Subsection 111(1) - Losses deductible

Paragraph 111(1)(a) - Non-capital losses

Cases

The Queen v. Merali, 88 DTC 6173, [1988] 1 CTC 320 (FCA)

"There is nothing in the Act to prevent a resident from carrying over non-capital losses incurred when he was a non-resident taxpayer having elected during his non-resident years to be treated as a resident under the terms of subsection 216(1) of the Income Tax Act."

Oceanspan Carriers Ltd. v. The Queen, 87 DTC 5102, [1987] 1 CTC 210 (FCA)

"A corporation which incurs losses from business activities outside Canada when it is neither a resident nor had income from a source in Canada, and thus is not subject to assessment under the Act, is not entitled to deduct such losses to reduce taxable income to nil on income derived after it becomes a Canadian resident."

See Also

Hatt v. The Queen, 2015 TCC 207

The taxpayer, who became a non-resident when she went on unpaid leave from her Canadian job in 2003, retired in 2007 and thereupon received $2497.44 in unused annual leave credits (treated by CRA as income from her Canadian employment under s. 115(1)(a)(i)) and a retiring allowance of $43,255 (taxable under Part XIII rather than Part I). She contributed $22,384 to a registered pension plan which, by virtue of its deductibility under s. 147.2(4)(a), gave rise to a 2007 loss from employment under s. 5(2). After her return to Canada in 2010, she deducted this amount from her taxable income as a non-capital loss.

CRA disallowed the carry-forward on the basis that s. 147.2(4) does not allow the carry-forward of RPP contributions but rather requires that the deduction be made "in the year" they are contributed - and this limitation's "purpose would be frustrated by the availability of non-capital losses under section 111" (para. 35).

In allowing the taxpayer's appeal, D'Arcy J stated (at para. 48):

[P]ursuant to the definition in subsection 111(8), the Appellant incurred a non-capital loss from employment of $20,302 in her 2007 taxation year. Pursuant to subsection 111(1)(a), such loss may be carried forward and deducted when determining the Appellant's 2010 taxable income.

Administrative Policy

19 August 2015 T.I. 2015-0589611E5 - loss consolidation arrangements

In loss consolidation transactions: are they permitted to occur amongst related parties that are not affiliated? Does it matters whether or not the "lossco" has any source of funds to cover dividend payments other than the interest income paid by a "profitco".Does CRA requires a commitment letter issued by a third party to confirm that the proposed transactions are commercially plausible?

CRA responded:

S3-F6-C1… paragraph… 1.71… indicates that such loss consolidation arrangements could be undertaken by parties that are related but not affiliated (as well as parties that are both related and affiliated and parties that are affiliated but not related).

…[I\n upstream shareholding situations, the CRA will generally ask for a representation that the issuer of the shares will have other assets from which the dividends will be funded.

...[T]ypically the CRA will request a representation relating to borrowing capacity. In some cases, such as situations where the amount of the debt is substantial, CRA may request a signed letter from a director or other documentation.

2015 Ruling 2014-0559181R3 - Internal Reorganization

CRA provided s. 55(3)(a) and other rulings for spinning off various business divisions of an indirect subsidiary (Bco) of a public corporation to newly-incorporated sisters (Cco, Dco and Eco). Bco also was the "profitco" in a loss shifting transaction for which a 2012 ruling letter (2012-0437881R3) was received. Those transactions are described as already having been completed (i.e., their set-up but not their unwinding?) In confirming that the transactions described in the second ruling letter would not cause the 2012 rulings to cease to be binding, CRA stated:

Bco, through its XX, will generate sufficient income to absorb the interest expense resulting from the loss consolidation transactions… . Therefore, no modification is required to any of the loss consolidation transactions.

…[N]o new business activities will be created within the corporate group as only existing operations will be transferred into sister corporations… . Moreover, the Proposed Transactions will be made in a tax-deferred manner and will not have the effect of creating new tax obligations.

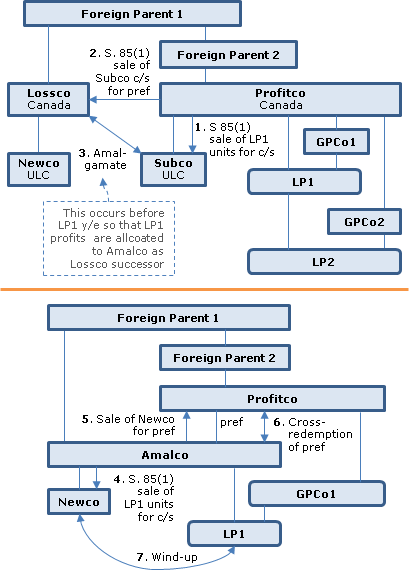

2014 Ruling 2013-0516071R3 - Reorganization

Background

Profitco is wholly-owned by Foreign Parent 2 which, in turn, is indirectly wholly-owned by Foreign Parent 1. Profitco is the limited partner of LP1 and its subsidiary is the GP. LP1 holds all the LP units of LP2, whose GP is another subsidiary of Profitco. Profitco will have positive QTI re LP1. Lossco is wholly-owned by Foreign Parent 1.

Transactions

- Prior to the ruling letter, Profitco transferred its LP1 units to a newly-incorporated unlimited liability company ("Subco") in consideration for Subco common shares, with a joint s. 85(1) election filed. The LP1 partnership agreement will be amended "to clarify that it allocates its income for income tax purposes only to those partners that are partners at the end of its fiscal period."

- Profitco will transfer all its shares of Subco to Lossco under s. 85(1) in consideration for non-voting redeemable retractable preferred shares of Lossco.

- Lossco and Subco will amalgamate, so that XX% of the income of LP1 for its current fiscal period will be allocated to "Amalco."

- After the LP1 year end, Amalco will transfer the LP1 units to a newly-incorporated ULC ("Newco") under s. 85(1) in consideration for common shares.

- Amalco will transfer its common shares of Newco to Profitco under s. 85(1) in consideration for non-voting redeemable retractable preferred shares of Profitco.

- Amalco and Profitco will cross-redeem the two preferred share holdings for notes and set-off the notes.

- Newco will be wound-up.

Rulings

The proposed transactions will not result in any disposition or increase in interest described in ss. 55(3)(a)(i) to (v). S. 34.2(14) will deem Profitco to be a member of LP1 continuously until the end of its XX taxation year for purposes of s. 34.2(13)(a). S. 245(2) will not apply.

2014 Ruling 2014-0543911R3 - loss consolidation

underline;">:

Similar to 2013-0498551R3

.

Proposed Transactions

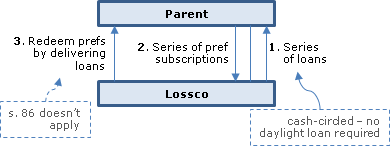

Lossco, which is an indirect subsidiary of Parent and has permanent establishments in various provinces, will make a series of loans, on one or more days, to Parent (also with PEs in various provinces). Parent will use the total proceeds to subscribe for one or more series of redeemable retractable preferred shares of Lossco bearing a cumulative quarterly dividend at a small spread over the interest (payable quarterly) on the loans, (with the resulting Lossco losses thereby effectively transferred to Parent in its xx taxation year being less than its income for that year). Prior to the end of that taxation year, Lossco will redeem the preferred shares by delivering the loans to Parent.

Rulings

. Standard rulings re ss. 20(1)(c), 112(1), 15(1), 56(2), 246(1) and 245(2) (but no provincial GAAR ruling). The delivery of the loans to Parent will not give rise to a forgiven amount.

2015 Ruling 2014-0563151R3 - Loss consolidation

This is essentially identical to 2014-0518451R3 from a year earlier. Briefly, a lossco parent (Lossco) will not transfer losses to a profitco subsidiary (Opco) under typical triangular loss-shifting techniques, because Opco has public preference shareholders and does not wish to incur debt. Accordingly, Lossco will engage in such techniques to transfer losses to a newco subsidiary (Aco), and then transfer Aco to Opco to be wound-up under s. 88(1.1) (2013-0511991R3 and 2013-0496351R3 are similar). More realistically than 2013-0496351R3, the usual borrowing capacity rep is given in relation to the Lossco rather than Aco. The unwinding of the loss transfer transactions will occur on a cashless basis. The Additional Information states:

It is anticipated that the steps described in the Proposed Transactions will be undertaken at the beginning of each future taxation year of Lossco, with new entities to be created having the same attributes as ACo and Newco.

2013 Ruling 2013-0498551R3 - Loss Consolidation

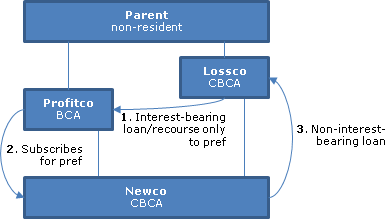

Lossco, an indirect subsidiary of Parent, will make interest-bearing loans to Parent, and Parent will subscribe for redeemable retractable preferred shares of Lossco ("prefs"). On the unwinding, Lossco will redeem the prefs by delivering the loans which it made to Parent. Rulings include interest-deductibility by Parent, and delivery of the loans on the pref redemption not giving rise to a forgiven amount.

2014 Ruling 2014-0525441R3 - loss consolidation arrangement

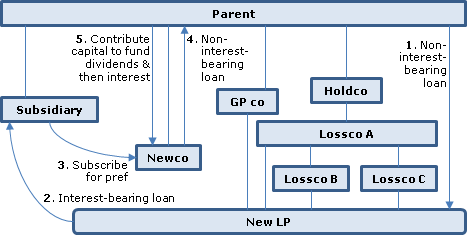

Existing structure

Parent holds Subsidiary, which is profitable, directly, and holds Lossco A (which, in turn, holds Lossco B and Lossco C) through Holdco. In a preliminary transaction, the "New LP Partners," (Lossco A, B and C) will become the limited partners of a new LP ("New LP"), with a newly-incorporated subsidiary of Parent ("GP Co") as the general partner.

Proposed transactions

- Parent will make non-interest-bearing demand loans (the "Parent Loans") to New LP.

- New LP will on-lend these funds at interest to Subsidiary under the "Subsidiary Loans."

- Subsidiary will use such proceeds to subscribe for non-voting redeemable "Preferred Shares" of a newly-incorporated subsidiary of Parent ("Newco").

- Newco will use those proceeds to make non-interest-bearing demand loans (the "Newco Loans") to Parent.

- On each monthly interest payment date, Parent will make a contribution of capital to Newco to fund the Newco Preferred Share dividends, and Subsidiary will pay to New LP the interest then due on the Subsidiary Loans.

- Upon generation of interest sufficient to utilize the non-capital losses of Subsidiary (which is anticipated to occur "on or before the month end in which the Proposed Transactions are initiated,") the transactions will be unwound through: Newco redeeming the Preferred Shares by delivering the Newco Loans to Subsidiary; Subsidiary repaying the Subsidiary Loans by delivering the Newco Loans to New LP; and New LP repaying the Parent Loans by set-off against the Newco Loans.

- New LP, Newco and GP Co will be wound-up (with no capital loss being claimed by Parent respecting its investment in Newco).

Newco and the Losscos will satisfy the applicable corporate solvency tests.

Rulings

: Including interest deductibility to Subsidiary, timing of Ne LP income allocation to Losscos and non-application of ss. 9 and 12(1)(c) to capital contributions received by Newco. SS. 56(2), 15(1), 69(11), 246(1) and 245(2) are not applicable. Provincial GAAR ruling.

2 December 2014 CTF Roundtable, Q2(a)

In a loss consolidation arrangement, "Lossco," which has non-capital losses, lends money to Profitco at a reasonable stated rate of interest and Profitco in turn uses the inter-corporate debt to acquire preferred shares of Lossco. Does the CRA require a positive spread between the dividend yield on the preferred shares acquired with inter-corporate debt and the interest rate on that debt, and must the dividend payor have an independent source of income to pay the dividends? CRA stated:

[I]t is the CRA's policy not to provide rulings without a positive spread between the interest paid and the dividends earned. …[I]n circumstances of upstream shareholding in which a subsidiary acquired dividend paying preferred shares of the parent…[o]ur views… expressed in Income Tax Technical News No. 30…[are], "The key criteria to be met in such situations is the existence of other assets in the parent company that can generate sufficient income to pay the dividends on the preferred shares held by the subsidiary."

2 December 2014 CTF Roundtable, Q2(b)

Must corporations be affiliated or related or both in a loss consolidation arrangement? CRA responded:

The CRA will consider ruling requests where the corporations are related and affiliated, as well as circumstances in which the corporations are related.

…[W]here the corporations are affiliated but not related…the meaning of affiliated will be determined on the same criteria as stipulated in subsection 69(11)… . In other words, where two corporations are not related, but are affiliated, the CRA would consider a loss consolidation arrangement only if the corporations are affiliated by reason of de jure control.

2 December 2014 CTF Roundtable, Q2(c)

Does the decision in the 2013 Federal Budget not to proceed with a corporate group taxation system impact rulings for loss consolidation arrangements? CRA responded:

The 2013 Federal Budget announcement has not had an impact… .It should be noted, however, that where we consider that one of the main reasons for engaging in a loss consolidation arrangement is for the purposes of shifting income among provinces, the CRA may challenge that loss consolidation under provincial GAAR legislation.

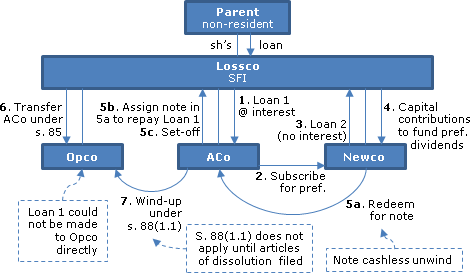

2014 Ruling 2014-0518451R3 - Loss consolidation

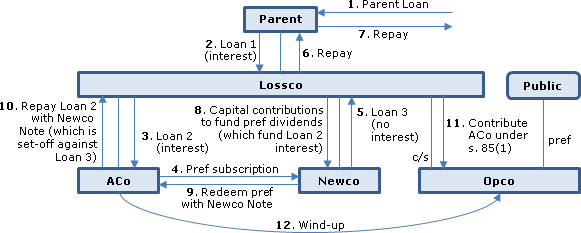

Overview

Loan 2 (in step 3 below) is being made by Lossco (the wholly-owned loss subsidiary of Parent) to Aco (so as to generate losses in Aco for later transfer under s. 88(1.1) to Opco), instead of being made directly to Opco, "to ensure that Opco, which is a public corporation, does not incur debt in order to implement the loss utilization." Furthermore, "any shift of income between provinces will be incidental to the Proposed Transactions."

Proposed transactions

- Parent will borrow the Parent Loan.

- Parent will use the proceeds to make Loan 1 to Lossco. "Lossco will have the borrowing capacity to obtain a daylight loan, in an amount equal to the amount of Loan 1, directly from an arm's-length financial institution."

- Lossco will use the total proceeds received under Loan 1 to make Loan 2 (bearing interest) to ACo.

- ACo will use such proceeds to subscribe for Newco Preferred Shares. (Although these shares will be term preferred shares, they not be acquired by ACo "in the ordinary course of ACo's business.")

- Newco will use such proceeds to make Loan 3 (not bearing interest) to Lossco.

- Lossco will repay Loan 1.

- Parent will repay the Parent Loan.

- Lossco will make periodic contributions of capital to Newco to fund accruing dividends on the Newco Preferred Shares, with Aco in turn servicing Loan 2 interest. The contributions will be recorded as contributed surplus under IFRS.

- After generation of the requisite losses in Aco, Newco will redeem the Newco Preferred Shares of ACo in consideration for the Newco Note.

- ACo will repay Loan 2 by assigning the Newco Note to Lossco - and Lossco and Newco will agree to setoff the amount due under Loan 3 against the amount due under the Newco Note.

- Lossco will transfer all of its ACo Common Shares to Opco in exchange for additional common shares of Opco under s. 85(1).

- In the same taxation year, the winding-up of Aco will be commenced, and "ACo will file articles of dissolution with the appropriate Corporate Registry within a reasonable time after the winding-up resolution is passed."

Rulings

: Including interest deductibility to ACo on Loan 2 and non-application of ss. 9 and 12(1)(c) to capital contributions received by Newco. Ss. 56(2), 15(1), 246(1) and 245(2) are not applicable. Provincial GAAR ruling. Dividends received by Aco on its Newco Preferred Shares (which are term preferred shares) will be deductible under s. 112(1).

2014 Ruling 2013-0511991R3 - Loss consolidation

Structure

Lossco, which is a specified financial institution with non-capital losses, is a subsidiary of non-resident parent, and serves as the holding company for Opco.

Proposed transactions

- Lossco will use the proceeds of a daylight loan to make Loan 1 to a newly-incorporated special-purpose subsidiary (ACo). Loan 1 will be interest-bearing and its amount "will not exceed the amount that ACo could reasonably be expected to borrow from an arm's-length financial institution."

- ACo will use the total proceeds received from Loan 1 to subscribe for non-voting redeemable retractable preferred shares (the Newco Preferred Shares) of Newco, which is a newly-incorporated subsidiary of Lossco.

- Newco will use such proceeds to make a non-interest-bearing loan to lossco (Loan 2), with Lossco repaying its daylight loan.

- Lossco will annually make contributions of capital to Newco in order that it can pay the accrued dividends on the Newco Preferred Shares which, in turn, will fund th epayment of the accrued interest on Loan 1.

- The unwinding of the transactions will be accomplished by: Newco redeeming the Newco Preferred Shares held by ACo in consideration for a non-interest bearing promissory note (the "Newco Note"); ACo will repaying Loan 1 by assigning the Newco Note to Lossco; and Loan 2 and the Newco Note being set-off.

- Lossco will transfer all its ACo shares to Opco in exchange for Opco common shares, electing under s. 85(1), and Aco will be wound-up into Opco, with articles of dissolution being filed "within a reasonable time after the winding-up resolution is passed."

Reason for Aco

"Due to regulatory constraints and the potential liability issues that may arise with respect to the operations of Opco, it is not feasible from a business perspective to have Lossco make Loan 1 directly to Opco. Instead, Loan 1 is being made to ACo to ensure that Opco does not incur debt in the course of executing the loss consolidation."

Rulings

: Including interest deductibility to Profitco on Profitco Note and non-application of ss. 9 and 12(1)(c) to capital contributions received by Newco. SS. 56(2), 15(1), 246(1) and 245(2) are not applicable. Provincial GAAR ruling.

S. "88(1.1) will apply after the winding up of ACo into Opco….[and] [f]or this purpose, ACo will not be considered to have been wound up until it has been formally dissolved."

13 June 2014 T.I. 2014-0522251E5 - Independent source of income for loss utilization

Lossco, which is developing a commercial use building, lends money to Profitco (a related corporation) at interest and Profitco uses the proceeds to invest in preferred shares of Lossco. Lossco does not yet have an independent source of income. How does the CRA policy that the loss corporation have an independent source of income apply? CRA stated:

Income Tax Technical News No. 30 (May 21, 2004) makes the following comment regarding the CRA's views on typical loss utilization structures:

- "While we have not reached the point where we would state that C.R.B. Logging is no longer good law, we have provided rulings on some upstream shareholding situations. The key criteria to be met in such situations is the existence of other assets in the parent company that can generate sufficient income to pay the dividends on the preferred shares held by the subsidiary".

Whether there are assets in the parent company that can generate sufficient income to pay the dividends on preferred shares held by the subsidiary is a question of fact.

2013 Ruling 2013-0512321R3 - Loss Consolidation

Conventional loss shift between two sister corporations (Lossco and Profitco) utilizing preferred shares and interest-bearing loan.

2013 Ruling 2013-0504301R3 - Loss Consolidation

Background

Lossco, which is a Canadian public corporation with a portion of its shares held by Parentco, wishes to transfer losses to Profitco, which is a wholly-owned subsidiary of Cco which in turn, is a wholly-owned subsidiary of Bco, which is a Canadian public corporation whose shares are widely held but which is controlled by Lossco. This will be accomplished by Lossco selling cumulative preferrred shares of a newly-incorporated subsidiary to Profitco in consideration for an interest-bearing note of Profitco. The borrowing capacity of Bco, and of Lossco and its subsidiaries, significantly exceeds the maximum amount required to complete the transactions. losses being transferred to Profitco on a s. 88(1.1) winding-up.

Proposed transactions

- Lossco will borrow under a daylight loan from an arm's length financial institution or a related entity.

- Lossco will use such proceeds to subscribe for non-voting cumulative redeemable retractable preferred shares (the "Newco Preferred Shares") of a newly-incorporated subsidiary ("Newco").

- Lossco will transfer the Newco Preferred Shares to Profitco in consideration for an interest-bearing debenture (the "Profitco Note"), recourse under which will be limited to the Newco Preferred Shares and which will have a security interest in the Newco Preferred Shares.

- Newco will use the proceeds in 2 to make a non-interest-bearing loan to Lossco under the "Lossco Note."

- Lossco will repay the daylight loan.

- At least quarterly, Lossco will make a contribution of capital to Newco to fund the payment by it of accrued dividends on the Newco Preferred Shares held by Lossco, with Profitco then paying all accrued and unpaid interest on the Profitco Note.

- In connection with the unwinding, Newco will redeem the Newco Preferred Shares and deliver the Lossco Note to Profitco as payment of the redemption proceeds, with the Lossco Note and the Profitco Note then set-off.

- Newco will be wound-up into Lossco pursuant to s. 88(1).

Rulings

Including interest deductibility to Profitco on Profitco Note and non-application of ss. 9 and 12(1)(c) to capital contributions received by Newco. SS. 56(2), 15(1),246(1) and 245(2) are not applicable.

The general anti-avoidance provision of a province with which the Government of Canada has entered into a tax collection agreement will not be applied, as a result of the Proposed Transactions, in and by themselves, to determine the tax consequences confirmed in the rulings given above, in respect of a taxation year in respect of which such a tax collection agreement is in effect.

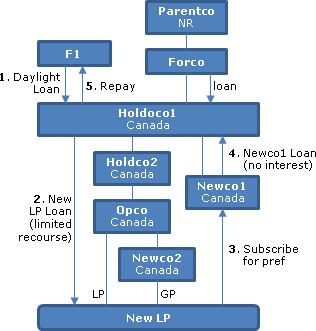

2014 Ruling 2013-0483491R3 - Loss Consolidation Arrangement

Existing structure/debt indenture

Parentoco, a widely-held non-resident corporation, holds Forco, a non-resident holding company, which holds Holdco 1, which holds Holdco 2, which holds Opco, the latter three subsidiaries being taxable Canadian corporations. In the transactions below, Opco is a limited partner of New LP to limit the potential claims and recourses of creditors of New LP (including Holdco 1) against assets of Opco, so as to comply with the provisions of a Debt Indenture.

Proposed transactions

.

- Holdco 1 borrows on a daylight basis from the Financial Institution.

- Holdco 1 makes the "New LP Loan" to a partnership (New LP) formed by a newly-incorporated subsidiary of Opco, as general partner (Newco 2), and Opco as limited partner. Holdco 1's recourse is limited to the Newco 1 Preferred Shares described in 3 below. "The borrowing capacity of Holdco 2 and its subsidiaries ("Holdco 2 Subsidiary Group Borrowing Capacity") is equal to or exceeds the principal amount of the New LP Loan."

- New LP subscribes for cumulative preferred shares of a newly-incorporated subsidiary of Holdco 1 (Newco 1). The dividends payable on the Newco 1 Preferred Shares will exceed the aggregate of the interest accrued on the New LP Loan and nominal incidental expenses of New LP.

- Newco 1 makes a non-interest-bearing demand loan to Holdco 1 (the "Newco 1 Loan").

- Holdco 1 repays its daylight loan.

- At least annually, Opco and Newco 2 will make pro rata cash capital contributions to New LP to fund interest on the New LP Loan;

- New LP will pay the interest on the New LP Loan.

- Holdco 1 will make contributions of capital to Newco 1 to fund dividends payable on the Newco 1 Preferred Shares held by New LP.

- On unwinding the loss consolidation arrangement, (a) Newco 1 will redeem the Newco 1 Preferred Shares by assigning its Newco 1 Loan receivable to New LP, (b) New LP will repay the New LP Loan by set-off with the Newco 1 Loan, (c) Newco 1 will be wound-up into or amalgamated with Holdco 1; and (d) Newco 2 will be wound-up into or amalgamated with Opco, with the result that New LP will cease to exist.

Rulings

Including re s. 20(1)(c) deductions of New LP, utilization of streamed and non-streamed losses by Losscos and non-application of s. 12(1)(x) re contributions of capital to Newco 1.

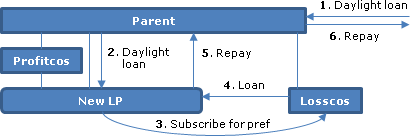

2013 Ruling 2012-0458091R3 - XXXXXXXXXX - loss consolidation

Proposed transactions

- Parent borrows on a daylight basis from the Financial Institution.

- Parent makes a daylight loan to a partnership (New LP) formed by the Profitcos (Parent and two wholly-owned subsidiaries – Aco and CCo, with another wholly-owned subsidiary, BCo as the GP).

- New LP subscribes for cumulative preferred shares of the Losscos (DCo, a wholly-owned subsidiary of Parent to and Eco to KCo, wholly-owned subsidiaries of DCo).

- Each Lossco makes a loan to New LP at a commercial rate of interest resulting in New LP earning dividend income somewhat in excess of its interest expense.

- New LP repays its daylight loan.

- Parent repays its daylight loan.

- If a Lossco does not have sufficient cash available to pay dividends on its Preferred Shares, DCo will provide to the Lossco, by way of an interest-free loan (the "PS Dividend Loan"), the amount required for the Lossco to pay the full amount of the dividends on the Preferred Shares.

- New LP will use the proceeds from the Preferred Share dividends to pay the interest on the New LP Loans.

- Each Lossco will repay any PS Dividend Loan out of its interest income. If any balance remains, DCo will, at its discretion, make a contribution of capital to the particular Lossco.

- Once the (post-acquisition of control) non-capital losses of the Losscos have been fully utilized, the transactions will be unwound.

Rulings

Including re s. 20(1)(c) deductions of New LP, utilization of streamed and non-streamed losses by Losscos and non-application of s. 12(1)(x) re DCo contributions of capital.

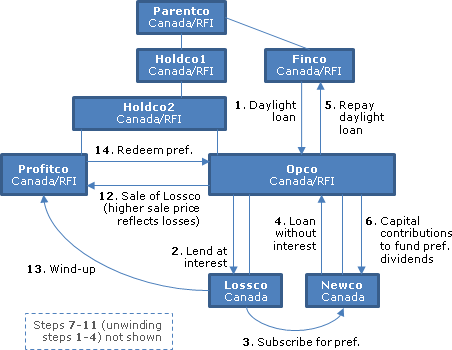

2013 Ruling 2013-0496351R3 - Loss Consolidation

Background

Opco, which has non-capital losses and is a great-grandchild RFI subsidiary of Parentco (also an RFI) and an immediate subsidiary of its RFI parent (Holdco 2), wishes to transfer its non-capital losses to Profitco, another RFI subsidiary of Holdco 2, on a basis that will permit it to be compensated for those losses. A further difference from typical loss-shifting transactions is that in order to not impact its regulatory capital, Profitco does not wish to borrow from Opco. Accordingly, Opco will effectively transfer its losses to a newco (a.k.a. Lossco) and then sell Lossco to Profitco, with the newly-generated Lossco losses being transferred to Profitco on a s. 88(1.1) winding-up.

Proposed transactions

- Opco will borrow under a daylight loan from Finco, a taxable Canadian corporation of which Parentco and XX are members.

- Opco will use such proceeds to make an interest-bearing loan to its newly-incorporated subsidiary, Lossco (Lossco Loan).

- Lossco will use such proceeds to subscribe for redeemable retractable preferred shares of another newly-incorporated subsidiary of Opco (Newco).

- Newco will use such proceeds to make a non-interest-bearing loan (the Interest-free Loan) to Opco.

- Opco will repay the daylight loan.

- At least annually, Opco will make a contribution of capital to Newco to fund the payment by it of accrued dividends on the Newco Preferred Shares held by Lossco, with Lossco then paying all accrued and unpaid interest on the Lossco Loan to Opco.

- In connection with the unwinding, Opco will borrow on a daylight basis from Finco in the amount of the Interest-free Loan, then;

- Opco will repay the Interest-free Loan to Newco, then;

- Newco will redeem its preferred shares issued in 3 above; then

- Lossco will repay the Lossco Loan to Opco; then

- Opco will repay the new daylight loan.

- Opco will transfer all of its Lossco common shares to Profitco in exchange for preferred shares of Profitco with a fair market value and redemption amount equal to the FMV of the transferred Lossco common shares, utilizing s. 85(1).

- Lossco will be wound up into Profitco.

- Profitco will redeem the preferred shares issued in 12 above.

- In a subsequent year, the above transactions will be repeated to use the remaining balance of the Opco non-capital losses.

Reasons for not using a direct loss shift

: "[A] typical loss consolidation arrangement could not be implemented directly with Profitco because the typical loss transfer arrangement does not provide compensation for the transfer of the [Opco non-capital losses]. Moreover, Profitco would need to advise the [financial] Regulator in order to borrow an amount equal to the Daylight Loan and the repayment thereof would require regulatory approval. In addition, such borrowing could impact significantly the regulatory capital that Profitco must maintain in order to satisfy its regulatory and statutory requirements."

Rulings

Including interest deductibility to LosscoA Co on Loan 2 and non-application of ss. 9 and 12(1)(c) to capital contributions received by Newco. SS. 56(2), 15(1),246(1) and 245(2) are not applicable. No explicit s. 55(3)(a) ruling.

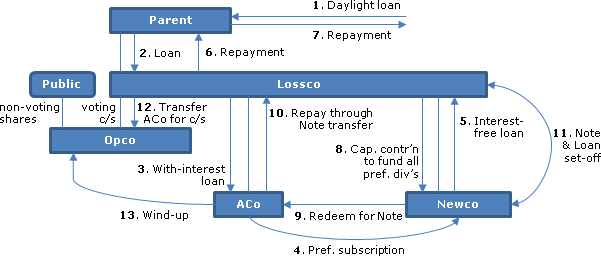

2013 Ruling 2012-0472291R3 - Loss consolidation

Background

Lossco, which has non-capital losses and is a holding company subsidiary of Parent, holds all the common shares of Opco, which is a public corporation with various classes of non-voting shares which are widely held and traded.

Proposed transactions

In order to permit Opco to use losses which Lossco is expected to incur:

- Parent will borrow under a daylight loan (Parent Loan).

- Parent will use such proceeds to make a non-interest-bearing loan to Lossco (Loan 1).

- Lossco will use such proceeds to make an interest-bearing loan (Loan 2) to a newly-incorporated subsidiary of Lossco (A Co).

- A Co will use such proceeds to subscribe for redeemable retractable preferred shares (Newco Preferred Shares ) of another newly-incorporated subsidiary of Lossco (Newco).

- Newco will use such proceeds to make a non-interest-bearing loan (Loan 3) to Lossco.

- Lossco will repay Loan 1.

- Parent will repay the Parent Loan.

- At a subsequent juncture, Lossco will make a contribution of capital to Newco to fund the payment by it of accrued dividends on the Newco Preferred Shares held by A Co., with A Co then paying all accrued and unpaid interest on Loan 2 to Lossco.

- Immediately following the interest payment in 8, and in connection with the unwinding of the loss consolidation arrangement Newco will redeem the Newco Preferred Shares held by A Co in consideration for its issuance of a non-interest bearing promissory note (the "Newco Note"), then;

- A Co will repay Loan 2 by assigning the Newco Note to Lossco, then;

- Loan 3 and the Newco Note will be repaid by mutual set-off.

- Lossco will transfer all of its A Co Common Shares to Opco in exchange for the "Opco Common Shares," utilizing s. 85(1).

- A Co will be wound up into Opco and Newco wound up into Lossco.

Additional information

"Loan 2 is being made to A Co, instead of having Lossco make Loan 2 directly to Opco, to ensure that Opco, which is a public corporation, does not incur debt in order to implement the loss utilization." No rep that A Co has stand-alone borrowing capacity.

Rulings

Including interest deductibility to A Co on Loan 2 and non-application of ss. 9 and 12(1)(c) to capital contributions received by Newco. Opinion that provided draft s. 55(3.01)(h) is enacted, s. 55(2) will not apply to the dividends that ACo will receive from Newco by virtue of s. 55(3)(a).

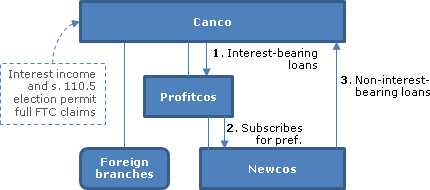

18 December 2012 Memorandum 2012-0461651I7 - Foreign Tax Credits - s. 126 vs. s. 110.5

Canco realized deductible losses on FX hedging instruments due to the strengthening of the U.S. dollar. Accordingly, it engaged in the transactions summarized below ("Project Shift") to shift taxable income from profitable subsidiaries to itself. The intended effect was to allow Canco to claim foreign tax credits, and generate losses in the subsidiaries for carry-back to prior years. However, the hedging losses turned out to be greater than the income which was transferred to it under Project Shift, so that Canco had to make a s. 110.5 election to generate enough taxable income to claim the requisite level of foreign tax credits. Under Project Shift:

- Canco made a demand interest-bearing loan to each of the subsidiaries (without requiring a daylight loan).

- Each of the subsidiaries (which were Canadian) used the borrowed funds to invest in preferred and common shares of new wholly-owned subsidiaries (Newcos).

- Each of the Newcos then lent the proceeds to Canco on a demand, non-interest bearing basis.

- After the income from the subsidiaries were transferred (via interest payments), the structure was unwound.

In noting that Project Shift accorded with CRA's position on acceptable loss consolidation strategies (which it also described in general terms), the Directorate stated:

The purpose of such strategies is generally to effectively allow all the non-capital losses to be utilized, which would be similar to the situation they would be in had the lossco and profitco in the related group been amalgamated. Since we would normally allow for such losses to be utilized under an amalgamation, two entities who choose not to amalgamate for business reasons, should not be disadvantaged, and thus this is why the policy behind such structures are permitted and not subject to GAAR.

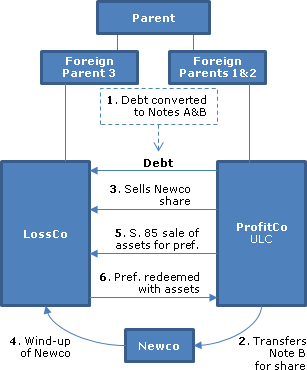

2012 Ruling 2012-0451431R3 - Loss Consolidation

LossCo, which is insolvent, and ProfitCo, both are indirect subsidiaries of a foreign parent. LossCo is indebted to ProfitCo under the LossCo Indebtedness.

Proposed transactions:

- LossCo will amend its prior years' returns to claim unclaimed capital cost allowance, thereby increasing its non-capital losses

- the terms of the LossCo Indebtedness will be amended to make them convertible into two new interest bearing debt obligations: the LossCo Note A Indebtedness, bearing interest at LIBOR and ranking pari passu with the general creditors; and the LossCo Note B Indebtedness bearing interest at LIBOR plus X% and ranking junior to the general creditors

- ProfitCo will then exercise this conversion right

- ProfitCo will transfer the LossCo Note B Indebtedness to newly-incorporated Canadian subsidiary in exchange for one share of Newco

- ProfitCo will sell Newco to LossCo for $X, subject to a price adjustment clause "whereby LossCo will issue a demand promissory note to ProfitCo in an amount equal to the amount of any price adjustment"

- Newco will be wound up into LossCo to make an election under s. 80.01(4) in respect of the settlement of the LossCo Note B Indebtedness; as a result of such settlement, LossCo will become solvent

- ProfitCo will transfer assets including depreciable property to LossCo in consideration for redeemable retractable preferred shares, electing under s. 85(1), with the transferred assets being leased back

- one day later, the preferred shares will be redeemed in consideration for the transfer of the assets back to ProfitCo on a non-rollover basis

Rulings:

- the addition of the conversion feature will not result in a disposition of the LossCo Indebtedness provided that there was no novation or rescission of the debt

- s. 51.1 will apply to the conversion, and no forgiven amount will arise

- the loss denied under s. 40(2)(e.1) on the transfer of the LossCo Note B Indebtedness to Newco will be added to the adjusted cost base of that debt to Newco under s. 53(1)(f.1)

- no forgiven amount will arise on the settlement of the LossCo Note B Indebtedness

- on the taxable transfer-back of the assets, LossCo will utilize its non-capital losses to offset recapture income; and Profitco will acquire such assets at a cost amount and undepreciated capital cost equal to their fair market value [no mention of 1/2 step up limitation in s. 13(7)(e)]

2012 Ruling 2012-0439191R3 - Loss Consolidation

Lossco, which is a wholly-owned indirect subsidiary of a non-resident parent ("Parent"), borrows money under a daylight loan and uses the proceeds to make an interest-bearing loan to Profitco (another wholly-owned indirect subsidiary of Parent), with recourse under that loan (the "Profitco Note") being limited to the preferred shares of Newco (incorporated by Lossco) which Profitco subscribes to with the Profitco Note proceeds. The Profitco Note also provides that is may be settled through delivery of such preferred shares. Newco uses the proceeds from such preferred shares to make a non-interest bearing loan (the "Lossco Note") to Lossco, which repays the daylight loan. The dividends on the Newco preferred shares will exceed the interest payable by Profitco.

Pursuant to a capital contribution agreement, Lossco will make periodic capital contributions to Newco equal to the amount of accrued but unpaid dividends on the Newco preferred shares. After the utilization of the Lossco losses, the arrangement will be unwound by Newco redeeming its preferred shares through delivery of the Profitco [sic, Lossco] Note to Profitco, and the Profitco and Lossco Notes then being set-off.

Lossco has permanent establishments in various provinces, whereas Profitco only has a permanent establishment in one province. A "financial institution has provided confirmation, in a letter dated XX, that Lossco has the ability to obtain borrowings up to $XXX."

Rulings: that interest not exceeding a reasonable amount will be deductible by profitco on the Profitco Note; and that the periodic capital contribution amounts received by Newco will not be included in its income.

5 October 2012 APFF Roundtable Q. , 2012-0454061C6 F - Transfer of a Lossco to a related corporation

Example 1

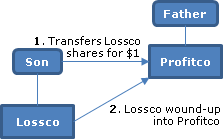

Son claims an ABIL under s. 50(1) with respect to his share investment in a wholly-owned corporation (Lossco), which had ceased active business operations in the year, and then transfers his shares of Lossco at the beginning of the following year to a corporation wholly-owned by his Father (Profitco) for consideration of $1, with Lossco then being liquidated into Profitco under s. 88(1).

Example 2

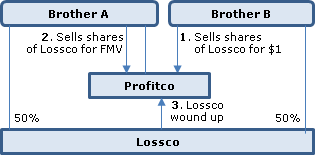

Brothers A and B each hold 50% of the common shares of Lossco, which had ceased active business operations in the year, with Brother B claiming an ABIL under s. 50(1). Brother B then transfers his shares of Lossco at the beginning of the following year to a corporation wholly-owned by Brother A (Profitco) for $1, Brother A sells his shares of Lossco to Profitco for their fair market value, and Lossco is liquidated into Profitco under s. 88(1).

CRA indicated that both examples represented transactions of a different type than loss consolidation transactions described in 2009-0332571R3. However, as in these two examples, there was not an acquisition of control of the Losscos by virtue of s. 256(7)(a)(i), "it appears that the restrictions provided for in paragraphs 88(1.1)(e) and 88(1.2)(c) respecting the utilization of losses other than capital losses and net capital losses would not be applicable." (TaxInterpretations translation)

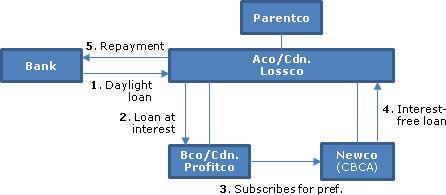

2012 Ruling 2012-0437881R3 - Loss Utilization

Set-up

Aco, which is a direct Canadian-resident holding-company subsidiary of Parentco (which, in turn, is a wholly-owned subsidiary of Ultimate Parentco, a public corporation), borrows under a daylight loan in order to make an interest-bearing loan (at bankers' acceptance rate plus X%) to its profitable Canadian subsidiary Bco, which has permanent establishments in various provinces. Bco uses such proceeds to subscribe for non-voting cumulative redeemable retractable preferred shares of Newco, a newly-incorporated CBCA subsidiary of Aco. Newco uses such proceeds to make a non-interest-bearing loan to Aco.

Periodic payments

The periodic interest/dividend payments will be handled from time to time as follows:

- Pursuant to a capital contribution agreement, Aco will make a contribution of capital to Newco in an amount equal to the accrued but unpaid dividends on the Newco preferred shares held by Aco

- Newco will declare and pay such dividends

- Bco will pay the interest on its borrowing from Aco

Unwinding

On the unwinding of these arrangements, Newco will redeem its preferred shares by assigning the loan owing to it by Aco, with Aco and Bco then setting off the loans now owing to each other.

Rulings

as to interest-deductibility by Bco and the contribution amounts not being included in the income of Newco under s. 9, 12(1)(c) or (x).

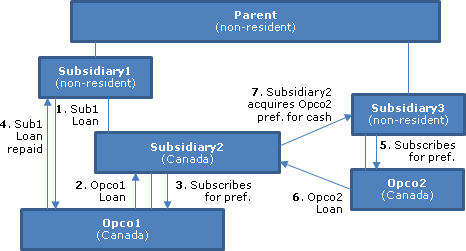

2012 Ruling 2011-0427951R3 - Loss Consolidation

1st Proposed transactions

Subsidiary1, which is a non-resident subsidiary of Parent (a non-resident publicly listed corporation) makes an interest-bearing loan to Opco1 (the "Subsidiary1 Loan"). Opco1 is a direct wholly-owned Canadian subsidiary of Subsidiary2, which is a Canadian corporation that is an indirect wholly-owned subsidiary of Subsidiary1. Opco1 on-lends the proceeds of the Subsidiary1 Loan on an interest-bearing basis to Subsidiary2 (the "Opco1 Loan"). Subsidiary2 uses the proceeds of the Opco1 Loan to subscribe for non-voting cumulative redeemable retractable preferred shares of Opco1. Opco1 then repays the Subsidiary1 Loan from Parent.

2nd Proposed transactions

Subsidiary3, which is the direct and indirect parent of subsidiaries carrying on a different line of business than those of the direct and indirect subsidiaries of Subsidiary1 (and which is not explicitly stated to be a subsidiary of Parent in the unredacted portions of the letter), subscribes for preferred shares (similar to those of Opco1) of Opco2, which is an indirect wholly-owned subsidiary of Subsidiary3 having non-capital losses that were incurred in various provinces (and with some of such non-capital losses having been incurred prior to Subsidary3's acquisition of control of Opco2). Opco2 is affiliated with Subsidiary2 and Opco1. Opco2 uses such share subscription proceeds to make an interest-bearing loan (the "Opco2 Loan") to Subsidiary2, which uses such proceeds to acquire the preferred shares of Opco2 held by Subsidiary3.

Unwinding

The above transactions will be reversed once Subsidiary2 has incurred sufficient interest expense to generate non-capital losses that eliminate prior years' taxable income. In the meantime, payments of interest and dividends will be made through the set-off of like amounts, with the payment of the balance owing. Subsidiary2 will have sufficient borrowing capacity to effect the proposed transactions.

Rulings

Interest deduction ruling for Subsidiary2 and ruling that Opco2 will be entitled under s. 111(1)(a) to deduct its non-streamed non-capital losses from its taxable income arising on the Opco2 Loan provided that its streamed non-capital losses are first deducted in accordance with the loss-streaming rules.

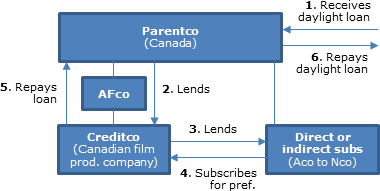

2012 Ruling 2012-0426581R3 -

Creditco is an indirect subsidiary of Parentco, which is a Canadian corporation. Creditco carries on business in one province, has non-capital losses and unutilized credits and is a qualified corporation (presumably as defined in s. 125.4(1).)

Creditco receives a loan from Parentco (funded by Parentco out of a daylight loan) and on-lends the proceeds in demand loans bearing interest at a market rate to various direct and indirect subsidiaries of Parentco (Aco through to Nco), who use the lent proceeds to subscribe for preferred shares of Creditco bearing a cumulative dividend equal to the interest rate on the demand loans plus a spread. These demand loans do not exceed the respective borrowing capacities of the borrowing subsidiaries. Creditco uses such share subscription proceeds to pay off the loan from Parentco. The arrangement will be unwound in X years.

Interest deduction ruling given re Aco to Nco; and ruling that these transactions will not cause Creditco to cease to be a qualified corporation.

Income Tax Technical News No. 44 13 April 2011 [archived]

If a typical loss-consolidation transaction results in an incidental shifting of income or losses between provinces, simply because the profitco and the lossco happen to have different provincial allocations, there should not be a concern from the perspective of agreeing provinces. If, on the other hand, the transactions are designed to deliberately shift income or loss between provinces, provincial concerns will have to be considered.

2010 Ruling 2009-0332571R3

Mr A and Mrs B are siblings. Mr A holds all the voting shares of HA which, in turn, holds Lossco. HA also is the common shareholder of HASub. Mr. B and/or Mrs B indirectly control HBSub through a similar structure.

Lossco will make interest-bearing loans to HASub and HBSub, and HASub and HBSub will use the loan proceeds to subscribe for preferred shares of Lossco, thereby accomplishing a loss shift.

Standard rulings including GAAR. Summary states:

The transfer of losses between related, but not affiliated, corporations should not result "in an abuse having regard to [the provisions of the Act]...read as a whole", for the purposes of subsection 245(4), because specific provisions such as subsections 111(4) to (5.5), 256(7), 191.3(1), 112(2.4), paragraph 55(3.1)(c), section 80.04 etc. allow loss utilization transactions between related corporations, while only subsection 69(11) does not allow rollover where property is transferred to a person other than a person that is affiliated with the transferor.

2009 Ruling 2008-0289771R3

Favourable ruling was given with respect to transactions in which the following three transactions are repeated until the right amount of interest-bearing data is created: Lossco Sub transfers its portfolio to its parent, Lossco in exchange for an interest-free demand note, Lossco transfers the portfolio to a newly-created subsidiary ("Newco") in exchange for an interest-bearing demand note, and Newco transfers the portfolio to Lossco Sub in exchange for Lossco Sub preferred shares.

17 December 2008 T.I. 2007-0253031E5

Ruling request denied because the Lossco did not have the borrowing capacity to effect the loss consolidation arrangement: "It is the borrowing capacity of the entity that actually suffers the losses, rather than the borrowing capacity of the affiliated group as a whole, that is relevant in the particular circumstances."

Income Tax Technical News, No. 30, 21 May 2004

As noted earlier, loss consolidation transactions must be legally effective. ...However, we would not feel comfortable providing a ruling on a loss consolidation transaction that contemplates dollar amounts and time frames that are blatantly artificial. Thus, in order to be provided with a ruling, we must be able to satisfy ourselves that the transactions are plausible, and the quickest way for us to obtain such assurance is through a commitment letter. ...

While we have not reached the point where we would state that CRB Logging is no longer good law, we have provided rulings on some upstream shareholding situations. The key criteria to be met in such situations is the existence of other assets in the parent company that can generate sufficient income to pay the dividends on the preferred shares held by the subsidiary.

27 May 1998, Chartered Accountants of Ontario Roundtable, 9811750

"Transfers of income or deductions between corporations that are affiliated using transactions that are legally effective and complying with all applicable provisions of the Income Tax Act will not usually result in the application of GAAR."

12 April 1995 T.I. 9508595 [inventory roll-down to use non-capital losses]

Would GAAR apply where inventory is transferred by a corporation to a wholly owned corporation for the purpose of utilizing the accumulated non- capital losses of that subsidiary? CRA stated:

The Technical Notes to subsection 245(4)...[state]:

In fact, the scheme of the Act as a whole, and the expressed object and spirit of the corporate loss limitation rules, clearly permit such transactions between related corporations where these transactions are otherwise legally effective and comply with the letter and spirit of these exceptions. Therefore, even if these transactions may appear to be primarily tax-motivated, they ordinarily do not fall within the scope of section 245… .

1994 A.P.F.F. Round Table, Q. 3

Where Mr. X has been employed by Opco Inc. for a number of years and is also the sole shareholder of a corporation ("Investco") with accumulated non-capital losses, the non-capital losses of Investco could be utilized by having Opco conclude an agreement with Investco under which services previously rendered directly by Mr. X are to be rendered by Investco. Such an arrangement generally would not be considered to result in an abuse for purposes of s. 245(4).

1 December 1992 T.I. (Tax Window, No. 27, p. 9, ¶2319)

If one of the purposes of a series of transfers of a capital property within a related corporate group is to utilize non-capital losses of one of the corporations and if the vendor corporation has no intention of reacquiring the particular assets, then GAAR will not apply.

2 October 1990 T.I. (Tax Window, Prelim. No. 1, p. 21, ¶1024)

Where a non-resident person incurs a non-capital loss in a business carried on in Canada, the loss may be applied against income earned by the person after becoming a resident of Canada. However, non-capital losses incurred in a foreign business by the non-resident may not be applied against Canadian source income.

Articles

Vukets, "Structural Issues and Utilization of Domestic Loss Carryforward Pools", 1993 Conference Report, C. 23

Discussion (at pp. 28-29) of Revenue Canada's position on similar businesses.

Paragraph 111(1)(b) - Net capital losses

Administrative Policy

14 August 2014 Memorandum 2013-0506691I7 - Capital Losses - Health & Welfare Trusts

Are health and welfare trusts ("HWTs") permitted to incur capital losses and deduct net capital losses when computing taxable income under Division C and/or adjusted taxable income under Division E.1? CRA stated:

2004-009364 concluded that where a HWT has expenses that were otherwise deductible and not allowed because of the limitation discussed in paragraph 12 of IT-85R2, it will be permitted to use those expenses to reduce its adjusted taxable income for purposes of AMT. …

Consistent with section 3.., a HWT's gross trust income for a year includes its taxable capital gains realized in the year in excess of its allowable capital losses realized in the year. …[I]t would be inequitable to prevent a HWT from reducing taxable capital gains through the application of net capital losses, given that a HWT effectively applies allowable capital losses on a current basis when determining its gross trust income for a year.

5 July 2013 T.I. 2013-0479161E5 - Capital Loss Adjustment - 152(4)

The correspondent asked whether a capital loss for a statute-barred year can be amended to increase the amount of the capital loss, and whether that loss can be carried forward to a non-statute-barred year. CRA stated:

[T]he Minister may adjust the net capital loss for a taxation year after the normal reassessment period, but cannot adjust the tax payable for that year except as described above. In other words, the Minister may adjust the net capital loss (available for carry forward), but the amount of the capital loss previously not claimed cannot be applied against the capital gains reported for the statute-barred year. Furthermore, the net capital loss would be equal to the net capital loss that would have been available had the allowable capital loss originally been reported correctly.

Paragraph 111(1)(e) - Limited partnership losses

Administrative Policy

31 May 2012 T.I. 2012-0436521E5

In Year 1, C and D form a limited partnership (CD), which incurs a loss of $500 in that year , which is $300 in excess of their contributed capital. At the beginning of Year 2, C and D transfer their interests in CD under s. 97(2) to another limited partnership (Master) in consideration for LP interests in Master. At the end of Year 2, Master allocates $500 of income to CD which, in turn, allocates this income equally to C and D.

Notwithstanding the subsequent interposition of Master, C and D have a limited partnership loss in respect of CD because they were members of CD at the end of Year 1. However, the at-risk amount of its interest in CD at the end of Year 2 would be computed by Master and not by C and D. Accordingly, as C and D would not have an at-risk amount in respect of CD at that time, they would not be able to deduct their limited partnership losses in respect of CD at that time, notwithstanding the allocation to them of income which was sourced to CD.

25 February 2005 T.I. 2004-0107981E5 -

In response to an inquiry as to the deductibility of limited partnership losses ("LPL") in a multi-tier partnership arrangement, the Directorate noted that "the LPL of a partnership that is a member of a limited partnership cannot be used by the partnership," and then stated:

It is our view that the losses allocated by a limited partnership to each of its members, including another partnership (as a result of subsection 102(2) of the Act), will be deductible by each member, to a maximum of each member's (including the member partnership's) at-risk amount. The excess of the loss over the member's at-risk amount is deemed to be a member's LPL by virtue of paragraph 96(2.1)(e) of the Act. However, this LPL cannot be used by the member partnership because a partnership is not a taxpayer for purposes of paragraph 111(1)(e) of the Act. Also, subsection 96(1) of the Act does not allow the transfer of a LPL to its members.

14 May 2004 T.I. 2004-0062801E5

Suppose that Mr A and B form a partnership (AB Partnership), with AB taking the $100 contributed by each of them to, in turn, contribute $200 to a limited partnership, which realizes a business loss of $500 in Year 1 and business income of $500 in Year 2.

Although AB Partnership would have a $300 limited partnership loss for Year 1, Mr A and B would have no limited partnership loss with respect to the limited partnership when income is allocated to them in Year 2 ("subsection 96(1)...does not allow the transfer of a limited partnership loss to its members"), with the result that they would have no deduction from that income allocation in respect of the previously denied loss of CD - nor could the limited partnership loss of AB Partnership be used by it "because a partnership is not a taxpayer for purposes of paragraph 111(1)(e)...."

2 May 1994 T.I. 5-940777 -

A general partnership, that is a limited partner of a limited partnership, cannot carry forward its limited partnership losses arising from the limited partnership because it is not a taxpayer for purposes of s. 111. Furthermore, s. 96(1) does not provide for the flow-through of limited partnership losses of a partnership to its partners.

92 C.M.TC - Q.11

Deductions under s. 111(1)(e) are not available to a general partner who was formerly a limited partner.

Articles

Forster, "Limited Partnership Losses", Canadian Current Tax, June 1992, p. P57

A limited partner who becomes a general partner thereafter will have no at-risk amount and, accordingly, will be unable to deduct any unutilized limited partnership losses.

Subsection 111(2) - Year of death

Articles

Sandra Bussey, Jim Barnett, "Capital Gains and Losses in the Year of Death", Tax for the Owner-Manager, Vol. I, No. 2, April 2001, p. 10.

Subsection 111(3) - Limitation on deductibility

Cases

CCLI (1994) Inc. v. The Queen, 2007 DTC 5372, 2007 FCA 185

In its 1989 taxation year, the taxpayer deducted non-capital losses of $29.4 million which it treated as comprising a non-capital loss carried back from 1991 of $5.8 million and a $23.5 million non-capital loss carried back from 1992. The Minister, following a request by the taxpayer for a loss determination for the 1991 and 1992 taxation years provided a loss re-determination indicating that the losses for 1991 were now $25.8 million and for 1992 were $8.1 million (based on treating the taxpayer's foreign exchange gains and losses as being on capital account rather than income account). These re-determined figures were correct.

The Court reversed the Tax Court, where Miller J. found that in determining the amount of the 1991 loss that was available to be deducted by the taxpayer in 1993, the Minister was entitled and required to apply the ordering provisions of s. 11(3), so that the amount of the 1991 loss that should be considered to have been utilized by the taxpayer in its 1989 taxation year was higher than the $5.8 million originally considered by the taxpayer to have been so applied. The Minister could not point to any legal authority for requiring the deduction of the 1991 loss in 1989 (which was statute-barred) to be increased (so that the amount of such loss that could be carried forward was decreased). Furthermore, under subsection 111(1), "only the taxpayer has the right to choose how to allocate the non-capital loss of a particular year between the 3 prior years and the 7 subsequent years, subject only to the restrictions in subparagraphs 111(3)(a)(i) and 113(3)(b)(i)."

Paragraph 111(3)(b)

Administrative Policy

17 May 1993 Memorandum (Tax Window, No. 31, p. 11, ¶2522)

Except as provided in s. 111(3)(b), s. 111 does not impose an ordering on the application of losses and, therefore, a taxpayer can claim losses in the manner which is most beneficial. Accordingly, where a taxpayer incurred an allowable business investment loss and an ordinary non-capital loss in Year 1, had income equal to the allowable business investment loss in Year 2, and in Year 3 there was an acquisition of control resulting in the application of s. 111(5), the taxpayer could choose to have the allowable business investment loss considered to have been applied in Year 2.

Subsection 111(4) - Acquisition of control

Administrative Policy

10 July 1997 T.I. 5-971588 -

"The policy stated in paragraph 18 of IT-302R3 would apply to a corporation receiving a notice of reassessment in the same manner as is described for a corporation receiving a notice of assessment."

Paragraph 111(4)(c)

Administrative Policy

2005 APFF Roundtable Q. 1, 2005-014088

As s. 249(4) does not apply to a non-resident corporation that does not have a permanent establishment in Canada and whose control is acquired by another non-resident corporation, ss.111(4)(c) and (d) will not apply to shares of a taxable Canadian corporation held by the first non-resident corporation.

Paragraph 111(4)(d)

Administrative Policy

94 C.P.T.J. - Q.25

S.111(4) does not generally apply to the capital property of a foreign affiliate upon the acquisition of control of the affiliate or the Canadian parent of the affiliate.

Tax Professionals Mini Round Table - Vancouver - Q. 11 (March 1993 Access Letter, p. 104)

Where s. 111(4)(d) applies to create a loss, then s. 40(2)(g) will deem that loss to be nil where the criteria therein are met.

Paragraph 111(4)(e)

Administrative Policy

10 February 1995 T.I. 950069 (C.T.O."Paragraph 111(4) Amended Designation")

"In view of the fact that, in subsection 248(1) of the Act, the term 'assessment' is defined as including a 'reassessment', it is our position that a corporation is permitted to file an amended designation within 90 days from the later of the date of mailing of a notice of assessment for the taxation year ending with the acquisition of control and the date of mailing of a notice of reassessment, if any, for that year."

10 February 1995 T.I. 942448 (C.T.O."Paragraphs 111(4)(c) & e")

S.111(4) does not generally apply to the capital property of a foreign affiliate upon the acquisition of control of the affiliate or the Canadian parent of the affiliate.

93 CR - Q. 22

Depreciable property designated under s. 111(4)(e) is deemed to have been disposed of by the corporation and reacquired by it for the purposes of computing the corporation's taxable income, including Part XI of the Regulations. However, Regulation 1100(2.21) will ameliorate the resulting consequences.

8 July 1992 T.I. 5-922051

Because an "assessment" includes a "reassessment", a corporation is allowed to amend a previously-made election under s. 111(4)(e) for a taxation year within 90 days from the date of the notice of reassessment for that year.

13 February 1992 T.I. (Tax Window, No. 16, p. 19, ¶1747)

RC will accept an election under s. 111(4)(e), or any written amendment thereto, made within 90 days from the date of assessment or reassessment of the fiscal period ending on the acquisition of control.

90 C.R. - Q42

Because s. 111(4)(e) is only applicable with respect to capital properties rather than foreign currency obligations, the designation will not be available with respect to an unrealized gain or loss on the latter.

90 C.R. - Q45

RC will not accept designations under s. 111(4)(e) beyond the time limits specified therein.

88 C.R. - Q8

Ss.111(4)(c), (d) and (e) do not apply to foreign exchange gains and losses on indebtedness of the corporation.

Subsection 111(5) - Idem [Acquisition of control]

Cases

Yarmouth Industrial Leasing Ltd. v. The Queen, 85 DTC 5401, [1985] 2 CTC 67 (FCTD)

For the purposes of s. 111(5), control of a corporation may be acquired by virtue of control being acquired of its parent. [C.R.: 125(1)]

Malka v. The Queen, 78 DTC 6144, [1978] CTC 219 (FCTD)

The taxpayers, who acquired 400 voting common shares in a company were held to have thereby acquired control of it notwithstanding that 500 voting preference shares with a par value of $1.00 each had been issued to the vendors immediately prior to the time of the acquisition. Under the Quebec corporate law, the common shareholders could liquidate the company at any time and "preferred shareholders, that can be discarded that easily, cannot seriously be said to have a controlling interest." In addition, the "holders of preferred shares could not care less about [the company] as ... their main worry was to assure themselves to get back the $500 that had been paid for the shares." The supposed control by the preference shareholders accordingly was a sham.

See Also

A.G. of Canada v. Fallbridge Holdings Ltd. (1985), 31 BLR 57 (FCA)

It was stated, obiter, that the fact that two companies acted in concert to effect an acquisition did not necessarily constitute them as a group of persons.

Administrative Policy

25 February 1999 T.I. 5-990002 -

Various illustrations of the RC position that there generally will be an acquisition of control whenever one of two shareholders, each holding 50% of the shares, sell his or her shares to another person.

Income Tax Technical News, No. 16

"The Department will apply the Supreme Court's findings [in Duha] that, outside of the constating documents of a corporation and its share register, Unanimous Shareholder Agreements are generally the only relevant documents that need to be examined in determining de jure control." RC would generally seek to apply GAAR when temporary control of a corporation is acquired in order to take advantage of tax benefits.

93 C.R. - Q. 57

Where an individual makes an assignment in bankruptcy, there will be no acquisition of control of a corporation owned by the individual for purposes of s. 111(5), because s. 128(2)(a) deems the trustee in bankruptcy to be the agent of the bankrupt individual.

88 C.R. - Q.43

Where 4 unrelated individuals each own 1/4 of the shares of a corporation and one of the individual's shares are redeemed, then control of the corporation will not be considered to have been acquired if A, B and C acted together to control the corporation both before and after the redemption.

If A, who owns all the shares of a corporation, sells 1/3 of the shares to each of B and C, then control of the corporation will be considered to have been acquired if any of A and B, B and C, A and C or A, B and C act together to control the corporation.

Where a public corporation reduces its shareholding in a second public corporation ("Pubco 2") from 55% to 35%, then if persons can be identified after the sale who own in aggregate more than 50% of the shares and such persons act together to control Pubco 2, then control of Pubco 2 will have been acquired by a group of persons.

Articles

Joel A. Nitikman, "Who Has De Jure Control of a Corporation When Its Shares Are Held by a Limited Partnership?", 2011 Canadian Tax Journal, Vol 59, p. 765

Argues that (at least where the shares of a subsidiary corporation held as partnership property are registered in the name of the limited partnership rather than the general partner), an acquisition of control of the general partner or of the limited partners will not result in an acquisition of control of the subsidiary corporation as it is owned by the limited partnership itself.

Paragraph 111(5)(a)

Cases

Manac Inc. v. The Queen, 98 DTC 6605, Docket: A-122-96 (FCA)

All the voting shares of a corporation ("Nortex") which manufactured resin-coated wood panels, were acquired by a subsidiary of a predecessor of the taxpayer ("2432"). Nortex was then wound-up into 2432, and 2432 amalgamated with the predecessor of the taxpayer.

Nortex's former business of manufacturing fibreglass panels for sale to 2432 which used the panels in the manufacture of boxes for trailers and semi-trailers did not satisfy the test in s. 111(5)(a)(ii) given that there was no evidence that income derived from the sale or development of the panels made up substantially all the income attributable to the 2432 business. In addition, the Court did "not see how property which loses its identity when incorporated into an end product can be described as property similar to the end product" (p. 6608).

The Queen v. Diversified Holdings Ltd., 97 DTC 5203, Docket: A-309-94 (FCA)

The taxpayer, which at the relevant times operated a ranch and was a real estate developer, acquired, in an arm's length transaction, another BC company ("860") that operated a parking lot. Following a sale of the parking lot to a creditor of 860 and an amalgamation of the taxpayer and 860, the amalgamated corporation sought to deduct the losses of 860 from income of its real estate development business. In dismissing the Crown's appeal, Strayer J.A. stated (at pp. 5207-8):

"In the present case the learned trial judge was faced with a generic type of business, namely real estate development, and it was open to him to conclude that such business had not disappeared. It was also open to him to conclude that a period of inactivity of two months was not enough to demonstrate the end of such a business ... ."

The Queen v. Dorchester Drummond Corp. Ltd., 79 DTC 5163, [1979] CTC 219 (FCTD)

A company which acquired vacant land with the intention of eventually erecting a highrise office tower thereon, and which during the period between the time of acquisition and the time that the vacant land was sold for a gain, operated a parking lot on the land during years that it was not prohibited from doing so by municipal by-law, was held to be "undoubtedly carrying on business during the years in question."

Orlando v. MNR, 62 DTC 1064, [1962] CTC 108, [1962] S.C.R. 261

With the exception of minimal revenues from the sale of hay, the only revenues derived by the taxpayer from her farm lands were sums which she received for the annual sale of topsoil to a company controlled by her husband. Abbott J. held (p. 1065) that the taxpayer's "dealings in topsoil had no relation to any farming operations she may have been carrying on" for purposes of s. 27(1)(e) of the pre-1972 Act.

See Also

Birchcliff Energy Ltd. v. The Queen, 2015 TCC 232

A predecessor ("Birchcliff") of the taxpayer negotiated a plan to merge with a corporation ("Veracel"), which had discontinued its medical equipment business, in order to access Veracel's non-capital losses and credits. Investors subscribed for subscription receipts of Veracel and received voting common shares of Veracel therefor under a Plan of Arrangement, and Veracel and Birchcliff amalgamated immediately thereafter under the Plan. The voting common shares received by the investors on the amalgamation represented a majority of the voting shares of the amalgamated corporation, so that no acquisition of control of Veracel occurred under s. 256(7)(b)(iii)(B), and the loss-streaming rules under ss. 111(5)(a) and 87(2.1) were avoided.

Before finding that this represented abusive avoidance under s. 245(2), Hogan J rejected (at para. 61) the Minister's submission that the new investors represented a "group of persons" who had acquired control of Veracel:

[T]here is no evidence to show that the New Investors knew each other or had a plan to control the corporation together. ..[They] entered into the Subscription Agreement and granted a proxy to [two officers of Veracel and Birchcliff] to vote their shares in favour of the plan…because it appealed to their individual self-interest [and]…did so without discussing the matter with the other investors. Therefore…the grant of the proxy…is insufficient to demonstrate a common connection… .

See summary under s. 245(4).

NRT Technology Group v. The Queen, 2013 DTC 1021 [at 110], 2012 TCC 420, briefly aff'd 2013 DTC 5153 [at 6360], 2013 FCA 221

The taxpayer, which sold ATMs to the gaming industry, and specialized keyboards and price scanners to retail stores, in January 2006 acquired a corporation ("Telepanel") that had been carrying on a business of selling electronic price display modules to retail stores. C. Miller J. found that s. 111(5)(a) precluded the taxpayer from using Telepanel's losses in the taxpayer's taxation year ending on September 30, 2007, as the business was not carried on for profit or with a reasonable expectation of profit in that year. The business was "dormant" in that year: the only third-party business activity identified was the receipt of a small licence fee, and explaining to a customer how to replace batteries. Furthermore, if the former Telepanel business nonetheless was still being carried on, it was not being carried on with a view to profit, having regard to the objective factors listed in Tonn. In particular, the business had persistent and substantial losses, and the taxpayer had no plan, and made no effort, to turn the business around, and instead used the Telepanel technology in its gaming business, which was not the same or a similar business.

No. 678 v. MNR, 60 DTC 45 (TAB)

The taxpayer, which had been a dealer in trucks and cars, ceased operations and, following a change of control, started operating service stations. These were found to be two separate businesses, with the result that losses from the former business could not be carried forward for deduction from the profits of the second business.

Maidment v. Kibby & Anor., [1993] BTC 291 (D)

Vice-Chancellor Nicholls affirmed the finding of the Commissioner that the purchase as a going concern by the taxpayers of an existing fish and chip shop business in a village five miles away, followed by the continued conduct of that business from the same premises but with substantial variations in the mode of conduct thereof should be characterized as an expansion by the taxpayers of their own fish and chip business into the new premises, rather than as a continuation of the trade carried on by the former owner at the new premises.

Montplaisir Ltée v. MNR, 92 DTC 2317 (TCC), aff'd , 2001 DTC 5366 (FCA)

The taxpayer, which acquired control of a corporation ("Pinard") carrying on a used car dealership, was found not to be carrying on the business of Pinard with a reasonable expectation of profit following the amalgamation of the two corporations given that prior to the amalgamation Pinard had disposed of all its tangible assets and not continued with any of its staff other than its best salesman. Lamarre Proulx J. stated (p. 2321) that "it is impossible to logically arrive at the conclusion that the mere use by an automobile garage business of a key person from another automobile garage business is the continuation of that latter business".

Queen & Metcalfe Carpark Ltd. v. MNR, 74 DTC 6007, [1973] CTC 810 (FCTD), aff'd [1976] CTC xvi (FCA)

The proposed renting out of hotel premises or a cinema structure was implicitly treated as part of the taxpayer's business of acquiring various properties and leasing them out for rental use, notwithstanding that it had never rented out facilities of this character before: "the fact that the realty handled and leased by the appellant is of a different type or kind than that contemplated by the structure [in question] makes no difference."

Jeffrey v. Rolls - Royce, Ltd. (1961), 40 TC 443 (HL)

In finding that sums received by the taxpayer for providing technical know-how to foreign organizations were receipts of its trade of manufacturing automobiles and airplane engines, Lord Radcliffe stated (at p. 495) that "I think that the Crown were right in saying that the Company's new way of exploiting 'know-how' was no more than a development of its direct manufacturing trade and did not rank, or need to rank, as a separate business".

Utah Co. of Americas v. MNR, 59 DTC 1275, [1959] CTC 496 (Ex Ct)

A Nevada company which was engaged in Canada in the construction of housing (and of a large building in Vancouver), and which carried on a mining operation (after having wound up the company which had previously carried on that operation) was found to be carrying on two separate businesses for purposes of s. 27(1)(e) of the pre-1972 Act. The two divisions "had different (a) processes; (b) products; (c) services; (d) customers for the products ... ; (e) inventories; (f) locations; (g) union contracts; (h) offices; and (i) staffs. In addition, the accounting and records for each of the two divisions were maintained separately ... I find here no inter-connection, interlacing or interdependence and no unity embracing these two operations."

Frankel Corp. Ltd. v. MNR, 59 DTC 1161, [1959] CTC 244, [1959] S.C.R. 713

An operation of recovering non-ferrous metals from scrap material, alloying them with other non-ferrous metals to specifications required by purchasers, and selling the products, was found to be a separate business (for purposes of the Doughty doctrine) from an operation of dealing in ferrous and non-ferrous scrap, a wrecking and salvaging operation and a steel fabrication and erection operation, in light of evidence that the areas and equipment of the respective operations were separate (albeit contiguous) and the maintenance of separate accounts. Compared to the ferrous operations, the sources of material and the customers were, in general, different, and the staffs were separate. In addition, those in the trade generally regarded the smelting and alloying of non-ferrous metals as separate from that of iron and steel.

Keir & Cawder, Ltd. v. C.I.R. (1958), 38 TC 23 (C.S. (1st Div.))

The taxpayer, which sold materials for use in construction projects, made a foray into the field of construction contracting which was terminated on the death of a consulting engineer whose services it had retained. In finding that the death did not result in the loss of the taxpayer's business, the Lord Present (Clyde) stated (p. 30):

"The civil engineering activities of the Appellants were not being conducted by a separate entity, but formed an inchoate part of a single business which still continues."

Canadian Fruit Distributors Ltd. v. MNR, 54 DTC 1145, [1954] CTC 284 (Ex. Ct.)

The respective activities of the taxpayer in acting as a broker for the sale of the fruit and vegetable products of its parent and of third parties were found to be one business.

Administrative Policy

2011 Ruling 2011-0392171R3 -

A deposit-taking financial institution with significant non-capital losses (LossCo") was directed by the provincial regulator to quickly merge with a financially stronger institution. Accordingly, ProfitCo acquired all the the LossCo shares of LossCo Shareholder, and ProfitCo and LossCo then amalgamated to form AmalCo, with each LossCo and ProfitCo shareholder receiving shares of AmalCo which were substantially similar to the shares in the capital of ProfitCo. AmalCo will sell or close down some of the LossCo branches, but employ the employees associated with the closed branches and the continuing branches (as well as the employees of the branches to be sold until the time of sale). The ProfitCo Services which were provided before the amalgamation will be provided by AmalCo through the LossCo retained branches (now held by AmalCo) to the customers of those branches, with LossCo customers of the closed branches being serviced by the geographically proximate ProftCo branches.

Before ruling that GAAR would apply respecting transactions intended to avoid the application of the debt forgiveness rules to the non-capital losses of LossCo, rulings were provided that: the operation by AmalCo of the retained branches and the branches to be sold will constitute the carrying on by it of the LossCo business for purposes of s. 111(5)(a)(i); and that the income of AmalCo from the services referred to above "will be considered to be derived from the sale, leasing, rental or development, as the case may be, of similar properties or the rendering of similar services" to the services previously rendered by LossCo.

2007 Ruling 2006-019842 -