout the 24-month period.

19 February 1990 T.I. (July 1990 Access Letter, ¶1325)

Where XYZ holds all the shares of A, more than 50% of the assets of A consists of advances to XYZ, the balance of such assets being used in an active business, and XYZ has used the advanced funds to make advances to other connected corporations which are CCPCs, it cannot be found that XYZ meets the "all-or-substantially-all" test due to the uncertainties of the endless loop which results in applying the test.

18 January 1990 T.I. (June 1990 Access Letter, ¶1273)

A corporation which holds real estate inventory which had been acquired to be resold, although no sale had occurred over the past five years, is not "using" those assets in an active business, in light of the comments made in Tara by Jackett J. that an adventure does not involve the carrying on of a business. In addition, the holding of an asset with a view to prospective future business use does not constitute use in that business.

13 December 1989 T.I. (May 1990 Access Letter, ¶1227)

The expanded concept of control set out in s. 186(2) applies for purposes of the connected corporation test contained in the definition of qualified small business corporation share.

15 November 89 T.I. (April 90 Access Letter, ¶1179)

The 24-month test will not be met where the taxpayer acquired the shares from her husband less than 24 months before the determination time, and prior to the determination time they were divorced and thus no longer related. The relationship referred to in paragraph (b) must be maintained during the entire 24-month period before the determination time.

19 September 89 T.I. (February 1990 Access Letter, ¶1119)

Where Holdco holds a loan receivable from a related corporation which is not connected ("Opco"), the loan receivable will not be an asset used in an active business carried on in Canada by Holdco if Holdco's ordinary business activity does not include the lending of money.

89 C.R. - Q.11

RC is presently reviewing whether its position in IT-486R, that an asset is used in a business if more than 50% of its use is in respect of that business, is appropriate in applying s. 110.6.

October 1989 Revenue Canada Round Table - Q.12 (Jan. 90 Access Letter, ¶1075)

Proceeds of an insurance policy can taint a corporation even where the proceeds were distributed shortly after their reception by the corporation. The relevant asset test must be met throughout 24-month reference period. Therefore, if the proceeds of insurance caused the corporation to fail the test even for a very short period, the shares will not qualify.

88 C.R. - "Small Business Corporation Shares" - "Background"

The exception in paragraph (d) is designed to preclude circumvention of the 50 percent test by stacking of holding companies."

88 C.R. - F.Q.33

The receipt of life insurance proceeds by a corporation upon the death of a shareholder can breach the 50% test even if the proceeds are paid out as s dividend shortly after receipt [C.R.: 248(1) - "small business corporation"]

88 C.R. - "Small Business Corporation Shares" - "Background"

The exception in paragraph (d) is designed to preclude circumvention of the 50 percent test by stacking of holding companies."

88 C.R. - F.Q. 35

The fair market value of an asset is determined without regard to a mortgage debt on the asset.

Articles

Mallin, "Organizing and Reorganizing to Ensure 'Qualified Small Business Corporation Share' Status", 1990 Canadian Tax Journal, pp. 745, 1026.

Truster, "The Capital Gains Exemption", 1989 Conference Report, c. 12.

Share of the Capital Stock of a Family Farm Corporation

Administrative Policy

24 December 2012 T.I. 2012-0457881E5 - Share of a capital stock of a family farm

After stating that the comments in 2000-0011595 were still valid, CRA quoted with approval the statemnt therein that:

property that is owned by the corporation and that was used by the corporation or other eligible person principally in the course of carrying on the business of farming in Canada will satisfy the requirements of subparagraph (b)(i) [sic], even if the corporation did not own the property while the property was so used.

CRA then elaborated:

while the family farm corporation must otherwise meet the requirements of subparagraph 110.6(1)(a) of the definition of "share of the capital stock of a family farm corporation" for a continuous 24-month period during which that corporation actually owned the property for that entire 24-month period, for the purposes of subparagraph 110.6(1)(b) of the definition, the CRA would take into account the use of a particular property by a person who was an eligible person during a period of time where such property was otherwise owned or rented by such eligible person(s) before it was acquired by the family farm corporation.

24 August 1995 T.I. 5-951846

"As regards the 24-month period [in para. (a)], it does not have to be the 24-month period immediately prior to the determination time. However, the longer the property owned by the corporation is used for other than farming purposes prior to the determination time, the less likely [it is that] the shares of the corporation will meet para (b) of the definition."

92 C.R. - Q.53

If throughout an 8-year period that a corporation owns a particular piece of land, the corporation is carrying on a farming business in which one of the qualifying individuals in the definition is actively engaged on a regular and continuous basis, the land will be considered among the eligible properties insofar as the 50% test is concerned during the period of time it was used in the farming business. However, at the time of disposition of shares of the corporation, the particular piece of land will not qualify as an eligible property for purposes of the "all or substantially all" test in paragraph (b) unless it has been used for more than four of the eight years that the property was owned by the corporation in the course of carrying on the business of farming in Canada by the corporation.

1 October 1991 T.I. (Tax Window, No. 10, p. 13, ¶1491)

To be actively engaged the individuals' contributions of time and attention to the business would be determinant in its successful operation.

19 February 1990 T.I. (July 1990 Access Letter, ¶1328)

Where a farm house owned by the corporation accommodates only individuals who are actively engaged in the farming business and their family members, the farm house will qualify as an asset used in the farming business. Assuming that all the conditions of subsection 70(9.2) are met, the shares could be transferred on a rollover basis to the son of the deceased farmer/shareholder and the capital gains exemption could be utilized by the estate.

Subsection 110.6(1.3) - Property used in a farming business

Administrative Policy

9 June 2015 T.I. 2014-0554381E5 F - Copropriété par indivision - partage de biens

Mr A held land used by him in farming in co-ownership with his brother. Following a partition and cessation of farming, Mr A became the sole owner of the land and sold it to a third party. What was the date of Mr A's acquisition for purposes of s. 110.6(1.3)(a) and (c)? CRA stated (TaxInterpretations translation):

The fractional interest in land which Mr A held from the death of his father is deemed under paragraphs 248(20)(a) and (b) to have not been acquired or disposed of by him. As he acquired that interest before 18 June 1987, paragraph 110.6(1.3)(c) applies to that interest.

In accordance with 248(20)(d), Mr A is deemed to have acquired the fractional interest that his brother held in the land. As that was not acquired before 18 June 1087, paragraph 110.6(1.3)(a) applies to that interest.

Subsection 110.6(2) - Capital gains deduction — qualified farm property

Cases

Fournie v. Cromarty, 2012 DTC 5011 [at 6563], 2011 ONSC 6587

The deceased owned three farm properties. He bequeathed one to the applicants but specified that "capital gains taxes and probate fees, if any, that are attributable to this property shall be charged to or paid by the beneficiaries of the said property." His will also stated that, unless otherwise provided, any taxes determined as of the date of his death be paid out of residue.

The defendant argued that the capital gains tax attributable to the applicants' property was the difference between the estate's tax payable, and the amount that would have been payable but for the existence of the farm property bequeathed to the applicants. This would have the effect of excluding the applicants from the benefit of the capital gains exemption for qualifying farm property.

Hockin J. agreed with the applicants that the capital gains tax (and hence the exemption) should be attributed to each property based on their value in proportion to the entire estate, because that approach accorded with the apparent intentions of the deceased. A taxpayer's capital gains are determined in aggregate, not on a property-by-property basis.

Administrative Policy

3 February 2015 T.I. 2015-0567231E5 - Qualified farm or fishing property

The taxpayer inherited land from her husband that that had been farmed by him and their son, but neither she nor her son continued the farming operation. Would renting the land for cash or under a sharecropping arrangement affect the availability of the lifetime capital gains exemption on a subsequent sale of the land? In responding favourably, CRA paraphrased the ownership, gross revenue and use tests, and stated:

As long as the above requirements are met prior to the disposition of the land, the fact that the land was not used by you in any farming business would not prevent such land from being considered as QFFP.…[T]he crop share received by a landlord in a sharecropping arrangement is rental income and not income from farming.

7 January 2013 T.I. 2012-0460791E5 - Qualified Farm Property & Oil Reserves

In response to a question "as to whether a taxpayer whose farm property meets the definition as a "qualified farm property" ("QFP") within the meaning of subsection 110.6(1)...will be eligible to claim the capital gains deduction under subsection 110.6(2) on a subsequent disposition of the farm property in circumstances where petroleum or natural gas reserves are discovered on the property," CRA responded:

any real property the principal value of which depends on its petroleum, natural gas or related hydrocarbon content will constitute a "Canadian resource property" as defined in subsection 66(15) of the Act by virtue of paragraph (c) of that definition. For these purposes "principal" means more than 50%. Where the taxpayer owns one right that includes both the surface right and the subsurface right, and more than 50% of the value of the real property depends on the petroleum or natural gas reserves, the right would constitute a Canadian resource property and the disposition of the right would result in the tax consequences described in the previous paragraph [i.e., income inclusion under ss. 66.2(1) and 59(3.2)(c), if a negative CCDE balance arises]. Consequently... the proceeds received from the disposition of the right will not give rise to a capital gain such that the capital gains deduction under subsection 110.6(2) will not be available, as the amount determined under paragraph 110.6(2)(d) of the Act in respect of that disposition would be nil.

24 June 1992 T.I. 5-920895 -

Where a father transfers farm property to his children under s. 73(3) and the children immediately thereafter dispose of the farm property to a related party, such as a family farm corporation, the gain will be that of the father rather than the children if they sold the property as agents of their father. Alternatively, GAAR may be relevant, or the disposition by the children may be on income account.

6 September 89 T.I. (February 1990 Access Letter, ¶1117)

Where a farmer transfers his farm to his adult children pursuant to ss.73(3)(a) and (b) and immediately thereafter the children sell the farm property in an arm's length transaction, the capital gains exemption will be available to the children provided they have no history of real estate trading.

29 Aug. 89 T.I. (Jan. 90 Access Letter, ¶1085)

GAAR would not apply to a transaction whereby an individual transferred his qualified farm property to a wholly-owned subsidiary in consideration for consideration comprising: boot equal to the adjusted cost base of the property plus $500,000; and shares. Had there been a proposal to repeal or reduce the capital gains exemption, the response might be different.

Subsection 110.6(2.1) - Capital gains deduction — qualified small business corporation shares

Administrative Policy

4 June 2012 T.I. 2012-0439271E5

Where an inter vivos personal trust has itself satisfied the 24-month holding test in para. (b) of the qualified small business corporation shares definition and it then realizes a capital gain from the disposition of such shares, it may make a designation under s. 104(21) and (21.2) in respect of a Canadian resident individual who has only been a beneficiary for 12 months prior to the share sale.

24 March 1994 T.I. 933164 (C.T.O. "Qualified Small Business Corporation Shares")

The capital gains exemption limits are calculated at the partner rather than the partnership level, given that a partnership is not a person for purposes of calculating taxable income (as opposed to income).

11 January 1993 T.I. (Tax Window, No. 27, p. 14, ¶2358)

A capital gain realized on a cash distribution of paid-up capital on preferred shares that constitute qualified small business corporation shares and that have a low adjusted cost base will be eligible for the enhanced exemption, without application of GAAR, even if the distributed funds are immediately loaned back to the corporation.

18 Aug. 89 T.I. (Jan. 90 Access Letter, ¶1082)

Mr. A, who owned 100% of the common shares of Opco, transfers 1/2 of those shares to Opco in exchange for preferred shares of Opco having a fair market value of $500,000 and a paid-up capital equal to the paid-up capital of the transferred common shares. The amount elected under s. 85(1) is $500,000. Mr. A will be able to claim the capital gains exemption in respect of this transaction.

88 C.R. - F.Q.38

S.110.6(2.1) will apply to the realization of a $100,000 capital gain from the disposition of a qualified small business corporation share, and the individual's ability to claim a deduction in the future under s. 110.6(3) will not be impaired.

Subsection 110.6(3)

Administrative Policy

11 September 1992 T.I. (Tax Window, No. 23, p. 18, ¶2176)

A person who is deemed to be resident in Canada by virtue of the sojourning rule in s. 250(1)(a) is eligible for the capital gains deduction unless the taxpayer's sojourn in Canada cannot reasonably be considered to have been arranged primarily for a bona fide purpose other than to obtain the capital gains exemption.

2 February 1990 T.I. (July 1990 Access Letter, ¶1329)

It is RC's position that an individual's taxation year ends on the date of his death. Accordingly, his death part way through the year is not inconsistent with the requirement that he be "resident in Canada throughout the year".

Articles

Dunbar, "Forward Participation Share May Produce Tax-Exempt Gain With Minimal Downside Risk for Executive", Taxation of Executive Compensation and Retirement, February 1990

Issuance, at a nominal cash subscription price, of shares which only participate to the extent that the common shares increase in value, may produce the same economic effect as a stock option plan which is eligible for the capital gains exemption.

Singer, "Revenue Canada Accepts Arrangements Designed to Make Capital Gains Exemption Available Under Employee Stock Purchase Plan", Taxation of Executive Compensation and Retirement, December 1989/January 1990

RC has indicated that it would not apply GAAR where Holdco, rather than Opco, undertakes to buy back shares issued to employees in stipulated circumstances, in order to ensure capital gains rather than deemed dividend treatment.

Subsection 110.6(6) - Failure to report capital gain

See Also

Adams v. The Queen, 96 DTC 1737 (TCC)

A finding in previous tax evasion proceedings brought against the taxpayer that the taxpayer's gains from the disposition of real estate (and other transactions) were exempt from tax appeared to have subsumed a finding that his failure to report the gains had not been done knowingly and had not been attributable to gross negligence. Accordingly, the Minister in reassessing the taxpayer was required to allow the deduction under s. 110.6(6) in light of the doctrine of issue estoppel.

Administrative Policy

93 C.R. - Q. 54

The fact that a taxpayer did not report a capital gain where he had reasonable grounds to believe that the disposition of the asset did not result in a capital gain would not, by itself, trigger the application of s. 110(6).

June 1990 Meeting of Alberta Institute of Chartered Accountants (November 1990 Access Letter, ¶1499, Q. 8)

A taxpayer will be allowed the capital gains deduction on all adjustments to include a capital gain previously not reported by him, unless the addition of that unreported income would be subject to a penalty under s. 163(2).

Subsection 110.6(7) - Deduction not permitted

Administrative Policy

3 June 2014 T.I. 2013-0503511E5 F - Discretionary Dividend Shares

Mr. X effects an estate freeze under which a portion of his Class A-1 shares of Opco (a small business corporation), being all the outstanding shares, are exchanged under s. 51 for Class B non-voting redeemable retractable non-participating shares. Opco then pays a stock dividend to Mr. X on his remaining Class A-1 shares consisting of non-voting Class C redeemable retractable shares discretionary-dividend shares. Mr. X transfers the Class C shares to a newly-incorporated corporation of which he is the sole shareholder ("Holdco") in consideration for common shares, electing under s. 85(1). In order to purify Opco for qualified small business corporation share purposes, dividends are annually paid on the Class C shares to Holdco. Several years later, Holdco and Mr. X sell their Opco shares to a third party for their fair market value.

After noting that the question as to whether s. 110.6(7)(b) applied to deny the capital gains exemption on the disposition by Mr. X of his Class A-1 and B shares depended on the fair market value (FMV) of the Class C shares, CRA noted that their FMV could exceed their redemption value in light of their holders right to receive substantial pre-established dividends.

24 October 2012 Memorandum 2012-0456711I7 F - Inadmissibilité à la déduction pour GC

Contains a general discussion of the series of transactions doctrine in the context of a proposes asessment under s. 110.6(7)(b). CRA notes that under Copthorne, a series of transactions can include the prospective or retrospective attachment of a related transaction to the series.

9 March 1995 T.I. 5-943025 -

Where two shareholders of a CCPC decided, in December 1993, to undertake a butterfly reorganization (which actually was undertaken in August 1994) and the two shareholders filed the capital gains election in respect of their shares, the resulting deemed capital gain could form part of the series of transactions to the same extent as an actual disposition. "Although the shareholders could not have formed the intention to file the capital gains election at the time the decision was made to enter into a reorganization, nevertheless, if they had formed the intention to dispose of their shares at that time, the reorganization and the filing of the capital gains election could be considered to form part of the same series of transactions and events."

14 December 1992 Memorandum (Tax Window, No. 30, p. 4, ¶2488)

S.110.6(7)(b) will not apply to a transaction or a series of transactions intended to make shares of a company qualify as qualified small business corporation shares, provided that during the course of the purification reorganization, a property has not been acquired by a corporation for consideration that does not approximate its fair market value. S.110.6(7) would not apply to butterfly transactions if a subsequent disposition of property to an arm's length person, or a subsequent increase in the interest in any corporation by such person, occurred as part of the series of transactions because the transactions would not be exempt from the provisions of s. 55(2) by virtue of s. 55(3)(b).

10 January 1992 Memorandum (Tax Window, No. 17, p. 16, ¶1773)

Where, in order to accommodate the sale by the other shareholder (Mr. A) of his shares of the corporation, Mr. B agrees that following the purchase the corporation will spin-off assets that are not wanted by the purchaser in a butterfly reorganization, s. 110.6(7) will apply to deny the capital gains exemption to Mr. A.

90 C.R. - Q19

Where one shareholder sells his shares of a corporation which has butterflied out a portion of its property to the other shareholder, whether the sale of the shares is part of the butterfly series of transactions is a question of fact.

89 C.R. - Read Paper (C.18)

s. 110.6(7)(a) "is quite broad and is not restricted to obvious cases ..."

Articles

McKnight, "Hidden Problems in Selling Employee Ownership", Canadian Current Tax, October 1994, p. 7

Discussion of the use of market makers for the purchase of employee shares in private companies.

Subsection 110.6(8) - Deduction not permitted

Administrative Policy

8 March 1994 T.I. 932927 (C.T.O. "Capital Gains Exemption")

The determination of what is a significant part of a capital gain in many cases can be ascertained by reference to the proportion or percentage of the capital gain that is attributable to the non-payment of adequate dividends, but there may be circumstances in which it is appropriate to consider the dollar amount of the capital gain that is so attributable.

One must take into account the time-value of unpaid dividends in determining whether a significant part of a capital gain is attributable to failure to pay dividends.

17 November 1992 T.I. 903665 (September 1993 Access Letter, p. 417, ¶C109-143)

Where an individual transfers non-prescribed shares that have an ACB of nil and a fair market value of $200,000, $35,000 of which is attributable to the fact that dividends were not paid on them, to a corporation and an agreed amount of $165,000 is elected under s. 85(1), s. 110.6(8) will not apply because even if dividends of $35,000 had been paid, a capital gain of $165,000 would have been realized.

92 C.R. - Q.56

RC has no mechanical guidelines as to what constitutes "a significant part of the capital gain", but it is prepared to give advance rulings.

1992 A.P.F.F. Annual Conference, Q. 8 (January - February 1993 Access Letter, p. 53)

Where a corporation has issued voting participating shares that are not prescribed shares because of the conversion privilege, the average annual rate of return on those shares will be determined based on the assumption that the proceeds to be received by the investor upon disposition of the shares are $100. One must not take into account the accrued capital gain on the shares in applying s. 110.6(8). RC is generally prepared not to apply the provision to a transaction whose object is to crystallize the capital gains exemption.

1992 A.P.P.F. Annual Conference, Q. 7 (January - February 1993 Access Letter, p. 52)

Where shares issued prior to May 23, 1985 on an s. 85 rollover have a paid-up capital equal to the market value of the transferred property, a capital gain arising on a subsequent reduction of the paid-up capital will not be subject to s. 110.6(8) provided that the fair market value of the shares issued upon the previous transfer was equal at that time to the fair market value of the transferred property.

24 February 1992 T.I. (Tax Window, No. 17, p. 4, ¶1762)

The gain on a disposition of common shares of a corporation could be tainted by the non-payment of dividends on preferred shares of that corporation even though such preferred shares previously had been disposed of or redeemed.

10 January 1992 Memorandum (Tax Window, No. 17, p. 13, ¶1773)

Where an individual holds all the common shares and preferred shares of B Ltd., and there is an accrued gain of $400,000 on the common shares, $50,000 of which may be attributable to the fact that the accrued but unpaid dividends on the preferred shares of B Ltd. total $50,000, then the individual can roll his common shares of B Ltd. into Newco at an elected amount of $350,000, thereby giving rise to a capital gain that is not subject to s. 110.6(8); however, s. 110.6(8) will apply to a $50,000 gain on the sale of the shares of Newco.

30 November 1991 Round Table (4M0462), Q. 11.3 - Scope of Subsection: 110.6(8) of the I.T.A. (C.T.O. September 1994)

The test in s. 110.6(8) is based on the total gain rather than on the portion thereof that is exempt. In a situation where the unpaid dividends on shares giving rise to a gain of $2 million is $500,000, this would be significant enough to permit s. 110.6(8) to be applied.

10 and 11 July 1991 T.I. (Tax Window, No. 6, p. 11, ¶1347)

Where no dividends are paid on preferred shares while they are outstanding and on their redemption, it is a question of fact whether a significant part of the capital gain arising on the disposition of the common shares of the same corporation would be attributable to the fact that dividends were not paid on the preferred shares. Even where a "catch-up" dividend is paid on the preferred shares around the time of their redemption, a significant portion of the capital gain on the common shares may be attributable to the fact that payment of the preferred share dividends was deferred.

24 June 1991 T.I. (Tax Window, No. 4, p. 2, ¶1313)

Where, in order to satisfy the 24-month asset test, it is agreed between the vendor of shares and the purchaser that the vendor's common shares will be immediately changed into cumulative preference shares which then will be purchased in two-years' time, s. 110.6(8) will not apply assuming that the stipulated dividends are paid on the preferred shares. The vendor's capital gain on the preferred shares will be attributable to the period of time prior to their change from common shares.

15 February 1991 T.I. (Tax Window, Prelim. No. 3, p. 24, ¶1120)

A reasonable and prudent investor should normally expect to receive dividends on preferred shares relating to the issue price paid therefor. Accordingly, it would not be sufficient for the dividend rate on high-low preferred shares issued to individuals on the incorporation of their businesses to be calculated on the paid-up capital rather than the redemption value of their shares.

20 March 1990 T.I. (August 1990 Access Letter, ¶1380)

$200,000 of the accrued gain of $1 million on shares (having a nominal ACB) of Opco, whose sole shareholder is Mr. A, is attributable to the fact that dividends were not paid on a class of preferred shares that have since been redeemed. When Mr. A transfers all his shares in Opco to Holdco for shares of Holdco, and designates an agreed amount of $500,000, s. 110.6(8) will not apply because even if the dividends had been paid on the preferred shares, the fair market value of the common shares of Opco would have exceeded $500,000.

21 February 1990 T.I. (July 1990 Access Letter, ¶1330)

The provisions of s. 110.6(8) should not apply to preferred shares with a paid-up capital and redemption amount equal to the fair market value of the assets in exchange for which they were issued.

31 January 1990 T.I. (June 1990 Access Letter, ¶1269)

Where 90% of the common shares of Opco owned by Father were exchanged for redeemable preference shares under an s. 86 reorganization, insufficient dividends paid on the preference shares could maintain the value of the preferred shares which might not have been the case if a reasonable rate of return had been paid thereon. Accordingly, insufficient dividends paid on the preference shares could result in the realization of a significant capital gain.

RC has not established any guidelines on what is a significant part for purposes of s. 110.6(8).

87 C.R. - Q.60

RC will not rule on the factual question of whether a gain is attributable to a low dividend rate.

Articles

Brender, "The De Minimis Dividend Test Under Subsection 110.6(8)", 1993 Canadian Tax Journal, Vol. 41, No. 4, p. 808.

Subsection 110.6(9) - Average annual rate of return

Administrative Policy

11 October 2013 APFF Roundtable Q. , 2013-0495641C6 F

X and Y, who deal with each other at arm's length, each effect an estate freeze, by exchanging their 100 common shares of Opco (i.e., 50 shares each), having a cost and legal paid-up capital of $100 for preferred shares with a redemption amount of $2M and with dividends permitted in the range of 0% to 10%, and with Trust X and Trust Y each subscribing for 50 new common shares. Should the average annual rate of return be calculated on the paid-up capital of $100 or on the $2M redemption amount?

Before indicating that such return should be based on the $2M amount payable for the preferred shares issued in the estate freeze, CRA stated (TaxInterpretations translation):

[A] knowledgeable and prudent investor would normally seek to obtain a dividend rate as a function of the amount payable by him or her to acquire the share.

18 May 1994 T.I. 5-940741 -

In response to a question as to whether the "average annual rate of return" is calculated based on the original issue price of shares, RC stated that they were of the view "that the return on the shares that are substituted with new shares must be taken into account in determining the annual rate of return and that the average annual rate of return is usually calculated on the basis of the amount invested by a knowledgeable and prudent investor who purchased the shares on the day they were issued".

14 June 1990 T.I. (November 1990 Access Letter, ¶1528)

Where in 1982 prior to the introduction of Part II tax, the shareholders of Opco transferred each common share of Opco to Holdco in consideration for one common share and one special share of Holdco, and no dividends ever were paid on the special shares, s. 110.6(a) will apply to deny the capital gains exemption where any significant part of any capital gain from the disposition of a share was attributable to the non-payment of dividends on the special shares.

7 June 1990 Memorandum (November 1990 Access Letter, ¶1529)

If upon the issuance of the shares in question it was understood that the profits of the corporation would be reinvested, the expected rate of return probably would be lower.

Subsection 110.6(14) - Related persons, etc.

Paragraph 110.6(14)(a)

Administrative Policy

2 May 2013 T.I. 2013-0481361E5 F - Ordre de disposition d'actions AAPE

The 300 outstanding shares of Corporation A are held by three unrelated individuals (A, B and C) as to 100 each. After the death of C, A and B acquire 50 shares each from his estate.

In order to eliminate $400,000 of liquid assets (representing 1/3 of its fair market value) from Corporation A prior to a sale of 200 of the shares to a purchaser, the shares purchased from the estate are transferred by A and B to a Holdco in a value for value exchange, with the transferred shares apparently being redeemed in order to "purify" Corporation A so as to qualify as a small business corporation.

After adverting to the requirement in the QSBC definition that the shares disposed of by A and B to the purchaser have been owned by them or a related person for 24 months, CRA stated (TaxInterpretations translation):

Paragraph 110.6(14)(a) specifies that a taxpayer is deemed to dispose of shares which are identical property in the order in which they were acquired, i.e., following the FIFO rather than LIFO method.

19 September 1990 T.I. (Tax Window, Prelim. No. 1, p. 14, ¶1031)

Where on an amalgamation of A Co. and B Co., the shareholder receives 100 shares of Amalco of which 90 were in exchange for his A Co. shares and 10 were in exchange for his B Co. shares, then on a subsequent disposition of a portion of his shares of C Co., he will be considered to have first disposed of those shares of Amalco which were issued in exchange for the shares of A Co., if he had acquired the shares of A Co. prior to the shares of B Co.

Paragraph 110.6(14)(b)

See Also

Pellerin v. The Queen, 2015 CCI 130

At approximately 18 months of age, Mika Pellerin received a distribution under s. 107(2) of small business corporation shares from the family trust and immediately sold them at a gain. Boyle J found that under the Quebec general law, when Mika was born he was retroactively deemed to have been a trust beneficiary for his previous nine months as a fetus. See summary under s. 110.6(1) - qualified small business corporation share.

Chartier v. The Queen, 2008 DTC 4627, 2007 TCC 37

On the same day that the owners of non-voting shares agreed to sell those shares and 49% of the voting shares of a corporation to a non-resident controlled purchaser, minority shareholders of the corporation entered into an Option Agreement to sell the balance of the voting shares along with some preferred shares, with such options being exercised approximately three months later in the subsequent taxation year.

In finding that s. 110.6(14)(b) applied to deem the corporation to be a Canadian-controlled private corporation notwithstanding the right to acquire control under the options, Tardif, J., after noting that the agreement for sale of shares referred to the Option Agreement, stated (at para. 32):

"thus, it is enough for the option to have been contemplated or envisaged in the purchase and sale agreement, and section 3.1 shows that the option in the instant case was so contemplated or envisaged."

Accordingly, the Option Agreements were rights "under" the Agreement of Purchase and Sale. Furthermore, the absence of more clear references under the Agreement of Purchase and Sale to the Option Agreement, so as to eliminate ambiguity in the relationship between the Agreement of Purchase and Sale and the Option Agreement, was a drafting error.

Administrative Policy

13 January 2012 Memorandum 2011-042837 -

certain share put/cal rights contained in a unanimous shareholders agreement would not be considered to be rights "under" a purchase and sale agreement, given that (contrary to the situation in the Chartier decision) such put/call rights were not referred to in the purchase and sale agreement.

88 C.R. - F.Q.39

Routine example.

Paragraph 110.6(14)(c)

Administrative Policy

May 1991 Question and Answer for a Conference (Tax Window, No. 3, p. 17, ¶1223)

Where an individual who owns shares of a corporation bequeathed those shares to his son who in turn sold the shares to his wife, the son's wife will not be beneficiary of her father-in-law's estate, with the result that the period of time during which the shares are owned by the estate will not be included in the 24-month holding period.

Paragraph 110.6(14)(e)

Administrative Policy

22 March 1991 T.I. (Tax Window, No. 2, p. 22, ¶1220)

S.110.6(14)(e) extends the definition of "related persons" for purposes of the enhanced capital gains exemption.

Paragraph 110.6(14)(f)

Administrative Policy

3 March 2014 T.I. 2014-0519071E5 F - Période de détention de 24 mois pour AAPE

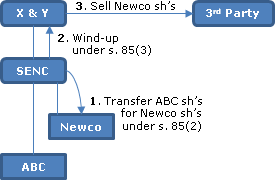

X and Y have been the partners for more than 24 months in "SENC, which for over 24 months has held all the shares of a Canadian-controlled private corporation (ABC) carrying on an active business. SENC transfers its shares of ABC to Newco under s. 85(2), SENC is wound-up under s. 85(3) and shortly thereafter X and Y sell their Newco shares to a 3rd party.

CRA stated (TaxInterpretations translation):